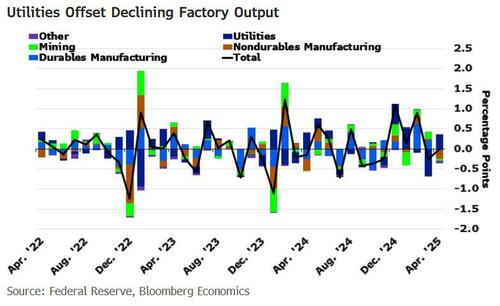

Industrial Production in April: A Mixed Bag

So, the latest numbers for April came in, and here’s the scoop: overall industrial production stayed flat. Not exactly headline‑grabbing, but it gives us a snapshot of how the economy is cruising through the spring.

Why the Numbers Stayed Steady

The secret sauce was utilities production. Think electricity, water, gas—those services that keep everything humming. When those service sectors do their thing, they can cushion a dip elsewhere and keep the overall index from dropping.

The Hit on Manufacturing

That slight wobble in the data was all about manufacturing production. It fell 0.4%, which isn’t huge, but it matters because:

- Vehicle output went down—fewer cars hit the assembly line, maybe because people’re waiting to see if the next model is worth the splurge.

- Nondurable goods took a dip—think household items and other things that don’t last forever. A slight slowdown in these goods can ripple through the retail sector.

What This Means For You

If you’re in the business of making, buying, or even selling stuff, expect the market to be a bit steadier than we might have hoped. The steady utilities sector is keeping the engines running, but a small slowdown in manufacturing could mean fewer jobs coming up in the car and household sectors—yet not an immediate recession sign.

Bottom Line

April didn’t break any records, but it did remind everyone that the economy’s trade‑off between steady utility output and a mild manufacturing decline is keeping things interesting. Stay tuned for the next update—maybe the next month will be a hit or a miss!

Manufacturing Production Takes a Dip: First Decline Since Oct 2024

Bloomberg’s latest snapshot shows a 0.4% slide in manufacturing output last month—after a surprise 0.4% bump the month before. This is the first fall in production rates recorded since October 2024, and it’s a bit of a shocker because analysts had sized it up at only a 0.3% dip.

What This Means for the Economy

Think of manufacturing like the heart of the economy—it pumps money, jobs, and confidence. A slowdown now hints that factories are packing less into their belting machinery, which could ripple through supply chains, inflate hiring forecasts, and dampen investor sentiment.

- Costlier Supply Chains: If production wobbles, suppliers and transporters feel the pinch.

- Job Market Impacts: A quieter factory floor can mean fewer hiring morsels for workers.

- Investor Mood: Equity blows can shift as corporate earnings outlooks adjust.

Why the Surprise Upshot?

Economists had pegged the fall at 0.3%, but the actual 0.4% tumble came out just a smidge heavier. The revision timeline looks like this:

- Month‑ago: +0.4% upgrade (good news, folks).

- Current month: -0.4% downgrade (bang, the flip side).

It’s like watching a roller‑coaster that once went up, now drops—keeping everyone on the edge of their seats.

Industry Voices

“We’re sorting out demand gaps,” says a supply‑chain manager who didn’t want to be named. “But the numbers tell us there’s a hiccup we need to iron out.”

Manufacturers broadly are trying to balance the delicate act of meeting consumer demand while juggling fluctuating raw‑material costs. The recent dip nudged them to re‑calculate their output plans.

Bottom Line

So, the manufacturing data released by Bloomberg isn’t just a line in a report—it’s a signpost indicating that the production engine might have taken a few sharp turns. While it’s unavoidable to feel a bit uneasy about the numbers, it also opens a conversation about how quickly adaptation and ahead‑thinking policies could steer the economy back on track.

April Economic Update: A Roller‑Coaster Ride

Production Takes a U‑Turn

Even though the charts paint a picture of decline, keep your eyes on the bright side: upward revisions lifted production by 1.2% year‑over‑year. That’s the biggest leap since October 2022 – a bold move that might just be a tactic to sidestep rising tariffs.

Sector Highlights

- Utilities – The power players saw a noticeable bump in output.

- Mining and Energy Extraction – Those heavy‑hitters took a dip, indicating a short‑term slowdown.

- Factory Output – A not‑so‑subtle drop in April, pinned mainly to reduced production of motor vehicles, computers, and apparel.

What It Means For You

Think of the economy as a big pizza: it’s still tasty, but some slices are thinner than others. Keep enjoying the crust (utilities) while watching the toppings (mining and factory goods) settle into their flavors.

Factory Capacity Takes a Hit—Now at 76.8%

According to the Fed’s latest report, the state of factory activity has slipped a little. Capacity utilization— the handy gauge of how much of a factory’s potential output is actually being used— fell to a solid 76.8%.

What the Numbers Mean

- Less than a quarter of factories are running at full tilt.

- Demand’s pacing down a notch, and supply chains still feel the drag.

- Overall output is a smidge below the long‑term ceiling.

Are We at the End of the Tariff‑Front‑Running Rollercoaster?

April’s slip in tariff‑front‑running has left many economists scratching their heads—does this mean we’re finally past the peak, or is it just a pause in the storm? Let’s dive in, break it down with a dash of humor, and see what it could mean for the “hard” data that keeps our markets humming.

What the Drop Actually Means

- Less “quick‑trade” behavior: Traders are pulling back from snagging deals before tariffs hit, so the wind’s a bit calmer.

- Signal of market maturity: A slower run of front‑running may hint that the hedge fund world is catching up to the underlying slow‑jam reality.

- Not a world‑end scenario: Markets still thrive on price discovery; front‑running is just one piece of the puzzle.

Will the Dip Drag Down “Hard” Data?

Hard data—like sales figures, shipping logs, or other hard‑core numbers—can feel the ripple of a front‑running slump but it won’t drown them. Think of it like a quiet glass of water; even if the surface is calm, the fish still swim deep.

- Impact on supply chain insight: Fewer front‑runs can smooth out distortions in inventory counts, potentially giving reports a clearer view.

- Information lag: Data still takes time to roll in, so the decline won’t flip the numbers overnight—a slow burn, not a fireworks display.

- Advertising edits? Not here. The torture of lost data improbable: throughput remains tight, especially for sectors less dependent on tariff timing.

Bottom Line

April’s downslide in tariff front‑running is less about doom and more about a natural adjustment. While it may fine‑tune market sentiment and peripheral hard data, the core figures—turnover, production, consumer demand—stay as robust as ever. So, breathe easy, friends: the market’s still churning, just a bit smoother.