Economics: The New Roller Coaster

Soft Survey Data: The 2025 Winter Olympics of the Business World

Picture the latest Services PMI as that legendary movie premiere where everyone pretends to be excited, but folks are secretly sulking. The soft survey data that once had the economy humming just yawned its way into a dramatic, albeit still slightly mellow, slump.

Manufacturing: A “Weirdly” Weak Beat

Manufacturing PMIs had a day that felt like a bad karaoke night. Their numbers stumbled, choked, and politely asked, “Could we try again?” It’s no wonder a few factories left their windows open in hopes of a better breeze.

Regional Red Surveys: The Meteorological Calamity

The red surveys were a total disaster, similar to a city parade where the floats run out of paint. Analysts screamed “Yellow!” when they expected “Green!”—but the red reports remained stubbornly loud.

Labor Market: Still the Dancing Queen

Despite the survey slump, the labor market keeps the beat. It’s like that friend who always has upbeat playlists: jobs are still plentiful, wages are steady, and the “hard data” shows a workforce that’s oddly resilient.

- Jobs in growing fields are on the rise.

- Wage growth remains steady.

- Unemployment stays low.

So, while the surveys play cross‑words with the economic mood, the workforce is still rolling with its smooth rhythm—because reality is not always what the numbers say.

Quick Update on Services PMI: One’s Stumbling, the Other’s Soaring

Why the Numbers are Baffling

- Global Services PMI dropped from 54.4 to 50.8 in late‑April. That’s below the flash‑print 51.4 and the lowest figure since October 2023.

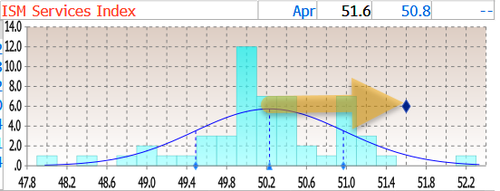

Bottom line: economies are still feeling the chill. - ISM Services PMI rose from 50.8 to 51.6, pleasantly surprising analysts who had pegged a 50.2 decline.

What’s the Takeaway?

It turns out the world of services is a mixed bag—some sectors are giving the world a thumbs‑down, while others are pulling up the flag with a hearty “yes!” And if you’re cleaning up the data mess, you’re probably thinking: “Is this a glitch or a prank?”

Final Thoughts: Baffle ‘em with Bullshit is Back

This just means analysts still love to keep the “bullshit” spin in the mix. Yes, it’s a bit of a joke, but hey, who doesn’t enjoy a little confusion amid the numbers?

ISM’s Surprise Performance

When the ISM print dropped, it gave almost every expectation a run‑around—only one forecast stayed close.

Why It Matters

- Almost all predictions were beat.

- Only one estimate stuck around, showing how solid the reading really is.

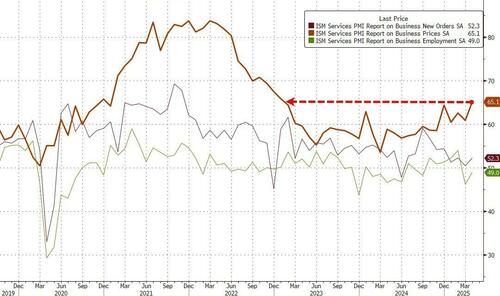

Prices Paid: The Sneaky Skew That’s Still Wearing a Pointed Hat

Under the hood, the picture isn’t exactly a sunny beach—prices have reached their highest levels since January 2023, while new orders and employment have only managed a modest bump.

Why the Numbers Feel Like a Bad Joke

- Prices Paid: 12‑month high, and they’re still climbing like that one coworker who can’t stop bragging about his new car.

- New Orders: A polite nod to the market—there’s more demand, but not enough to tackle the price summit.

- Employment: Slightly better than a rainy Monday, but not a full-on sunny Friday.

What We’re Really Seeing

While the data tells us that the economy is moving, mostly at a snail’s pace, those price hikes make it feel like we’re stuck in a long, expensive treadmill.

Bottom Line

The overall story is clear: inflation is still partying hard, and even minor improvements in orders and jobs can’t stop the party.

Economy’s Pulse: Services PMI Takes a Breather

Yesterday, the Services PMI was announced at 51.6 % for April, a subtle sign that the economy might crank out around a 1-percentage‑point lift in real GDP on an annualized basis.

Things Going Downward

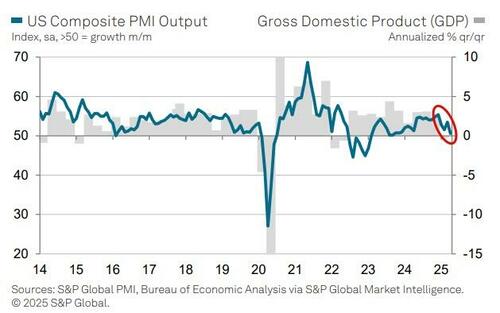

- All-in‑one S&P Global US composite PMI slid to 50.6 % in April, slipping from the March figure of 53.5 %.

- That puts the composite index down to its lowest level since September 2023.

What This Means for Us

It’s not a dramatic drop, but when all the big players in services are nipping at the heels of growth, you can feel the economy’s heart rate slow a trickle. Take a look at how this tiny slip might affect the lay‑off trends, consumer confidence, and the big markets already on the edge.

Bottom line: a modest dip in the Services PMI is a polite nudge that the economy may have some room to breathe—just enough to keep business leaders at a polite distance from the desperation crowd.

Inflation & Service Sector Slowdown: A Spicy Update

Why the Services Sector is Feelin’ Rough

According to Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, the latest tariff talks are doing more damage than just a manufacturing ripple—service businesses are starting to feel the heat too.

- Business Confidence Crumbles: In April, firms across the services arena saw hiring and activity inch toward a halt as confidence nosedived.

- Financial Services in the Crosshairs: Those dealing with money and clients feel the downturn biggest. They warn on “markedly weaker growth prospects” amid swirling uncertainty after new tariffs and ongoing federal spend trimming.

Export Woes & Domestic Doubts

Exports of services are plummeting faster than we’ve seen since 2022, yet the slump is not limited to international trade. Domestic demand’s also fading—confidence has leapt down the scale, dissolving what was once bustling.

Stagflation’s Sneaky Reveal

The manufacturing survey’s “stagflation” demons have begun to sip into services. The high import prices triggered by tariffs are inflating the operational costs for service firms, turning hell into higher consumer prices. Restaurants, hotels, and the like feel the burn most.

Bottom Line: The service sector is at a crossroads—either stalling growth or playing a vicious inflation loop that could leave the Fed frozen in its tracks for longer. Will it be a price‑rise loop or a spur‑in the policy pocket? Only time will tell.