Head‑lining the China Craze? Let’s Take a Candid Look

A recent jab from Kyle Bass, the hedge‑fund maverick, highlights a stark truth: China’s economic “dream” is slipping faster than a banana peel on a slick floor.

The Billion‑Dollar Reality Check

- “We’re witnessing the largest macroeconomic imbalances the world has ever seen, and they’re all coming to a head in China.”

- Turning the dream into a nightmare is no accidental side‑effect.

What’s Going Wrong?

Think of China’s economy as a symphonic orchestra that once played a flawless tune.

- Mis‑guided policies – like inserting a trumpet in a violin section.

- Systemic financial rot – “deep‑state” debt storms that make a dry lake flash bright.

- Growth engine fizzles: the horse that once trotted fast now has a confused “I‑don’t‑know” look.

Why It Matters (And Why It’s Not Just a Bummer)

Anything that slumps in China isn’t just local—global markets feel the tremors.

- Investor confidence takes a nosedive.

- Supply chains experience the knot-the-tying equivalent of a holiday traffic jam.

- Who ever thought China’s “superpower” status would be a fable?

In summary: China’s saga is not a suave saga, but a cautionary tale—one that a savvy investor like Bass suggests we all plan for.

China’s Economy: The Roller‑Coaster No One Can Catch

When Bass drops the mic, he’s got the whole scene in view…

Key Takeaways

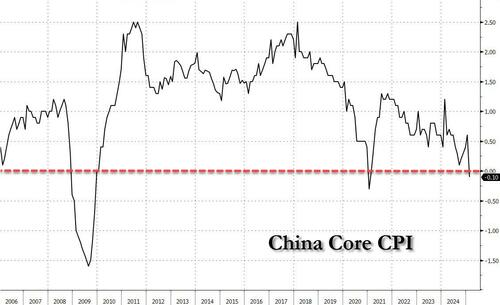

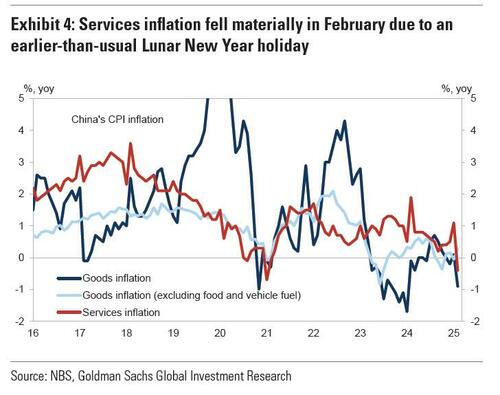

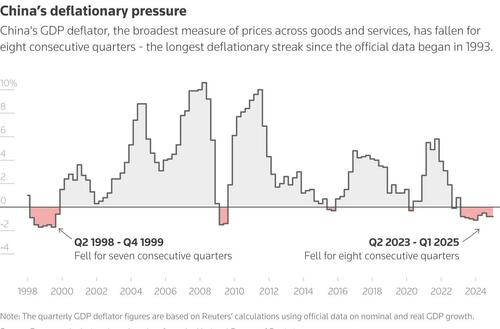

- GDP deflator keeps sliding. Prices falling across the board, while the economy is taking a nosedive.

- No end in sight? Bass says it’s a spiral that feels like a never‑ending loop‑the‑world dance.

- The rule‑breaker in the market. The deflator and activity are in a mutual dissolution mode, leaving economists scratching their heads.

Feel the Vibe

Picture a carnival ride that keeps spinning faster and faster, with nobody inside the cart. That’s basically the current story: a economy doing the “infinite loop” routine — and nobody’s got a stop sign.

Humorous Touch

Imagine your favorite coffee shop suddenly offering made‑to‑order mugs that drip—every cup’s a rookie’s first mistake. The market’s same vibe: things are dropping, and the world’s watching, holding its breath.

Your Portfolio Might Feel the Ripples

Imagine the world’s biggest economy—China—suddenly tipping. Investors worldwide won’t just shrug; they’ll shift their money like a busy stockroom. Why? Because when a giant economy stumbles, the capital doesn’t disappear— it travels!

What Movements Mean for U.S. Investors

- Capital Re‑flows: Cash that once danced in Chinese markets is now hunting safe harbor in U.S. dollars and Treasury bonds.

- Risk Re‑assessment: The spike in concern isn’t just market chatter. It’s a full‑blown re‑evaluation of how risky investments feel.

- Global Impact: Even local U.S. assets feel the tremor, so keep an eye on portfolio weights.

Quick Takeaway

Don’t treat this as a remote story. It’s a seismic macroevent that can swing the very markets you’re invested in. Stay informed, stay prepared.

China’s Backstory

China’s Real‑Estate Hangover: Why It’s Not Just Housing

When the real‑estate pressure cooker in China goes off, it’s not only a wall‑paper crisis—it’s a whole economy getting a stern squeeze.

600‑million Empty Chapters

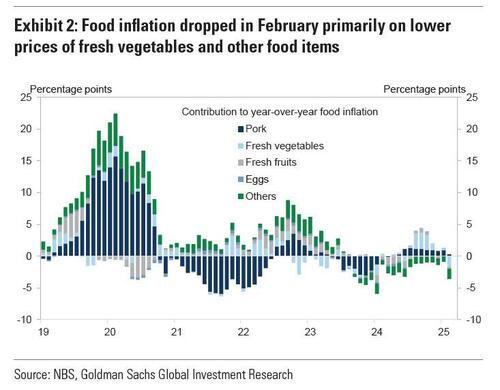

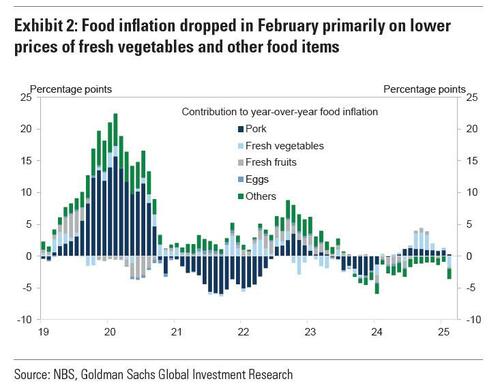

Think of the country as a gigantic book where 600 to 700 million chapters are left blank. Those are the “ghost cities” that sprung up after the financial crash. Bass throws it in a casual analog: “It’s a Ponzi scheme that’s finally collapsing.” That’s the visual. The sheer scale of that over‑build is no secret. Developers are dropping debts like call‑outs from a debt‑free class, sales numbers slam‑sdown, and home prices take a nosedive in the major metros.

When the Bubble Pops

The bursting impact is two‑fold. First, the bubble’s ripping is gunrocking deflationary fire—prices are going down faster than a garlic press. Second, the valuation of shadow‑bank collateral is plummeting, and that means the entire banking ecosystem’s linchpin is shaking.

China’s Tight‑Fisted Response

- Reforms that could bring transparency and market discipline? Hands‑off from the CCP.

- Government chooses to tighten the purse strings—capital squelching, state interference, and a microscope over every financial move.

In other words, Beijing isn’t earning a sequel—it’s putting the brakes on the market’s natural way of clearing out.

Capital Flight: The Inevitable Highway

When the capital starts to swerve out, it will do more than just scratch a surface; it’s a deep bath on American finances and markets. Bass sums it up like this: “China is experiencing a slow‑motion banking crisis, and capital is doing everything it can to escape.” The stakes are high, while the journey is only just beginning.

Capital in Search of Safety

Why the Dollar Is Not Going Anywhere

When people talk about an exodus of capital—both from the U.S. and abroad—it’s tempting to imagine the whole global economy doing a dramatic flip‑flop. We’ve talked before about how the so‑called “Death of the Dollar” story is basically a bad copy of a blockbuster movie. But if you ask a few key questions, you’ll see why the U.S. currency still has the “golden ticket” advantage.

1. No One’s Ready to Take the Lead

Fingers crossed for a new superstar currency like a GigaEuro or a “Northern Dollar” that’s got a 5‑year runway, but the reality is: all the dollars that matter—government debt, corporate bonds, international trade—are still issued and linked to the U.S. The gaps are too huge to fill.

2. The U.S. Economy Is Still the Heaviest

Think of the U.S. economy as a weight‑lifting champion. It’s big, it’s strong, and it can keep a steady pace even when the global financial world starts pulling their weight. That’s why markets keep favoring the dollar.

3. Network Effects and the “Stickiness” of Finance

When you’re in a town where everyone pays with your local currency, it’s super hard to switch to a new one—you’ll have to retool everything from ATMs to accounting software. That’s exactly how the global financial infrastructure is stuck with the dollar. The inertia is massive.

4. De‑Dollarization Is a Whole Lot of Work

Even countries that dream of moving away from the dollar have a limited toolkit. Steps include swapping debt denominated in dollars, finding reliable alternative reserves, and convincing businesses—yes, even pizza shops—to accept the new currency. The sausage roll of this transformation is thin.

5. Resilience in the Face of Policy Shifts

Even when the U.S. changes its monetary policy—tightening, easing, or just playing around—the dollar doesn’t break the bank. The currency’s resilience keeps it afloat, much like a lifeboat that’s not just a novelty but built to withstand every storm.

Bottom line? The dollar sits at the top of the global transaction ladder. It’s not just money; it’s the architecture on which commerce, debt, and confidence are built. So, while it’s great to stir the pot, the headline should little be written: the $ is still the reigning champion.

When China’s Economy Takes a Tumble

Every time China’s economy stumbles, the world’s craving for the good ol’ U.S. dollar only ramps up.

Safety Over Yields

In a crisis, investors don’t chase high-interest rates; they chase security. Think of it like swapping a roller coaster for a cozy armchair during a storm.

The U.S. Dollar Still Reigns

- Even though the U.S. is juggling massive fiscal deficits and debt, the dollar remains the go-to global currency.

- U.S. Treasury bonds act like a fortress of faith, offering depth, liquidity, and a trust level that’s unmatched.

- No other asset can claim the same level of safety for a worldwide market.

Bottom Line

With China’s economic hiccups, the world’s reliance on the U.S. dollar only grows stronger—proof that in the grand theater of finance, the dollar still has the spotlight.

The Dollar Is Set To Rise

Capitals on the Run: Why the Dollar Is on a Winning Streak

What’s Really Going On

- When investors start pulling money out of China and other high‑risk spots, the U.S. dollar gets a big boost.

- It’s not just a shiny theory – the trend shows up every time a crisis hits.

The Pattern in Action

Here’s the rundown of the big moments that have given the dollar a kick‑start:

- Global Financial Crisis – Investors eyed the solid footing of American finance.

- Eurozone Debt Crunch – A scramble to find a safe haven pulled dollars in.

- COVID‑19 Pandemic – Uncertainty made the U.S. dollar feel like the ultimate “calm” option.

- Russia/Ukraine Conflict – The world’s chaos prompted a sharp rally in the greenback.

Bottom Line

Every time global markets get shaky, the U.S. dollar steps up as the “safe‑haven” of choice, and the numbers back it up. Whether it’s a pandemic or a political showdown, the dollar’s got a front‑row seat in the global economy’s ups and downs.

Where The Money Goes When The World Gets Hot

In a nutshell, when investors start tossing their cash over the Atlantic clock and the world’s finance dial switches to the U.S. dollar, the default first stop is the great U.S. Treasury. Think of it as the rain‑forests of debt markets—tall, deep, and the place where the trade never stops.

Why Treasuries Are Winning The Money Battle

- Liquid Gold – They’re the most liquid sovereign debt out there, so you can buy and sell them instantly like a vending machine that never runs out of snacks.

- Safety First – With the U.S. backing, they feel like a future‑proof insurance policy for your portfolio.

- Depth Matters – The sheer size of the Treasury market is enough to make other markets feel a bit shallow.

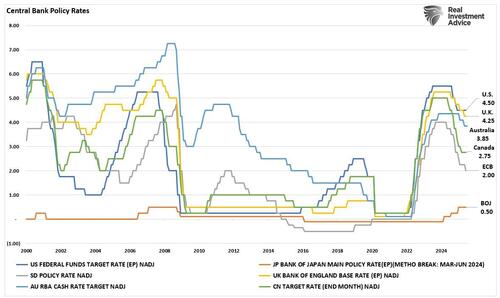

Central Bank Rate Cuts: A Speed‑Bump on the Global Road

Across the globe, central banks are pulling the brake pedal at breakneck speed. The European Central Bank (ECB) has cut rates eight times this cycle, while the Federal Reserve is sitting on the sidelines, playing it safe.

What that means? The yield gap between U.S. Treasuries and European bonds (like the German Bund) is widening like a gaping canyon. You’re looking at a dove and a hawk—one webbing for walking and the other for a quick hop across.

Bottom Line

When the world’s capital suddenly goes all in on dollars, it finds a comfy home in U.S. Treasuries because they’re reliable, liquid, and big enough to handle the influx. Meanwhile, Europe’s rate‑cutting spree creates a divergence that keeps investors on their toes. So, keep an eye on those yields—they’re telling us who’s grabbing the cash and who’s handing it out.

Why Treasury Yields Matter to Investors (and Why You Should Care)

Picture the financial world as a bustling market. Investors with a little extra cash are always on the hunt for the best spot to park their money. Treasury bonds? They’re the heavyweight champ of that market, especially when your wallet is looking for safety.

1. Higher Yields = More Cash Inflows

- When Treasury yields rise, the coins flow in—just like a new ice‑cream truck attracting crowds.

- Investors sniff out those sweet returns and pile on the dollars.

2. Treasuries Keep the World’s Money Stores

Foreign governments love holding U.S. Treasuries. They’re the Go‑to prize for storing value—think of them as the international e‑wallet you can’t help but trust.

3. The Yield Gap Favors the Dollar

- Yield differences act like a magnet for the dollar, helping it strengthen.

- That’s because the higher the yield gap, the more investors chase the U.S. currency.

What Happens When Demand Goes Up?

Good question! As more people chase Treasuries, prices shoot up, and yields step down—this is a classic supplyanddemand dance. Imagine a crowded concert: The louder the crowd, the higher the tickets, but the price per seat might fall.

But What About the U.S. Excess Debt?

Even if the U.S. floods the market with new debt to pay for everything—think of a massive house party—foreign demand can still keep the price from crashing. It’s that counter‑balance that keeps Treasuries on solid ground.

When the Global Scene Gets Bumpy

In a calm, predictable world, more Treasury issuance would normally push yields higher. But if the second‑biggest economy starts crumbling and trust in its banking system evaporates, that dance changes.

- Investors no longer chase the high returns.

- Instead, they’re whipped around by the promise: “Your money stays there, and you’ll get it back.”

Key Takeaway: Preservation Over Growth

It’s a big clue—investors are moving their money not to chase flashy growth but to secure a reliable return. Shifting from “growth hunting” to “preservation mode” can ripple across the entire market, cranking up volatility and changing the game for all.

Bottom line: Don’t underestimate the pull of Treasury bonds. They’re not just a dull storage unit; they’re the safest, most trusted ride in a world that’s sometimes wild and unpredictable. Stay tuned, stay safe, and keep your eye on those yield pools!

China’s Deflationary Impact on the U.S.

The Ripple Effect on the U.S. Economy

Picture this: The U.S. has been riding a giant wave of China’s rise for the past two decades, cashing in on what economists call “export inflation” and “import deflation.” In plain English, our companies got to ship big‑time, taking advantage of Chinese cheap labor, a growing middle class, and an appetite for every commodity and gadget under the sun.

China as the Ultimate Trade Sidekick

- From heavy‑duty machinery to chic consumer brands, China became the go‑to partner for U.S. exporters.

- It also played a crucial role as a reliable marginal buyer and a solid production partner in our supply chains.

What Happens When That Engine Slows Down?

When China’s economic engine starts to sputter, U.S. multinationals feel the heat. The consequences? Lower global trade, reduced demand for U.S. goods and services, and a slowdown in foreign investment flows. Even if our own consumer habits stay strong, the drop in international business will drag down nominal GDP growth.

Market Sentiment Takes a Hit

Investors are already pricing in a steeper slowdown. The expected terminal growth rate for the U.S. economy is going to dip, especially in sectors that have a hefty slice of international demand.

Exporting a Deflation Storm

China’s slide into deflation can spill over worldwide, putting a wrench into global inflation dynamics. This looming threat may even reinforce the idea that the Fed’s recent move was a “Transitory Mistake.”

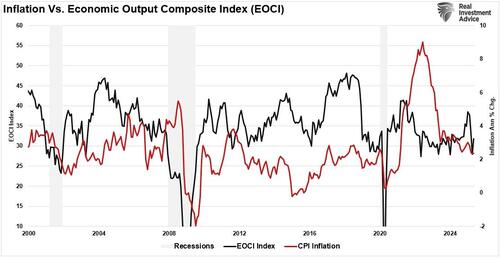

Why the Economic Composite Index Matters

The Economic Composite Index stitches together almost 100 hard and soft data points. After the post‑pandemic boom, growth is on a downward slope. Since inflation hinges on supply and demand, it’s no shock that it’s cooling right along with the economy.

US, China and the Great Deflation Tango

The U.S. is importing deflation from China, and the real test of how much it will hit our economy is coming up in the next data releases. Think of it like a slow‑moving wave of price drops gradually rolling across the river.

Why the Ripple Matters

- The ripple isn’t a one‑time dip: we’re looking at a continuous slide toward zero or even negative real growth.

- According to Investor Bass, it’s more than a simple downturn; it’s a permanent shift.

What This Means for China

China’s exports to the U.S. are the levers behind this slow slide. If the flow of goods continues to undercut domestic prices here, the global supply chain will feel the pressure.

Policy & Investor Takeaways

- Policy Shifts: Think import tariffs could tighten, but trade agreements will need a rethink.

- Investor Outlook: Growth forecasts will need a major recalibration—expect the next decade to look more like a data stew than a predictable chart.

The Bottom Line

Don’t let the numbers fool you—this is a long‑term game and it’s gonna reshape how China and the U.S. play the economic board. Stay alert, stay flexible, and maybe keep a snack stash handy for those inevitable price dips!

Conclusion

When Guarding Your Wallet Beats Quick Wins

In today’s patchwork of economic signals, the old‑fashioned playbook of chasing growth, boosting productivity, or pumping capital into the next big thing has lost its edge. Investors are swapping the mantra “Where’s my next big return?” for “Where’s my next safe haven?”

The U.S. Treasury Gathers the Crowd

Despite a stubborn deficit and the ongoing political standstill, capital keeps flocking to the U.S. Treasury market – the clear winner over any other headline‑sticking asset. It’s a hard look at how confidence trumps ideology: “Money doesn’t care what you fancy – it cares about trust, liquidity, and the rule of law.”

When Trust Breaks, Money Runs

Picture the trust in a giant economy like China suddenly evaporating. In that moment, the money that once lingered in those markets doesn’t just tiptoe – it sprints to safer ground.

Why the U.S. Continues to Shine

While the United States faces its own set of structural hurdles, the Treasury market still stands as the cleanest, most reliable choice among today’s dirty laundry. This is not a short‑term swing; it is part of a deeper realignment of global economic leadership and a threshold for risk tolerance.

- Trust in a country drives its investment appeal more than politics.

- Liquidity and clear legal frameworks are the new currency of safety.

- Even with fiscal deficits, the U.S. Treasury remains the go‑to safe harbor.

Stay Ahead This Way

Want a deeper dive or actionable ideas to protect your capital? Keep track of market shifts, update your strategy, and stay ahead.

Ready to turn protection into profit? The path is clearer with the right insights.