Five Years In, and The Pandemic’s Echoes Still Ring

It’s easy to hear headlines shouting about a “tough‑as‑skin” U.S. economy: unemployment is low, GDP is back on the climb, and stock markets are partying. But the real story has a few darker shades to it. Beside those flashy numbers, a deep‑dive into the core stats shows that the U.S. is still grappling with the fallout from both the virus itself and the massive policy blitz that came in response.

The “Two‑Edge Sword” of Lock‑downs and Stimulus

Back in 2020, a chorus of economists sounded the alarm: the drastic measures would leave long‑haul scars. And yet the country over‑delivered. Lock‑downs rattled businesses; fiscal and monetary expansions ballooned into unprecedented sizes. They were marketed as the only way to balance health with hearts-on-fire economic output—an oversimplified wrong “public‑health‑vs‑economy” narrative that discarded the hidden cost of chilling the economy on such a colossal scale.

What’s Still Paying the Price

- Small‑business losses: Many family shops closed permanently, taking local jobs and community spirit with them.

- Labor‑market gaps: Although unemployment is down, certain segments (especially low‑wage roles and young workers) remain stuck in a “quiet‑period” of slow recovery.

- Inflation‑choked real wages: Rising prices mean the dollar’s buying power has shrunk for those who stayed in the workforce.

- Income inequality: The richest departments grew richer while the bottom tier saw the biggest setbacks.

Looking Ahead

These fallout issues aren’t simply a footnote of the pandemic; they’re a growing challenge that may take years—or even decades—to fully resolve. The next chapters of the U.S. economic story will require more than flashy headline metrics; they will need practical policies that repair the bruises inflicted on the nation’s industrial bones.

New Orders for Nondefense Capital Goods (Excluding Aircraft)

The Conference Board’s Niche Gauge lets us peek into how businesses feel about heavy equipment and durable assets—basically, if firms are ready to splurge on the stuff that keeps the economy humming.

The Pre‑Pandemic “Happy” Years (2015‑2020)

- Consistent growth, a solid sign that companies were confident.

- Capital formation was on the up‑trend, pointing to healthy investment plans.

- Long‑term outlook seemed optimistic; the data read like a sunny forecast.

The Great Plunge of 2020

- COVID‑19 rattled the globe and the orders tanked almost overnight.

- Supply chains slowed, factories halted, and business appetite cooled.

- Investor nerves were all over the place— the classic “slow‑down‑and‑pause” story.

2021: The First Steps Back

- Interest rates hit historic lows, providing a cheap boost for borrowing.

- Orders started to creep up, mirroring the overall recovery sentiment.

- However, the numbers never quite caught up to their pre‑pandemic levels.

March 2025: The Slow‑Paced Walk

- Orders slipped a modest -0.1% from the previous month—a subtle nudge that firms remain cautious.

- Despite incremental gains, the trend sits below the 2015‑2020 trajectory.

- It signals that the business world is still nibbling at risk rather than galloping widespread.

Why the Caution?

- Reshoring worries: Companies face decisions about bringing production back home.

- Labor shortages: Finding skilled hands isn’t as easy as it used to be.

- Geopolitical tension: From trade wars to uncertain alliances, the global backdrop isn’t inviting.

- All these factors keep the big‑spending wheel spinning at a slower pace.

In short, the data tells a story of a proud, growing economy that took a quick duck in 2020, wriggled back with some help from low rates, and now moves forward, albeit with a cautious slash of uncertainty. The future shows promise, but whether that promise turns into a full‑blown resurgence will depend on how businesses navigate the current landscape.

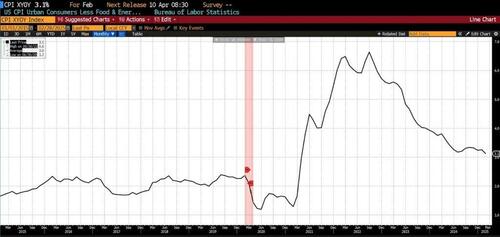

Inflation: The Silent Bouncer of Your Wallet

The Core CPI—the number that turns off the noisy food and energy price spikes—has been hanging out at about 2 % from 2015 up to early 2020. Then the pandemic threw a wild party.

What Went Wrong?

- Trillions in stimulus sent cash flying into the economy like confetti.

- Supply chains hiccupped, leaving shelves a bit empty and prices a bit higher.

- All this added a hefty bump to the Core CPI.

2022: The Peak, 2023‑24: The Cool‑Down

Core inflation shot up to its highest point in 2022. Like a boiling kettle, it’s had a chance to cool down since then.

What Does It Mean for You?

Even in early 2025, Core CPI sits around 3.1 % year‑over‑year—still above the 2 % sweet spot. That means your hard‑earned dollars buy less than before, especially if you’re on a middle‑to‑lower income.

Why the Fed Is in a Pinch

- Hiking interest rates to tame the inflation feels like tightening a noose.

- Lower rates would help growth, but with price pressure still high, the Fed’s got to choose wisely.

Bottom line: Inflation’s a relentless gremlin hiding in plain sight, draining purchasing power and standing in the way of smoother economic growth. Keeping an eye on Core CPI is like watching your wallet’s heartbeat—smaller jitters mean a healthier financial future.

A Peek Inside How Americans Feel About the Economy

Consumer confidence is like the vibe check for the nation’s finances—if you sense it, you know how folks are feeling about everyday spending and big life choices.

What the Conference Board’s Main Number Tells Us

- 2015‑early 2020: The mood was pretty upbeat—jobs were plentiful, wages were growing, and people were treating the economy like a rock‑and‑roll party.

- 2020 COVID crash: Suddenly, the party stalled: jobs disappeared, budgets tightened, and confidence took a nose‑dive—think of a sudden drop from a sky‑high balloon to a shaky jellyfish.

- 2021‑2024: A slow climb back up, but the economy’s showing a puddle, not a full-on skyscraper of confidence.

- 2025 outlook: Many households still wary, haunted by worries over rising prices, interest rates, and job security. The result? Cautious spending and a hesitation to grab new credit.

These feelings might keep the economic engine from roaring full‑speed, as people pull the plug on big-ticket purchases and new loans. In short, the economy is still sliding on a slide padded with caution‑tire pockets.

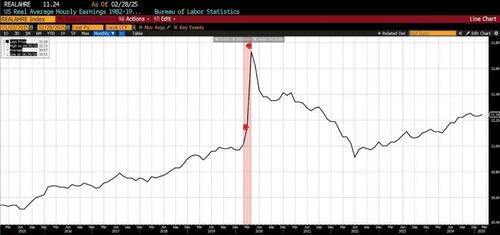

What the Numbers Are Really Saying About Your Paycheck

Back in the Day vs Today

When we strip out inflation and pull the money back to 1982‑84 dollars, the story gets a little dusty but still tells us what’s happening to your earnings. Think of it as a time‑travel snapshot of the average hourly wage.

2015‑2020: A Gentle Upswing

- Wages crept up slowly, kinda like your favorite slow‑mo coffee—just enough to offset productivity gains and a pretty tame rise in costs.

- Supersaturated with low‑inflation, everything seemed pretty stable. It was a quiet little climb.

2020: The Quick Spike (And then the Drop)

When the pandemic hit, the low‑wage workers lost more jobs than the high‑wage side, so the average wages popped up—just a bit. It looked like prospects were on an upward trajectory.

But Oops! Inflation came knocking and stole that nice bump right away. The numbers melted back to what they looked like before the crisis.

2025: The Slow Readjustment

Fast forward 2025, and the wages are only a tad better than before the COVID wave. That means your salary increases haven’t really outpaced how much groceries and rent cost. So, the pressure’s stacking up—home budgets get tighter, and the government may have to step in a little more.

The Bottom Line

In a nutshell, the real wages trend is essentially: sticking to the beam of growth. It feels like a roller coaster hit the brakes too soon, and everyone’s biting into that cost of living break‑even line.

5. Average Hourly Pay in the Private Nonfarm Sector

Think of the private nonfarm workforce as a steady march—until 2020, when wage gains flowed like a healthy river, buoyed by a competitive labor market and robust economic underpinnings. Then, the pandemic hit, and the wage flow hit a snag.

Post‑Pandemic Woes

- Wage growth has been neutralized by soaring costs—think coffee prices that keep doubling.

- Many workers find their real incomes hanging in a limbo state: flat or even slipping.

- Only a few sectors—like tech and logistics—are sailing ahead with better earnings.

For the rest of the workforce, it’s a holding pattern that feels as static as a frozen emoji.

Impact on the Everyday

When wages plateau, ripple effects spread wide: consumer spending shrinks, savings dip, investment stalls, and overall quality of life takes a hit.

In Short

Real earnings in the private nonfarm arena have stalled, echoing across the economy.

Saving the US One Dollar at a Time

Picture this: a ledger that keeps track of where every U.S. dollar goes—banks, businesses, households, and the ever‑busy government. Net saving is the sum of all those currents, and it tells us whether the nation is throwing money into a future stash or just cashing out.

What the Numbers Say (and Don’t)

- Before the pandemic, the flow‑of‑funds pages were showing a fairly steady balance. The economy was doing its thing—saving a bit, spending a bit, and keeping everyone in balance.

- 2020 hit the gas pedal. Government transfers (think stimulus checks) and folks cutting back on spending caused household saving to skyrocket—record highs! If you thought the savings account was super‑charged, you’re partly right, but it was a quick surge, like a surging tide that forgets to move on.

- Fast forward to 2025. Those ties to a high‑savings era have loosened. With living costs climbing and purchasing power shrinking, the neat thrift that people had is on the wane. The net saving has slipped back to its long‑term trend or even dipped below it.

- Why it matters. Low net savings means fewer funds for investments, less cushion when the economy hiccups, and families end up feeling the pinch. It’s like tossing all your future gifts back into the mail bin—you might end up while walking through a storm without an umbrella.

The Emotional Takeaway

Essence aside, having your dough tucked away for a rainy day feels like a hug from your future self. When saving rates dip, that hug turns into a dry, open‑handed gesture, leaving people vulnerable to shocks—be it a sudden job loss or a surprise bill. It’s a sobering reminder that in an economy that loves to spend, the art of saving is the craft that keeps families steadier for the long haul.

How the U.S. Workforce Is Feasting on the Great Unemployment Pie

The employment‑population ratio is essentially the health check for America’s labor market. Think of it as the percentage of people actually working out of the total number of folks who could work. It’s a snapshot, but a pretty telling one.

Rising Tide (2015–2020)

- From 2015 through early 2020, the ratio was cruising upward like a well‑balanced smoothie.

- Job gains swept across almost every demographic‑group

- Everyone, from teens to retirees, seemed to find a gig or two.

The Great Drop (Early 2020)

Then, boom! The pandemic hit hard. Suddenly, the ratio plummeted. Picture a giant crowd of workers in a Broadway show suddenly left the stage.

- Mass layoffs meaning fewer people in work.

- Shuttered offices & factories almost froze the whole show.

Why It Still Stays Low

Years later, the ratio hasn’t bounced back to former glory. Why?

- Early retirees have been lounging in their a‑la‑carte retirement menus.

- Long‑term health issues keep folks on the sidelines.

- Childcare troubles—like a never‑ending ice cream sundae—create a barrier.

- People’s job preferences are shifting; some prefer gig life over the 9‑to‑5 grind.

The Domino Effect

A lower ratio means fewer hands to keep the economy humming. The repercussions are wide‑ranging:

- More retirees—that’s a larger, older pool to support.

- Reduced tax inflow—fewer workers to contribute.

- Potential thinness of social programs that rely on active‑work contributions.

- Overall slower growth as fewer people pump money into the economy.

Bottom line: When the workforce shrinks, the whole economic machine takes a hit. It’s a chorus everyone’s listening to, and the audience is keenly watching how quickly the song can return.

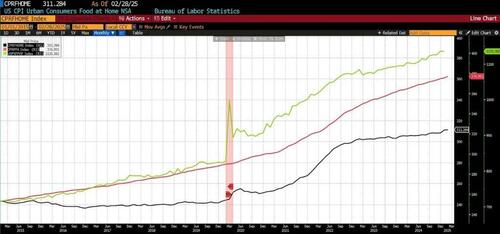

Food Price Gauntlet: From Chill to Chaotic

Food prices have been the quiet sidekick of economic trends for decades. In a world where inflation sneaks up like a polite neighbor, the market‑price of groceries owed a regular rhythm. Then the pandemic shuffled in, throwing a mix of fiscal fireworks, monetary bubbles, disrupted supply chains, and workforce hiccups into the blend. The result? A price spike that felt more like a comic book “hockey‑stick” than a tidy graph.

How the Price Curve Took a Wild Spin

- Late 2020 – Early 2022: The Sharp Ascent

- Staples (meat, dairy, grains) jumped faster than a skateboarder on a drift board.

- The rise didn’t just plot on paperwork; it sent real‑world wallets to the edge.

- 2025 – A Slight Slowdown

- While the steep climb slowed, prices lingered well above pre‑pandemic levels.

- The inflation rollercoaster is still looping, albeit at a gentler speed.

What This Means for Your Grocery List (and Wallet)

For households with fixed or modest incomes, the surge in food costs is a relentless squeeze:

- Budget Battles – Cereal that once cost a dollar now feels like a lump of cash hidden in your pocket.

- Food Insecurity Buzz – Communities across the U.S. are feeling the crunch, with more families scrambling for the next meal.

- Uneven Impact – Meat, dairy, and grains hit hardest, leaving families to adjust their menus in creative ways.

Bottom Line: A Kitchen‑intensive Reality Check

From the calm of steady prices to the frenzy of post‑pandemic inflation, food spending has jacked up faster than a kid on a sugar rush. The “hockey stick” turn of the numbers is a reminder that the market can change gears quickly, and budgeting for groceries now feels like a careful dance rather than a simple chore.

Inflation Expectations: The New Economic Roller‑Coaster

What’s the Big Deal?

Inflation expectations are like the economy’s weather forecast—if they’re sunny, wages rise, shoppers feel confident, and businesses invest. If they’re stormy, everyone is wary.

Pre‑Pandemic Default

- One‑, three‑, and five‑year outlooks were the “old reliable”—stable and smooth.

- Businesses and workers were comfortable knowing what to expect.

Since 2020, Things Turned Upside‑Down

- Expectations jumped suddenly and then started dancing wildly.

- What caused the chaos? Two big factors:

- First, an early inflation spike that shocked everyone.

- Second, policy responses that added more spice.

What Does This Mean for the Financial World?

- Higher and shakier inflation expectations raise the risk premium on investments.

- Long‑term contracts get called off—companies hesitate to lock in prices for the future.

- Households act like “inflation ninjas,” hedging against upcoming price swings.

- All of this erodes real wealth, since people keep saving and spending unpredictably.

Why Policymakers Are Feeling the Pressure

Credibility in inflation targeting has become the new headline for policymakers. They need to prove that steady rates are possible again, or else the economic “weather” won’t calm down.

The Housing Affordability Hysteria: Why Newbies are Longing for a House

Imagine buying a home feels almost like chasing a rare Pokémon—you trickling through the game’s levels, and suddenly it’s gone. That’s the reality for many first‑time buyers today. Cheap interest rates turned the house‑market into a roller‑coaster, the crowds trooped out of cities into suburbs and back twists, and the results? Sky‑high prices that’re out of reach for most hopeful buyers.

What’s Fueling the Price Surge?

- Interest rates at an all‑time low—big deal. Everybody is borrowing, and the cost of a mortgage has dropped like a hot potato.

- The great “flight to the suburbs”—people are ditching crowded downtowns in favour of roomy, green bags, and their hunger pushes local values to new highs.

- Inflation, coupled with huge Federal stimulus—home prices are sprinting ahead, while wages have stuck in a comfort zone.

First‑Timers on the Roller Coaster

- Most newcomers are still short on savings after the pandemic fiasco.

- The stimulus that was supposed to pad wallets has turned into extra “house‑money,” buffeting demand even more viciously.

- Supply chain headaches and slow construction delays mean there isn’t enough housing to go around.

- All of this cracks the affordability bridge, dropping it to record lows since 1986.

What’s the Bottom Line?

Homeownership has become a fanciful dream for many, a living sitcom where the giggles mask the struggle of falling behind. Because while a few are snug in their mansions, a ton of potential homeowners stare at listings, planning their future, and hoping a perfect sale turns into reality.

How the US Economy Is Still Hanging on the COVID Scales

When you look at the big picture after the pandemic, the numbers that most people love to flaunt look all sunshine‑and‑rainbows, but the reality is a little less pretty. The U.S. economy has been forever tweaked by the roller‑coaster of 2020.

What Went Down

- Massive Policy Pushes – Those emergency measures that saved lives were also a heavy hit on trade and production.

- The “Either‑Or” Story – Governments framed the situation as health vs. finances, ignoring a middle ground that could have helped both.

- Long‑Term Weight – Five years later, the effects still feel like a punch in the gut: wages dropping, capital spending tightening, inflation refusing to quit, and people not fully back in the labor pool.

Why That Matters for Everyone

Those trade‑offs aren’t just a headline—they’re a weight that keeps growing. The costs are high and will pop up in places we’ll see now, and in ways that are less obvious for a long time to come.

What to Keep In Mind

- Expect the ripple effect. The more money people spent on essentials (and less on other goods), the slower the rebound got.

- Think about the “hidden” costs. It’s not just the obvious things like fewer jobs.

- Look ahead! The price tag of those hard choices is still ticking up.

In short: the U.S. economy isn’t just “back to normal.” All the twists and bends from 2020 will echo for years, and it’s time to prepare for that ongoing journey.