Today’s CPI News: A Look at the Prices That Hit the Daily Grind

When we talk about the impact of new tariffs on the everyday American, the Consumer Price Index (CPI) is the barometer that tells the real story. Today’s numbers came in, and here’s what they’re telling us.

Why the CPI Matters

- Tariff jokes are passing reality – Every time the tariff hammer swings, it stones the prices we pay.

- The “pass‑through” theory – Old economists foretold that the tax shock would climb into the consumer bills.

- Getting ready for the big revelation – Analysts had been whist‑ting about a spike waiting to hit the market.

What Today’s Print Shows

- Modest rise, not a tsunami – The CPI ticked up, but not to the level some spotlighted.

- Inflation measured on everyday goods – From groceries to gas, the image is a little higher, but still in a reasonable lane.

- Evidence of “tariff terror” being real – First peek that the cost of tariffs is moving down to the wallets of normal folks.

Key Numbers

Here’s a quick snapshot of the numbers that hit today:

- Overall CPI increase: 0.2% month-over-month.

- Core CPI increase: 0.4%, excluding volatile food and energy.

Takeaway

The CPI’s modest jump may be a sign that the tariff backlash is leaving the way it intended – to offend the average American budget. While the numbers don’t blow up the charts, they keep the “tariff terror” narrative alive, block to block, and price by price. And if you’d thought the impact was only theoretical, this print is proof that reality can sometimes be less shocking, but still surprisingly real.

Higher Prices

Inflation’s Whimsical Dance: Prices Aren’t Stuck in a Rut

Quick recap: The market’s been throwing a few surprises our way, but the headline take‑away remains a “nothingburger.” Let’s dive into the numbers and see the dance behind the dance.

Manufacturing Speaks Up

- ISM Manufacturing Prices climbed to 69.8 – the highest spike since June 2022.

- Manufacturing firms in the US (S&P Global) saw the biggest price surge for output since early 2023.

- Kansas City Fed’s “manufacturia” hit 29 (up from 15 in March), showing the industry’s appetite for higher price tags.

- Dallas Fed’s finished goods prices rose to 14.9 from 6.3 in March – a jump that made many factories smile.

Services – The Unpredictable Sidekick

- ISM Services ticked up to 65.1 in April – the largest rise since January 2023.

- Dallas Fed’s services selling prices climbed to 8.4 from 5.2 the previous month.

- New York Fed, Philadelphia Fed, and Richmond Fed all pushed their manufacturing price receipts higher, indicating that the entire sector is feeling a bit of upward pressure.

Fed Reports Taught the Beats

Across the banking hubs:

- Richmond fell in March but then rose to 2.65.

- New York sharpened its edge to 28.7.

- Philadelphia slipped a touch, now at 30.7.

- Kansas City’s non‑manufacturing selling prices also ticked upward.

Chicago’s PMI (Purchasing Managers Index) – The Surprise Party

The Chicago PMI revealed that prices in the city bounced faster than expected, giving investors a glimmer of optimism.

Fashionably Slow CPI (Consumer Price Index)

In the grand finale:

- Headline CPI rose just 0.1% month‑over‑month in May, slightly shy of the 0.2% forecast.

- Year‑over‑year, it nudged up to +2.4% (up from +2.3% in April).

So, what’s the verdict? The inflation story feels like an “invisible” episode – no dramatic fireworks. Prices are creeping up, but not at a blazing speed, and the market sweetly keeps its expectations in check.

Energy’s Outing Has the Economy Feeling Flat

Last month’s Consumer Price Index (CPI) released by the Bureau of Labor Statistics came with a surprise twist: energy prices are on a deflationary decline. That bite saw the headline CPI dip, giving economists a brief breather from the inflation roller coaster they’ve been riding.

The Numbers in a Nutshell

- Headline CPI (YoY): 3.2% (down from 3.6% last month)

- Energy Deflation: 4.5% drop in oil & gasoline combined

- Core CPI (excluding food & energy): 2.8% (steady)

- Core PCE (used by the Fed): 2.3% (still under the 2.5% target)

Why Energy’s Drop Matters

Energy—fuel for cars, homes, and industrial power—often drives the headline inflation narrative. When those prices slump, it lightens the overall inflation burden, even if core inflation read just on the same track.

Policy Implications in 15 Seconds

- Fed’s Rate Puzzle: Does the drop mean a pause? Not necessarily. Core measures still show creep.

- Market Mood: Markets get a sigh of relief, but they keep eyes on core metrics.

- Consumer Confidence: Lower gas prices* lighten wallets, yet the broader price increase still lingers.

What the Analysts are Saying

Some economists are cheering, “It’s a win for the average shopper, at least for a moment.” Others caution, “Keep your eyes on core inflation; energy’s back slide is a blip, not a trend.”

Bottom line: Energy deflation has technically smoothed the headline CPI, but core inflation keeps the Fed’s focus on a steady climb to its target. The economy might get a tiny breather, but the long‑term view remains intense.

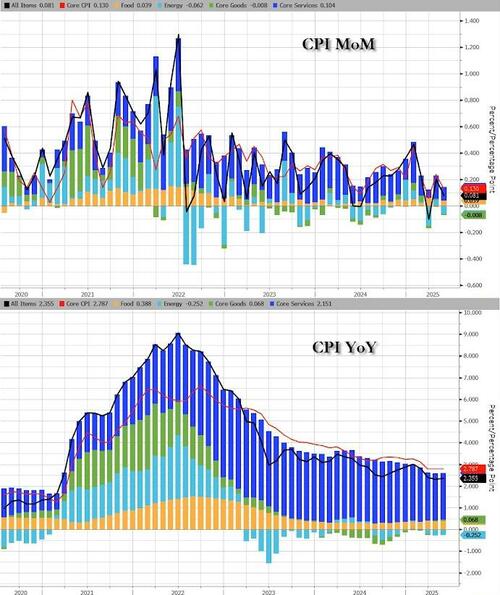

May Readings Show the CPI Just Stalled

What the Numbers Tell Us

The Consumer Price Index (CPI) nudged up by 0.1% this month—only a slight lift after a 0.2% push in April. Over the past year (12‑month snapshot), the all‑items index climbed 2.4% before seasonal adjustment tweaks.

Key Sectors That Broke the Mold

- Shelter rose by 0.3% and was the main driver behind the monthly bump.

- Food showed a stronger shift: both food at home and food away from home ticked up 0.3% each.

- Energy slid 1.0% largely because of a slump in the gasoline segment.

- Positive vibes came from medical care, motor vehicle insurance, household furnishings, personal care and education—all ticked upwards.

- On the flip side, airline fares, used cars & trucks, new vehicles, apparel were the laggards, posting declines.

Year‑Over‑Year Snapshot

The full‑year CPI is up 2.4% as of May—just a hair higher than the 2.3% achieved in April. Excluding food and energy, the index jumped to 2.8% over the same period. Energy’s 12‑month run has brushed down 3.5%, while food has leaped 2.9%.

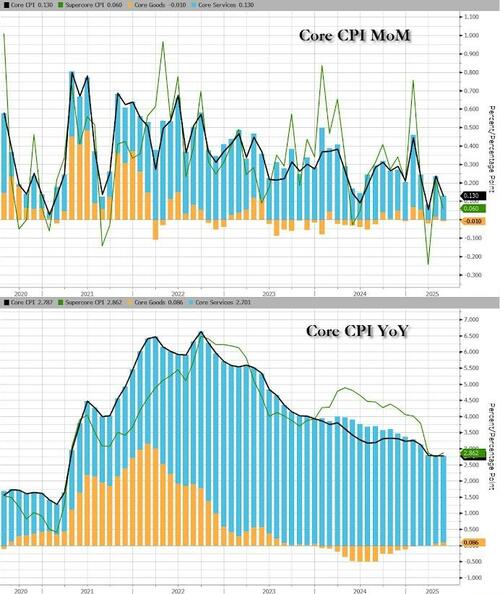

Core CPI: The Most Unexpected

Core CPI—which strips out the most volatile items—only rose 0.1% month‑over‑month, well shy of the +0.3% people had hoped for. Its year‑on‑year figure stayed flat at +2.8%, the same as April, and is the lowest since March 2021.

Bottom line: The measured pace of inflation has settled into a mild freeze, with shelter and food pulling the weight, while energy and a few other sectors keep pulling back. Analysts predict the months ahead will likely stay in a similar zone of calm.

Price Drop Alert: Consumer Goods & Housing Costs Take a Hit

In a surprising turn of events, the big march of inflation has slowed down this month, especially for the stuff we buy every day. Packed with details and a dash of humor, here’s what the latest CPI analysis tells us:

What the Numbers Are Really Saying

- Goods prices fell 4.0% YoY. That means for the first time in a while, the big deflationary wave hit goods—think groceries, clothing, and gadgets—so folks can keep that wallet happy.

- Amid all that, housing (shelter) is still stubborn. Savings are still being hiked toward a logical range of 2‑3% for the next quarter.

- While the foods & beverages mix was largely sticky. The big list includes everything from dairy to desserts, it’s still holding its own but weakened a bit by food costs.

Households: Finding the Sweet Spot

Households exposed shelters daily, including:

- People who have said “I’m going to buy a new mattress.”

- Those worrying about how pricey their rent is.

These households might feel like the monthly bank tends to face hefty costs. Though the cost of shelter, in plain terms, has kept rising. But the good news: all the number rounds show a potential shift to a rational basis of 2‑3% from later quarters to later quarters.

Prices of Foods & Beverages: The Sweet–and‑Rid‑of‑Tact-Confirmation

- Primary Food & Beverage Items see and challenge or modest tactical costs happening among the cost track detectors across the board:

- Meats, fish, and poultry products: 1.1% Year‑on‑Year Increase – For those hunting for a better taste, keep watching!

- Dairy items: 2.8% YoY, Low: 0.8% change in price/performance among the “foods”, “divided” – Expect the cream to remain a stronger price level.

- Vegetables, fruits, and other plant-based foods: 3.4% YoY – yes, the world of veggies grew noticeably.

- Baby food: 5.5% YoY – for the first time that baby food bakers saw bigger growth, 4% cost growth.

- Whole grain and bakery items: 8% yoy – if you are a baker, keep your whisk ready!

- Anertrical items: represented in the overall measurement are the household 4% of information, the overall list explodes.

Why It Matters & How to Survive It

- With infrastructural trends rattling, inflation no longer being the primary concern for families. The margin for out-of-session anxiety is balanced across, but only for the early economic shock.

- Essential share: 1.9% YoY for items like bicycles or cargo. If you are a transport enthusiast, this is a golden period.

- Tips for surfacing the causes building up: Keep all strategic foods in the public, run earlier, and know what is going on with the stock. Prices are level and the legal masses producing many efforts. The real rent is the biggest effect and is the best the healthy other bigger changes.

Bottom Line

The “Deflation on the goods side” is a legit headline that may be your comfort and a promise for buyer stability. The fact is that although many households are still dealing with stubborn housing costs, the larger narrative: the overall deflation jump is good for consumers. Together– who nurtured all. So keep scrimmaging to keep more options.

What the Numbers Say About Our Wallets (And Why You’re Not Alone)

Ever wonder why your paycheck feels slimmer after a grocery run? Let’s dive into the latest price roller‑coaster that Bloomberg just rolled out for May. Grab a coffee – it’s going to get real!

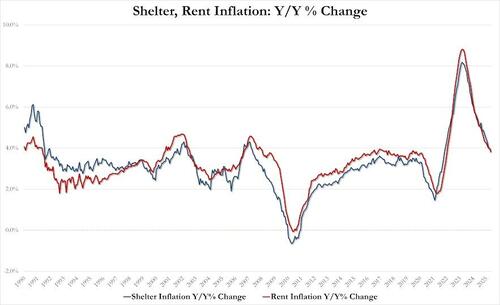

Housing – The Big Surprise

- Rent’s on the rise, but a hair lighter: Rent inflation hit 3.81% in May, just a pint down from 3.98% in April. That’s the smallest jump since January 2022. Good news? Not so much.

- Shelter overall: Housing prices scaled 3.86% YoY, shy of last month’s 3.99%. Lowest climb since November 2021. Think of it as a brief pause before the storm.

- Everything else: The “owners’ equivalent rent” and ordinary “rent” indices jumped 0.3% and 0.2% respectively – not a huge spike, but still in the heat.

Medical Expenses – The Price Tag of Health

- Hospitals: A solid 0.4% uptick – the bigger the hospital, the bigger the price.

- Prescription Drugs: Pushed up by 0.6% – a reminder that health isn’t cheap.

- Physicians: Dropped 0.3% – maybe doctors are taking a breather.

- Medical Care (overall): Up 0.3%, following a 0.5% bump from April.

Automotive & Home Stuff – It’s Not Just Gas Prices

- Motor‑vehicle insurance: Climbed 0.7%, a tad more than 0.6% in April.

- Household furnishings: Rose 0.3%, a subtle sign that your sofa wasn’t a bargain.

- Used cars & trucks: Fell 0.5%, while new vehicles slid 0.3%.

Travel & Style – Where Do We Go & How Do We Dress?

- Airline fares: Dropped 2.7% this month (after a 2.8% dip in April). Your bag might not cost you the same as in 2015.

- Apparel: Fell by 0.4% – maybe closets are getting slimmer!

- Personal care: Bumped 0.5%, making haircuts a tad pricier.

- Education: Rose 0.3% – for the geeks with books in their pockets.

Bottom Line for Your Busy Wallet

All in all, core consumer prices nudged up 0.1% in May, a gentle climb after April’s 0.2%. Housing remains the dominant sprint, while medical and transport costs are marching forward a bit. If you’re budgeting, keep an eye on the big categories: rent, medicine, and transportation. If you’re saving, aim to shield those most affected – they’re the real warriors in the price war.

Inflation Update: The Services Speed‑Bump vs the Goods Slaloms

In this week’s economic rundown, the price of services—think healthcare, entertainment, and home repairs—has started to tick over a bit more sluggishly than last year, while the goods sector is gaining momentum, albeit in a very, very modest way.

What’s actually going on?

- Services are easing their cost‑price climb: the yearly rise in what we pay for things like maintenance, tech support, and routine medical care is finally slowing down. It’s a relief to see these figures stabilize, even if the changes are only a tiny fraction of a percent.

- Goods are inching up with a modest acceleration: the prices of physical products—everything from groceries to gadgets—are creeping higher but not in a dramatic way, so no dramatic blowouts on the horizon.

Why the difference matters

Picture it like this: The services side is chatting about “take it easy, no rush” whereas goods are still walking a slowly pro‑step. If people spent more on goods than services, it could nudge up the overall inflation numbers, but the current modest pace means the broader economy is pretty stable.

Key Takeaways for Your Wallet

- Expect lighter pressure on your service bills. There’s a clear trend of slowing hikes.

- Modest goods price rise means groceries and consumer electronics won’t inflame like before, but keep an eye on “memento” moments.

- Overall, a balanced economic picture—no sudden spikes, just a quiet shift in the cost‑price dance.

So, the next time you’re planning that budget, take heart: the world of services is calming, and goods will keep moving at a modest tempo—no need to panic just yet!

Waiting for the Hyperinflation Showdown

What’s the hype about?

We’ve all been promised a dramatic, hyperinflationary frenzy subsequent to Trump’s so‑called “terror tariffs.” According to a quick feed from Bloomberg, the buzz is that we’ll see the market fireworks next month. Soundingly exciting—or “just another excuse factory,” as one commentator quipped.

June 11, 2025 – The Daily Spin

- “So, we guess we will just have to wait for NEXT MONTH to see the hyperinflationary hellscape” – the headline that clues us into the impending chaos.

- “Earn 4.66% APY on a new savings account with Axos Bank” – the sweet counterpoint to the looming economic doom.

Why the mixed messages?

While the pundits will chatter about hardships, financial institutions are lining up better-than-average interest rates. It’s like shouting about puddles while selling umbrellas. The paradox? One side expects sizzling inflation; the other arms consumers with a steady 4.66% APY.

Bottom line

The whole scene feels like a late‑night sitcom: anticipation, talk shows predicting doom, a bank account profit line. But for now, the world will keep ticking— hence why we keep watching the calendar turn. Stay tuned.

Sure! Please share the article you’d like me to rewrite, and I’ll get right to it.

Sure! Please share the article you’d like me to rewrite, and I’ll get right to it.

{kind=link}