Economy Gives a Surprise Knock‑Back

Just when everyone was ready to hand the recession a ticket to the front row, the latest numbers hit the market with a 0.7% month‑over‑month bump—way above the 0.2% bump that most forecasters had penciled in. Think of it as a snow‑man popping out of a pumpkin: oddly delightful and a bit hard to believe.

Why This Matters

- Consumer Confidence Rises – when spending looks stronger, people feel like they can actually buy something beyond the usual grocery list.

- Investor Sentiment Surges – markets love a sudden upside; it’s a cue for those trading on the breath of hope.

- Policy Discussions Shift – central banks might pause the rate hike countdown, because a healthier economy gets them to reconsider the rush.

Here’s the Bottom Line

Even a modest 0.7% rise feels like a pep talk for a sluggish economy: “Hey, you’re not dead, and you might just grow tomorrow.” The data isn’t a guarantee of a full-blown revival, but it does give analysts a brief pause to re‑examine their gloomy assumptions.

So if you were feeling a bit gloomy about the economic forecast, grab a cup of coffee. The numbers might just be the “cheerleader” you didn’t know you needed.

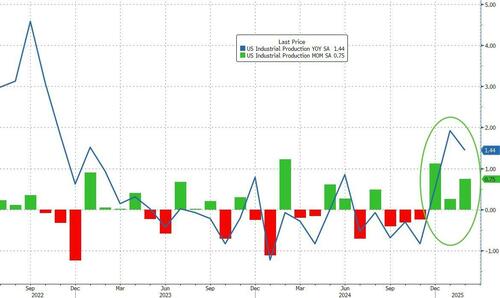

US Industrial Production Hits a New All‑Time High in February

When the economy gets a sudden burst of energy, the numbers love to show it. In February, U.S. industrial output shot up to an unprecedented peak, smashing the previous record from 2016 and proving that factories are still firing on all cylinders.

What the Numbers Tell Us

- Overall Output: 3.2 % jump – a sharp rise that outpaces most other sectors.

- Raw‑Material Consumption: 3.3 % rise – meaning more steel, plastics, and anything that gets turned into goods.

- Manufacturing: 3.2 % increase – from cars to computers.

- Mining, Oil & Gas: 3.8 % rise – the heavy hitters are keeping pace.

The key takeaway? The U.S. isn’t just back on track – it’s running laps.

Why It’s Not Just a Statistic

These figures matter because they speak directly to the working class, manufacturers, and the wider economy. A higher production level usually translates into more jobs, better wages, and a healthier balance of trade.

Outlook for the Rest of the Year

- Expect continued growth as firms ramp up production in response to rising demand.

- Watch for supply‑chain constraints that could temper the pace.

- Manufacturers are still shopping for parts, but inventory levels are improving.

In short, the numbers are smiling, and it’s a good sign that the American workforce is back in the groove again.

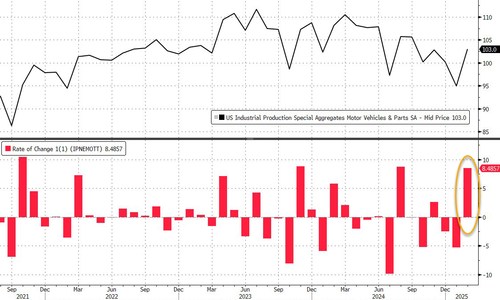

Manufacturing Mojo: The Bumpy Ride of 0.9% Growth

- Overall Output: Factory rooms are buzzing—production nudged up by a solid 0.9%.

- Motor Vehicles & Parts: The star of the show, this sector sprinted ahead with a jaw‑dropping 8.5% surge. Think of it as the automotive roller‑coaster that left everyone thrilled.

- Other Manufacturing: Even outside the car zone, things were moving. Non‑vehicle manufacturing grew by a respectable 0.4%, proving that there’s more than just engine reboots fueling the economy.

In plain talk: the industry’s gears turned faster, especially in car making, and that extra horsepower helped lift the whole market. The result? A brighter, slightly faster‑moving production landscape—like a well‑lubed factory keeps humming along.

Manufacturing Output Surges 0.9% in February

Good news for the industrial sector: US manufacturing output climbed by 0.9% last month, signaling a robust rebound from the downturn.

Durable Goods Lead the Charge

The durable manufacturing index outperformed at a 1.6% jump, reflecting stronger production of goods that last longer than a year.

What’s Driving the Growth?

- Motor Vehicles & Parts – The biggest contributor to the surge.

- Other Durable Categories – Nearly all sectors in this group ticked up, from electronics to industrial equipment.

Why It Matters

These gains suggest that businesses are ramping up production to meet demand, and that the economy’s backbone—its factories and workshops—are getting back on track.

Crunching the Numbers: February’s Manufacturing Beat

Grab a cup of coffee (or whatever fuels you) because the February manufacturing data just came out, and it’s a mixed bag of plots and profits.

Non‑Durable Manufacturing: A Quick Sprint

- Just a 0.2% lift – not a giant leap, but still better than the last month.

- Why it matters:

- Chemicals were the star performers, keeping the numbers up.

- On the flip side, the food, beverage, and tobacco segment slipped, pulling the entire group down a smidge.

Other Manufacturing: Slow‑Roll Decline

The publishing and logging sector saw a +0.1% drop. Not earth‑shattering, but it’s a reminder that the whole industry is still nudging sideways.

Mining Matters

- Big news: Mining output surged 2.8% this month.

- Remember: it was down 3.2% in January, so the swing back is pretty sweet.

Utilities Take a Dip

- The utilities index fell by 2.5%.

- Electric utilities slipped 1.2%.

- Natural gas utilities took the biggest hit – down 11.1%.

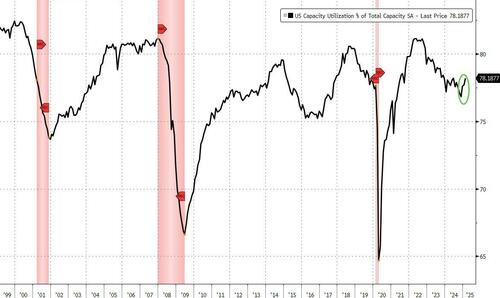

Capacity Utilization: The Rebound Booster

Despite the recessionary chatter, factories are filling up faster than expected. Capacity Utilization kept on rising, proving that the “slow‑down” signal might be a case of economics being a bit dramatic.

Overall, February’s figures paint a picture of a resilient manufacturing sector that’s navigating a rollercoaster of sector performances. Stay tuned for what the next month brings!

Why the latest Fed move isn’t a win for the doves

According to Bloomberg, the latest policy tweak won’t help the doves – those folks who are hoping for lower long‑term bond yields while Bessent and Trump are banking on a market that squeezes those numbers even tighter.

The key players in the yield debate

- Fed “doves”: The folks on the dovish side who want a softer stance and shorter rate cuts.

- Sales and political leaders: Bessent and Trump, who each have their eye on very low long‑term yields for a hotter economy.

In short, while slim sideways movements in the short‑term rates might feel like a win for the bird‑watchers, the big picture is that the strategy skim min against the very folks who would benefit most. It’s a reminder that policy moves can be a hit or miss, depending on whose agenda you’re looking at.

What this means for investors

For investors hoping to squeeze out some lower yields, the situation feels a little less hopeful. “It’s not exactly a miracle,” a market analyst recently said. “You’re still waiting for bigger pushes from the Fed’s side.”

Meanwhile, for the folks who want the policy to back them, there’s still a real hedge – the possibility that the Fed will play into a longer‑term yield trajectory that benefits their preferences.

In the end

Let’s just say the latest update has made the market cup feel a little more of a teapot. For some, it’s a sip of real hope, while for others, it’s just another reminder that politics and economics aren’t always in tow. Stay tuned – the next big move could change the playbook entirely!