Inside the Trump “Big, Beautiful Bill” (BBB)

Last week the Joint Committee on Taxation dropped a sneak‑peek of the House Ways and Means Committee’s mark‑up on the BBB – Trump’s grand financial fireworks. Even with a few stubborn ’says‑no‑to‑SALT‑deductions’, the bill is inching through Congress. Let’s break it down and see what this decade‑long tax overhaul might do for the U.S. economy.

Who’s pulling the strings?

The bill’s shape was largely steered by a Republican slim majority that’s taking the budget‑reconciliation route. Extending the tax cuts from 2017 (TCJA) isn’t going to bite the party hard – the majority is on board. The process also opened the door for extra goodies like:

- Domestic manufacturing credits – a little tax incentive for factories.

- “Tip‑tax” exemption – bartenders can keep their hard‑earned dollars.

- Some watered‑down versions of the promised IRA tax‑credit phase‑outs and cuts to social programs.

How do we measure the bill’s bite?

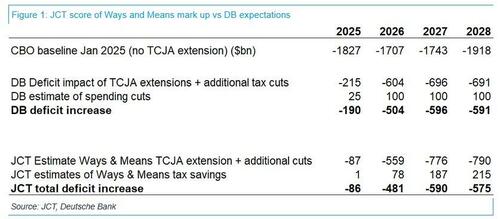

Think of the Ways and Means Committee as the tax code whiz. According to the Joint Committee on Taxation, the mark‑up could swell the federal deficit by $3.8 trillion over the next decade – most of that comes in the first five years. In the finer details:

- The bill pulls in $1.9 trillion in savings, but $1.2 trillion of that comes from the latter half of the ten‑year window.

- $915 billion of those savings stem from capping individual deductions for state and local taxes (SALT). Those numbers are likely to fall on‑hand when final tweaks happen, thanks to votes from high‑tax states.

- $560 billion of savings come from scrubbing or speeding up clean‑energy tax credits.

- $116 billion is earmarked for “remedies against unfair foreign taxes” – a pretty nebulous plan whose numbers are still fuzzy.

Where the numbers stack up against the big banks

DB, or Deutsche Bank’s Brett Ryan, had his own deficit calculations back in the day. While his earlier numbers differed slightly – especially around 2025 when he expected some cuts to be retroactive – the JCT’s latest score largely aligns with DB’s top‑line assumptions. The table below (in plain text) shows the comparison between DB’s prior estimates and the JCT score:

- DB’s 2024‑2025 deficit from tax and spending – $X trillion.

- JCT’s rollout – $Y trillion.

Bottom line: the BBB is a lot of plates spinning. While it promises tax breaks and certain savings in the long run, the upfront cost could widen the deficit for years. Only time will tell if the economic fireworks will light up the future or just flicker and fade.

Who’s Really Running the Numbers?

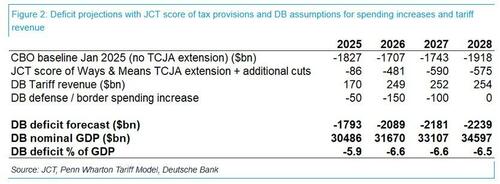

What the JCT Scores Miss

JCT rules in on revenue items, but it leaves out two pretty big steak‑pieces: tariff revenue forecasts and potential spending bumps. Those are the real drama in the fiscal plot.

The Ways and Means Committee Is the Tax‑Writing Hero

This committee is the mastermind behind every tax line in the bill. Unlike JCT, they handle all the revenue–related moves, from zero‑tax tricks to heavy‑handed tariffs.

Why CBO Is the Upside‑Down Final Scorecard

As the law-building story advances, the CBO will step in, doling out a fuller, sharper picture of both tariff gains and how the spending clock will tick.

What DB Melts Into The Forecast

- $300 bn in border and defense spending – front‑loaded and blazing over the next couple of years.

- About $250 bn in annual tariff revenue – enough to keep the coffers humming.

In short, the JCT score is like a chef’s starter notebook—great for the basics, but you’ll need the full menu from CBO to see the whole banquet.

What’s In It For You? The Tariff Trilemma

Two Sides of the Same Coin

- Higher Tariff Gains? If imports stay low and the tariff remains about 15%, the money streaming in could eclipse the current estimates.

- A Deficit Floor! The Ways & Means mark‑up, as recorded by the JCT, sets a baseline that hints at more deficit growth over the upcoming decade.

The Real Deal—More Room for the House and Senate to Rough It Out

Once the House and Senate settle the differences, the final bill will likely show even fewer savings than the draft suggested.

Bottom Line

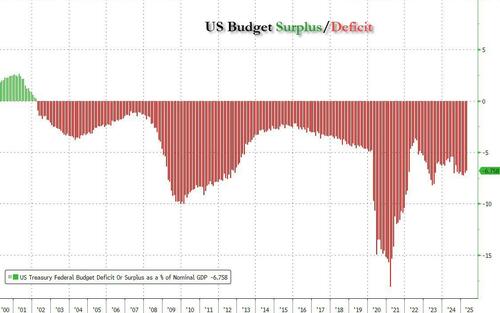

In short, according to the Department of Budget, there’s no serious effort being made to curb the historically high deficits that are on track to jump over 6 % of GDP in the coming years.

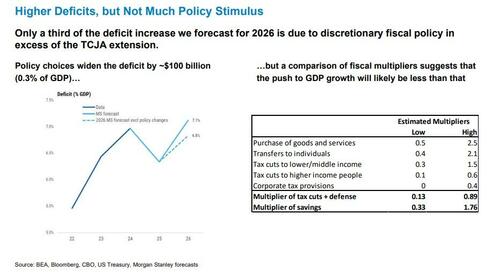

What Morgan Stanley Predicts for the 2026 Deficit

Picture the U.S. trying to secure a fiscal package that’s actually acceptable to both sides of the aisle. Morgan Stanley says the most likely outcome is a mix of tax‑cut extensions with a few incremental cuts, paired up with “pay‑fors” to keep the balance sheet from tipping.

Why 2026 Looks a Bit Bigger

- Sluggish economy – Growth is coming at a crawl, which means less revenue coming in.

- Higher costs – The current policy framework is stacked up with rising expenditures.

- These two factors are the “big drivers” behind a projected increase in the deficit.

Putting the Numbers in Context

Even after factoring in potential tariff revenue (which could quietly help the books), the bank forecasts:

- 2026 deficit: 7.1 % of GDP

- That’s a jump from 6.7 % of GDP in 2025.

- On the dollar scale, that translates to roughly $310 billion more than the previous year.

In short, the 2026 budget will nibble a few extra pennies off the baseline, thanks to slower growth and higher costs that the package can’t fully offset.

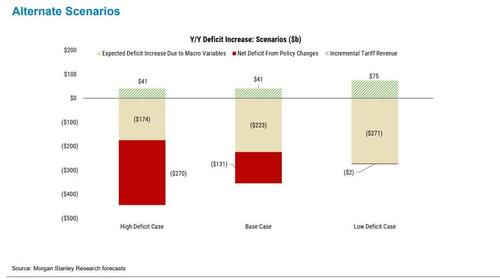

Bank’s Forecast – Two Deficit Playbooks

The financial pundits are throwing two different future‑scenarios at us. In one version, the deficit takes a big leap. In the other, it’s more… modest, even a bit of a “shh‑shh” the side.

Low‑Deficit Scenario (The “Whoa!” Moment)

In this storyline, the bank’s projections snag a +$400 B bump in the deficit. That’s like adding a whole four hundred trillion dollars to the pot of money—only the fund‑keepers get to see that kind of drama.

High‑Deficit Scenario (The “It’s Not That Bad” One)

Switching gears, the alternative storyline paints a less explosive picture: a +$200 B rise. That’s half the ballooning of the low‑deficit plot, but still enough to have the pundits raising their eyebrows in agreement.

Quick Takeaway

- Low‑deficit story: 400 B increase – a huge contribution to the deficit.

- High‑deficit story: 200 B increase – a more subdued, albeit still significant, rise.

So whether you’re a fan of the dramatic $400 B or the slightly calmer $200 B cliff, the bank’s telling the same story: the deficit is on the move, just under different band‑limits.

The Big Beautiful Bill: A Tax Tale of Twists and Turbulence

Picture the BBB as a grand extension of Trump’s original tax cuts—a shiny crown that’s just trying to keep the old perks alive. If that crown doesn’t find its spot on the throne, we’re looking at a hefty tax bump that could choke the economy, pulling the budget deficit down but simultaneously fanning the flames of a recession. The result? A stormy fiscal headwind that hits huge.

Deficits on the Dance Floor

Sure, the BBB throws a party for higher deficits, but the real rhythm it’s dancing to comes from a few sneaky spins:

- Record $1.2 trillion in gross interest—that’s like a giant debt jackpot, feeding the deficit avalanche.

- Economic slowdown—slow‑motion economy vibes that drain the budget’s candles.

So while the bill’s melody might sound like a stimulus tune, the real chorus will be quiet by 2026. Morgan Stanley already warned that even if we keep racing with the current policy, slower growth is bound to push deficits higher.

Why Growth Gets a Gloomy Glance

MS sees slowdown as the aftermath of a tighter policy whirlwind: more uncertainty, shifting trade rules, and a stricter immigration curtain. Still, it’s more a polite winding‑down of the Biden admin’s two‑year fiscal fireworks than a seismic shift. In short, softer growth means fewer tax coins in the coffers, and a bigger deficit balloon.

Crunching the Numbers

Here’s the kicker: only about one‑third of the deficit’s 2026 jump comes from discretionary moves beyond the TCJA extension. The rest? A mix of interest charges and the economy’s chill.

So, buckle up—if the BBB slips, expect a tax spike, a tighter deficit, and a recessionary ripple. If it holds, the budget may stay flat but the growth slowdown will keep the deficit at a brisk pace.

What the CRFB Says About the New Spending Package

Debt Numbers That Will Be On the Table

According to the Committee for a Responsible Federal Budget (CRFB), the proposed bill would tack on about $3.3 trillion to the national debt once we add interest. If the temporary parts of the bill become permanent, that bump climbs to a staggering $5.2 trillion.

Borrowing vs. Off‑Set Timing

The timing part is key: we’d be bleeding the money out fast in the first few years, while the offsets kick in later. That front‑loaded borrowing means people will feel the bite of the debt sooner.

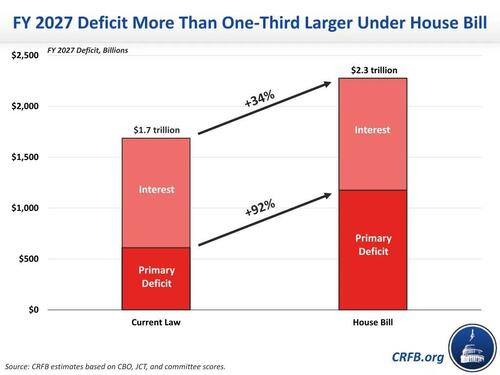

How the House Bill Affects the 2027 Deficit

- SBA’s estimate: $3.3 trillion added, but the CRFB thinks the bill will push the FY 2027 deficit higher by about $600 billion.

- That’s a 1.8 % hike of GDP and shows the bill would increase total projected deficits by one‑third, from $1.7 trillion to $2.3 trillion.

- The surge also cuts the primary (non‑interest) deficit in half, basically a jump from roughly $1.1 trillion to $2.3 trillion.

Net Borrowing vs. Offsets

In plain terms, the bill adds about $770 billion in new borrowing against only $180 billion of offsets. The net effect is almost a full $600 billion gap that will show up as a deficit boost.

Bottom line: with the timing of borrowing and offsets stacked this way, the short‑term deficits are going to feel the impact sharply, while the long‑term picture gets a less dramatic bump.

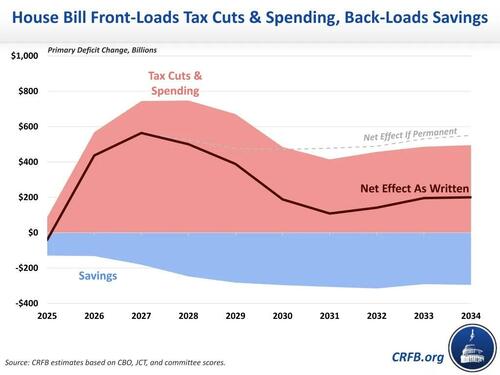

Budget Bill’s Front‑Loaded Spending Strategy

What makes this bill a bit of a curveball is how it schedules the money: the biggest cuts and new spendings are pushed front‑and‑center, while the offsets (the money that should eventually balance the books) are buried toward the end. Here’s the scoop:

How the Numbers Stack Up

- 55% of the gross deficit increase — that’s about $2.8 trillion — is happening in the first half of the budget period.

- Only 40% of the offsets, or roughly $970 billion, will be broached in the same timeframe.

- Consequently, a whopping 70% of the non‑interest borrowing kicks off in the first five years.

Why This Matters for Your Wallet

Think of it as a party where the host throws the biggest cake early on but promises to pay for the rest later. The front‑loaded approach might feel fresh and generous, but the lingering debt and delayed offsets mean the savings (or losses) won’t be settled until later, adding a hefty tax load down the road.

U.S. Budget: Premium Price on Quick‑Fix Clauses

When Washington is wiggling for a quick win, the price shows up somewhere else—usually on the next fiscal year’s scroll. The new House bill is basically a flurry of “quick‑pay” incentives that pop in now, hike debt, and fade out later. Let’s dig in.

Front‑Loaded Tax Cuts & Spending

- Child Tax Credit & Steady Deduction – Big boosts today, scheduled to vanish in 2028 or 2029.

- No Tax on Tips & Overtime – Lifesaver for workers, but only for a limited time.

- 100% Bonus Depreciation – Sparkles for equipment costs now, fading away just a few years down the road.

- “MAGA” Accounts – A novelty that pops off after 2027.

- Defense & Immigration One‑Time Appropriations – Must be spent by the end of 2029.

And if you thought that was all, there’s a whole set of retroactive windfalls—one‑time payouts for past actions that didn’t exist before.

Offsets That Take a Backseat

Money that saves won’t help soon enough. Picture a bank of savings at the end of a hallway:

- Medicaid Work Requirements – Might spare $300 billion by 2034, but the effect starts in 2028.

- IRA Energy Credits – Some are cut off at the end of 2025; the pricey ones taper off only after a few years.

- SNAP State Matching Funds – There’s nothing to be spent until 2028.

Put together, the mismatch means the bill will lift the deficit every year, except maybe 2025, because the front‑loads keep adding to debt long before the savings kick in.

Borrowing Hurting the Economy

The immediate spike in borrowing could push inflation and interest rates up well beyond what we’re comfortable with—especially if Congress extends the front‑loaded clauses or trims the offsets.

Yet, as unexpected as it might sound, the widened deficit for the next decade still represents a slower crash than the debt‑driven “life support” witnessed during Biden’s tenure. While the economy has been kept afloat by a cocktail of debt in the past, the new bill may keep the engine from idling for longer.

Market Sentencing & Dragon Tales

Bank of America’s Michael Hartnett highlighted a quirky “policy math” we can summarise as follows:

- US Fed funds rate: 2024 → down 100 bps, 2025 → flat.

- US spending: +$750 bn in the last 12 months; next 12 months? –$50 bn (FY26 proposal).

- Tariff haul: +$85 bn today; next 12 months → $400‑$600 bn (10‑15% duty).

- Tax cuts: potential $90 bn per year from the start of next 12 months.

- Cumulatively, a $0.2 tn increase from tax‑cut expansion + $0.7 tn in new cuts.

That swap of 100 bps cuts & $750 bn stimulus to a shrinking budget (spending cuts, tariff hikes, but no rate cuts) is a recipe for a 2025 slowdown.

Outside the U.S. – Where Are the Others?

China is still courting stimulus. NATO, meanwhile, set itself on a $100 bn annual rise in defence. To hit 5% of GDP by 2032, the 31 other members must contribute around $700 bn – with the U.S. currently hogging $0.9 tn in the NATO purse.

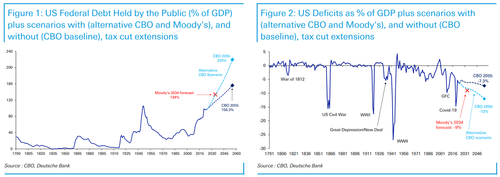

Moody’s Final Act & A Dark Forecast

A Friday downgrade of the U.S. Aaa rating didn’t come by accident—just when the “BBB” debate was heating up.

The key takeaways from Moody’s projections:

- Interest + mandatory spending will consume 78% of federal outlays by 2035 (up from 73% in 2024).

- Deficits will jump from 6.4% to 9% of GDP by 2035.

- Debt-to-GDP will hit 134% by 2035 (vs. 98% today).

- The “baseline” CBO numbers (excluding tax‑cuts) are mild. But add the tax‑cut extension, and debt/GDP will cross 200% in decades ahead.

The bottom line? Enough stimulus to keep the economy humming, but a debt‑roller coaster that might roll too far into the future.

The Real Story Behind “Savings” Claims Amid the Debt‑Burn Debate

When the idea of slashing government spending pops up, our instinct is to jump into the arms of the next big tech “hero” or any trending meme that promises a quick fix. But let’s cut through the hype and keep a clear eye on what really matters.

Why a “Cut” Is Only a Shimmer, Not a Solution

- Congress Rules the Agenda. Even if a charismatic entrepreneur wants to trim the billboards, the real power lies in the halls of the House and Senate.

- Recessions Are the Side Effect. Mass spending cuts can stir economic slowdown. And when that happens, lawmakers use the chaos as a springboard for emergency measures that often outweigh the original intent.

- The Debt Train Keeps Rolling. From a “fast passing of funds” angle, the long‑term trajectory of national debt remains largely untouched if the legislative body stays in its comfortable rhythm.

Elon Musk and the “Doge Saving” Narrative

Remember the tweets from early February that praised Musk’s attempt to “streamline the government” with a DOGE‑based savings plan? They promised a clean break from traditional budgetary knots. The reality, however, was more nuanced.

“The Doge saving goal of $2 trillion depends on congressional support and the overall executive backing.” – Elon Musk (May 20, 2025)

In plain words: the Doge team is no longer an autonomous monarch of fiscal policy. They’re advisors, not chief executives. Their big project is ill‑fated unless it gets a thumbs‑up from the lawmakers who ultimately write the budget.

Key Takeaways for the Everyday Citizen

- High‑profile tech antics can add sparkle to financial talk, but they rarely change how money is actually spent.

- Stubborn bipartisan politics keep the debt ladder intact, regardless of any well‑intentioned savings plan.

- When government spending gets trimmed, a recession can creep in – and lawmakers may use this slump as a cover for new policies.

From Cambridge, the CRFB and big banks – Deutsche, Bank of America, and Morgan Stanley – the full notes show the same story: the savings movement is fuzzy, the debt situation stays robust, and the only real mover remains Congress. No matter how flashy or contagious a tech‑based “cash‑saving” idea becomes, it must fit into the larger political & economic structure to succeed.