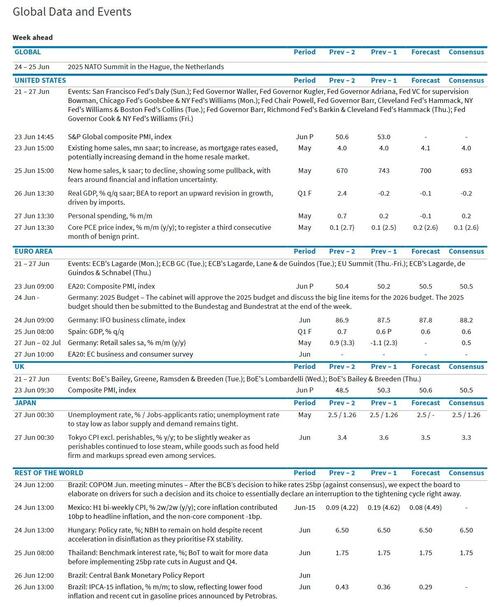

What’s Heating Up This Week

Grab your coffee, because this week’s news mix smells like fireworks, policy shake‑ups, and a dash of political intrigue. Here’s the low‑down—no fluff, all the highlights.

Israel‑Iran Showdown Takes the Spotlight

- Big‑time tension in the Middle East is the headline grabber. U.S. eyes getting involved, so everything else gets a second‑thought.

- While diplomats try to keep things calm, the rest of the world keeps watching. It’s like a live‑action drama with no script.

Doctrinaire or Dollar‑Sprinting? NATO’s Defense Bingo

- Defense Up‑the‑Retail – All NATO members (except Spain) are now committing to top‑lined 5% of GDP for defense. Spain is breathing easier, enjoying a handful of exemptions.

- The latest draft shifts the full spending spree from 2032 to 2035. Rutte had painted a faster, flashier picture that sent European stocks popping at the start of the year—now, the hype fizzles.

- Core military spending is 3.5% of GDP; the rest, covering infrastructure and cyber stuff, makes up the remaining 1.5%.

Financial Shaken‑On (Fed Edition)

- Powell’s June testimony is the usual go‑to; this time, it lands after last week’s FOMC—so expect less drama.

- Waller is back in the spotlight, echoing his dovish tone from Friday. He didn’t rule out a July rate cut, and markets are trying to guess whether he could be next Fed chief.

- Vice‑chair Michelle “Mike” Bowman joined in, calling for a July cut. Result? The dollar nosedived.

- Bottom line: the Fed is hinting that interest rates might see another dip next month—keep your wallets ready.

Back‑to‑Back Senate Sessions

- The “One Big Beautiful Bill Act” (OBBBA) is still in the mix. It could get a vote by week’s end.

- Key debates revolve around Medicaid, SALT cap reform, and the wiping‑out of clean‑energy tax credits.

- Economists still predict a 6.5‑7.0% deficit share of GDP over the next three years—no sudden radiation reversal.

China’s “Big Board” Moves in the East

- The NPC Standing Committee will run from tomorrow through Friday—think of it like the Chinese version of a boardroom meeting, but with less refreshments.

Brussels, Ottawa, and Somewhere Else

- EU‑Canada summit shakes hands on Monday (Prime Minister Carney present).

- EU leaders gear up for a weekend summit in Brussels—fewer coffee breaks, more policy decisions.

Market & Data Calendar (Because Numbers Matter)

- Preliminary June PMIs, U.S. existing home sales, Lagarde speech, U.S. consumer confidence, German Ifo, Canadian CPI.

- U.S. new home sales, Japanese PPI, Australian CPI, 5‑year U.S. Treasury auction.

- Final U.S. Q1 GDP numbers, durable goods, Chicago Fed, trade balance, jobless claims, 7‑year U.S. Treasury auction.

- Core U.S. PCE, personal spending/income, Chinese industrial profits, Tokyo CPI, French and Spanish CPI—give it a quick glance, because that PCE is the big fish in the sea.

In short, the week is full of policy moves, sharp market signals, and a lingering geopolitical drama that keeps everyone on their toes. Stay tuned, stay sharp, and keep your coffee handy—all that and more are unfolding as the world spins on.

June 23‑27: A Banking & Market Bonanza Calendar

Welcome to the whirlwind of July‑style economic updates. Below is your one‑stop guide to the top data releases, speeches, earnings, and auctions happening over the next five days. Grab a coffee — it’s going to be one busy week!

Monday, June 23 – The Pre‑Picnic Day of Prelims

- PMIs – The S&P Global shows the US manufacturing PMI at 51.0 (down from 52.0) and services at 52.9 (down from 53.7). European prelims are on the same track.

- Real Estate – Existing home sales in May jump 1.5% (beating a -1.3% expectation).

- Fed Fires: Waller, Bowman, Goolsbee, Williams, Kugler, and the ECB’s Lagarde & Nagel all give speeches. “Maybe we can ease rates soon,” says Waller – all eyes on July!

- Other Highlights – The EU‑Canada summit is on the docket.

Tuesday, June 24 – The Speech‑Heavy Tuesday

- US Consumer & Manufacturing – Conference Board’s June confidence hits 100.6 (beat 99.8). Philly Fed’s non‑manufacturing activity and Richmond’s manufacturing index set the stage.

- Housing & Trade – The FHFA April house‑price index stays flat. Japan’s April CPI receives a light touch.

- Reserve Central Bites: Powell toys with the House Financial Services committee, and the Fed’s big four (Hammack, Williams, Collins, Barr) rehearse their speeches. The ECB’s Lagarde, Guindos, and Lane join the chorus. The BOE’s Bailey, Greene, Ramsden, and Breeden also speak.

- Earnings Time! – FedEx and Carnival report their numbers.

- Auctions – 2‑year US notes are hawked at $69 bn.

- Other Events – NATO summit wraps up on June 25. China’s NPC stands by till June 27.

Wednesday, June 25 – Homeball and Tech Talk

- Housing Market – New home sales in May lag at -4.5% (but a +10.9% last month!).

- International Hotness – Japan’s PPI services tumble, Australia’s CPI rises, and China’s industrial profits stay bullish.

- Central Bank Debate – Bailey from the BOE paces before the Senate Banking Committee. Powell’s Senate testimony keeps the Fed’s policy in the spotlight.

- Earnings Spotlight – Micron Technology shares may soar with a new photolithography push.

- Auctions: The US 2‑year FRN reopens for $28 bn; 5‑year notes are minted for $70 bn.

Thursday, June 26 – The Durable Goods Showdown

- Durable Goods – Preliminary orders jump 15% (boosted by aircraft orders!). Core capital goods see small dips.

- Industrial Buzz – A $85 bn trade‑balance loss for May, only a modest inventory change.

- Jobs & Wages – Initial jobless claims sit close to 240 k; continuing claims hold steady.

- Fed Speeches – Barkin (RIA), Hammack, and the rest of the Fed chorus share their economic outlook.

- Other Highlights – Europe’s Council in Brussels keeps rolling.

- Auction – 7‑year US notes sell for $44 bn.

- Conference Highlights – “Economic outlook!” is the theme at the 2025 Agricultural Summit. (And Kansas City’s Schmid criticizes theory‑based easing at a recent panel.)

Friday, June 27 – The Personal Finance Finale

- Personal Income & Spending – Income up 0.3%; spending up a cool 0.1%.

- Core PCE – The index climbs 0.18% month‑over‑month (2.63% year‑over‑year). The headline PCE follows suit.

- Consumer Sentiment – Michigan’s final reading sits at 60.7.

- Fed Finals – Williams grooms a session on the BIS with Professor Reinhart. Cook & Hammack open a housing‑centric conference. The Fed’s DJ lineup finishes the week.

- Auctions: No new ones today.

Goldman Insight: The week’s major releases are: the durable goods orders and advance goods trade on Thursday, plus the core PCE inflation report on Friday. The Fed’s gala of speeches, especially Powell’s testimony on Tuesday and Wednesday, keeps everyone on their toes. The week ends with a noise‑free sleeping quality shot down to a “good place” for monetary policy.

That’s the full scoop. Stay tuned for more updates, and watch those FDIC‑at‑last quotas, ministerial techno‑drone speeches, and the roaring beast of trading volumes!