GDP Gist: The Ups and Downs of Q1

Where the Economy Took a Yawn (Bad News)

Yikes! The first-quarter GDP slipped to -0.3%—not just a pinch, but a full-on slide. The market had been braced for a modest -0.2% dip, so this surprise hit harder than a cold shower at dawn.

For a moment, the numbers looked like they’d left the table from a 2022 recession—though that’s one step that was already corrected in the revision. Imagine the economy waving a “Sorry for the scare, we’ve moved on!” flag.

What Was Still Bright (Good News)

- Revamped Figures – The bad print was already clawed back when the initial figures were updated, easing the knockdown blow.

- Core Strengths – While the headline looks grim, subsectors like manufacturing and services showed resilience, keeping the coin of enthusiasm in circulation.

- Hope Spikes – Analysts see this as a natural correction, not a catastrophic downturn. Think of it as a hiccup in a marathon runner’s stride.

Bottom Line: Take the Good, Politely Toss the Bad

Economists are twitching their eyebrows at the revamped data, but the overall vibe? The economy’s pulse is still breathing — just a tad sluggish. Hold onto that optimism; it’s like a cup of coffee that’s a light jerk, not a universe-shattering blackout.

Surprise Bounce: GDP’s Unexpected High‑Fives

Hey folks! Grab your coffee because the latest GDP numbers are a curve‑ball that even the Atlanta Fed didn’t see coming. The bad news—well, it was supposed to be worse. Remember the Fed’s new estimate: a whopping -2.7% in GDP, dropping to -1.5% when you chew out those record gold imports? Yep, that’s the story we’re flipping tonight.

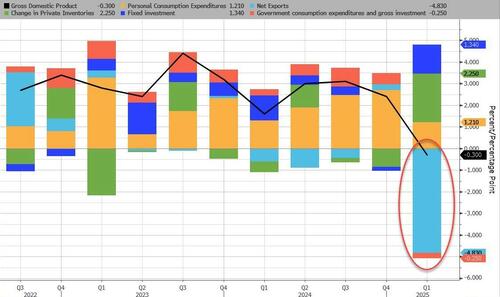

What’s Inside the Numbers?

- Personal Consumption: Dropped to 1.21% from 2.70% but still packs a punch with an annual rate of 1.8%—way above the 1.2% we expected.

- Fixed Investment: Zoomed in to 1.34% from a shaky -0.2%. This is the highest jump since Q2 2023 because the BEA finally gets data‑center spending right.

- Private Inventories: Boom‑split to 2.25%—a rebound from last quarter’s -0.84% dip. Anticipate the sale back down as businesses clear out their shelves.

- Government Spending: Went negative at -0.25%. First time Jordan (J) Biden’s favorite fiscal “plug” has pulled a trick and turned the lane into a slip‑slide.

- Net Trade: Major hero, clocking 4.830%—a drop from last quarter’s +0.26%. This was a double whammy: imports, especially gold, leapt up, nudging GDP by a nearly record 5.03%. Like inventories, it’s a “make‑up” if the tariff frenzy stalls.

Why It Matters

When you peel back the layers, the headline headline number was actually pocket-strong. The crash was just a side‑effect of two big boogeymen (net trade and government spending). If you wipe those out you get a big, bright picture that says, “Hold on to your hats, Vietnam, there’s hope!”

Slow‑Down Express

Inventory build‑ups and import spikes are printing like a season finale cliffhanger—big bump now, smaller after the tariffs stop buzzing around. Just like a blockbuster that’s still in post‑production, the real story will unfold in the next quarters.

Final Takeaway

So the takeaway isn’t that America is flailing, but that the economy’s plate is loaded with more than our usual number crunching edition—personal consumption, fixed asset growth, and, for now, a surge of gold imports. Keep this on your radar; the next quarter’s stats could flip the chart again!

Imports Take the Wheel in GDP’s Playground

Why Turns are So Crazy

Imagine GDP as a bored skateboarder. When imports spike, it’s like a sudden gust of wind—sudden, thrilling, and downright wild.

- Imports added a whopping 5.03% to GDP, ranking as the second highest spike ever recorded—just a shade of shy behind the COVID‑shock break‑dance.

- In a world free of economic shocks, that 5.03% would have stamped its own record on the quarterly charts.

Deflated GDP? Let’s break it down.

What the BEA Is Telling Us

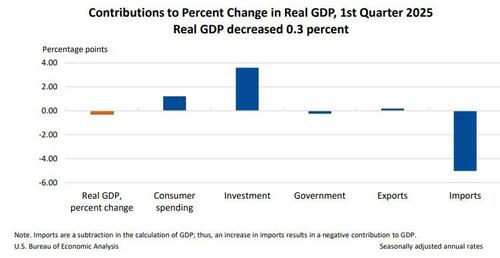

According to the Bureau of Economic Analysis (BEA), the drop in real GDP during the first quarter mostly stems from two things that pull the economy down:

- Imports jumpide up a notch. Every time we buy goods from abroad, that subtracts from the GDP tally—like a naughty subtraction in a math class.

- Government spending took a vacation. Less money flowing from the treasury means fewer jobs and less buying power.

But there’s a silver lining. Three friendly players stepped in to give the economy a boost:

- Investment. Businesses are still putting money into new projects and tech.

- Consumer spending. People are buying shoes, gadgets, and maybe a weekend getaway.

- Exports. Our goods are still getting a warm welcome overseas.

So, while some brakes are in place, the economy’s still got a decent amount of momentum.

U.S. Q1 Economic Update: A Rollercoaster of Numbers

GDP: The Big Picture

In the first quarter, the U.S. economy slipped a bit compared to Q4, largely because imports kept on rising, consumer spending slowed down a tad, and government spending took a hit. But guess what? Investment and exports stepped in to ease the blow, so the net result was a slight dip in real GDP.

Key Takeaways

- Imports up ↑ – trade deficit widening.

- Consumer spending ↓ – people are tightening their wallets.

- Government spending ↓ – less cash flowing into the economy.

- Investment and exports ↑ – business confidence and overseas demand are giving us a lifeline.

Inflation Surge: Prices on the Rise

The Bureau of Economic Analysis (BEA) reported a 3.4% jump in the price index for all domestic purchases in Q1, up from only 2.2% in Q4. The Personal Consumption Expenditures (PCE) price index lit up at 3.6%, compared to 2.4% last quarter.

Core PCE (food & energy excluded)

Even when we exclude the wild swings in food and energy, the core PCE climbed 3.5%, whereas it was 2.6% previously. In other words, the underlying inflation trend is still hot.

Hot vs. Expected

- GDP Price Index: 3.7% vs. 3.1% forecast – hotter than expected.

- Core PCE: 3.5% vs. 3.1% forecast – again, exceeding expectations.

The Bottom Line: A Shockingly Strong GDP

The GDP figure outperformed the forecast by a paltry 2.4% over the then-Atlanta Fed’s prediction—somewhat humorously, the number was so astonishing that folks started laughing at how lofty the forecast had been.

What does this mean for the future? If the outlier data points from Q1 are just a blip, the Trump administration could see a surprising rebound in Q2 or even Q3 as the economy corrects itself.

Quick Recap: What’s in It for You?

- Higher prices may dip your purchasing power but also show business growth.

- Investments and exports are a bright spot that could mean better job prospects.

- Keep an eye on the next quarter’s data—there’s a chance for a surprise upswing!