Inflation Expectations: A Political Game of Numbers

At first glance, the University of Michigan consumer sentiment survey looked like a “who‑blames‑whom” episode of Survivor, with results seeming to swing wildly in favor of one political camp. Turns out, the debate isn’t just about coffee shop vibes or rhetoric—it’s about the seriously inflated (pun intended) numbers that have made the public think inflation is out of this world.

Why the Michigan Survey Has Been a Hot Topic

- Outliers everywhere: The so‑called “Dr. Hawk-eyed” economists have pointed out that demographic smoke‑signals, especially among Democrats, can push the expectations upward.

- The “Marxist” label: The idea that certain professors (with salaries that sometimes rival executive paychecks) are pushing a political agenda just feels like a political smoothie—half nuts, half smooth.

- “Just another survey” twist: While the survey itself is a valuable barometer, the narrative around it has become as intense as a reality‑tv drama.

NY Fed Consumer Expectations Survey: The Verdict

Just moments before, a New York Federal Reserve survey dropped its own numbers on the table. Here’s the skinny:

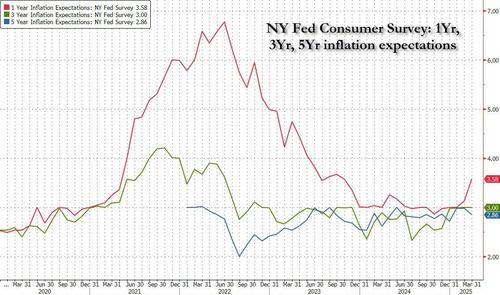

- 5‑year inflation expectation fell to 2.9%—down from 3.0%.

- That’s the lowest level since January. Seriously, the first week of the year? In your 50‑plus life, this thing blew a hole in the inflation “bubble.”

In other words, the Fed does not just “keep the froth” on the balloon of national expectation. They’re pulling the needle down, and the words keep moving—even though people keep clinging to that high‑cornered ballot.

The Bottom Line

If you’ve been listening to the news and noticing that the language about inflation now feels like a phonetic remix of political jargon, that’s exactly what the numbers and the surveys want to remind us.

- Inflation expectations are in motion.

- Check the NY Fed numbers for accurate info—don’t let any political hype distort what you’re really seeing.

- All in all, keep your eye on the inflation clock because it’s ticking down.

Feel the Numbers, Not the Politics

Sure, we’re all quick to grab the hype train, but a little data-checking keeps your money strategy on point. So next time you see those soaring or falling expectations, step back. The next 5‑year jump? It might not be a rail track, but it’s still a thorough elevator ride everyone’s boarding!

Inflation Expectations Take a Spin‑Turn, Yields Let Loose

What the Numbers Tell Us

- Three‑Year Outlook: Stuck where it was – no change.

- One‑Year Outlook: Gained a little, jumping from 3.1% to 3.6%.

- These figures are the kind of twist that keeps investors on their toes.

Why the Yield Dropped

When the inflation data hit the market, the two‑year Treasury yields tilted sharply downwards. The reason? The New York Fed’s survey, a blunt buzz‑word counterpoint to the University of Michigan’s numbers, said the one‑year inflation expectations are at 3.6% in March. That’s a record high for the month of March, but still far below the Democratic‑leaning 6.7% that the preliminary April UMich print warned for.

Mix‑And‑Match of Survey Signals

It’s like having two taste buds that disagree: one says “keep your expenses low” and the other screams “spend big!” The NY Fed’s voice is the louder one in the short term, nudging yields to sky‑rocket to new lows. Meanwhile, the big‑name UMich survey – though it swings the dial to a higher number – has a delayed impact on the market.

Bottom Line

With inflation expectations climbing a modest amount and the foretold divergence between surveys, the twists in the tick tape are like a mini roller‑coaster for the bond world. Keep an eye on those rates – they are never telling you exactly who’s calling the shots.

Inflation Expectations: The New York Fed vs. UMich—A Reality Check

When the New York Fed reports a five‑year inflation expectation dropping to 2.9%, it sends a subtle but clear message: our long‑term view of price growth is turning out to be more realistic than the hyper‑inflation hype that sometimes circulates out on Main Street.

Why the Drop Matters

- Fewer people are worried about runaway prices in the next five years.

- Policy makers get a clearer signal that inflation is staying pegged.

- It makes the UMich survey look a touch out of touch—like a news anchor who didn’t listen to the weather report.

What This Means for the Average Joe

Instead of a scramble over every coffee price, we can breathe a little easier. Your grocery list won’t suddenly inflate into the stratosphere. The longer‑term expectation staying low means:

- Stable purchasing power for retirees.

- Clearer planning for mortgage or student‑loan payments.

- Faster trust in the economy’s steady‑growth narrative.

The UMich Survey: A Quick Reality Check

While UMich’s numbers have music‑love‑like enthusiasm, they seem disconnected from the broader trend. It’s almost like a playlist that jumps straight from 1980s synths to an uprising of covers. Right now, ER sphere-wise, it’s time to tune in to the New York Fed’s clearer voice.

Bottom line: Higher expectations don’t always mean higher bills. The lower five‑year forecast is a positive sign that inflation is staying anchored and the economy is not about to go full “cardboard” crisis.

Inflation Panel Updates: What the Numbers Are Saying

Short‑Term Uncertainty Shrinks

- 1‑Year Forecasts – Confidence in next‑year inflation dropped, making future outlook a touch less mysterious.

- 5‑Year Forecasts – The same calming effect appears over the long haul.

- 3‑Year Forecasts – Still as steady as ever; no change here.

Housing Prices: Hovering in a Narrow Range

- Home‑price expectations slid 0.3% to 3.0% in March.

- Since August 2023, the series has been a stick‑in‑the‑mud between 3.0% and 3.3%.

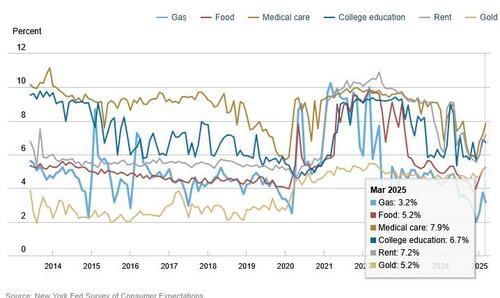

Year‑Ahead Price Expectations: Food & Drugs Jump, Gas & College Drop

- Food prices see a bump of 0.1%, reaching its highest spike since May 2024 at 5.2%.

- Medical care costs climb 0.7% to 7.9%, while rent edges up 0.5% to 7.2%.

- Gas prices slide 0.5% down to 3.2%, and the cost of college falls 0.2% to 6.7%.

In short, the world of inflation is a bit calmer on the near side, but still has room for surprise moves in the food, healthcare, and housing markets.

The Economic Outlook: A Reality Check

Recent figures from the NY Fed show that worries about stagflation are fading, but the warning signs for an upcoming slowdown (and possibly a recession) are more crystal‑clear than ever.

What’s Happening in the Labor Market?

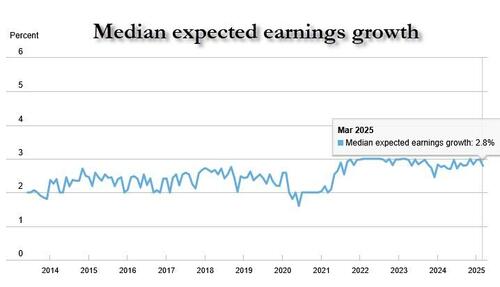

For the first time in months, the average expectation that wages will grow over the next year slipped a smidge: from 3.0% down to 2.8% in March. That’s right on the 12‑month average, and frankly, it’s a bit of a bone‑rattler when you’re watching inflation stay stubbornly high.

Unemployment, Job Losses, & Earnings Expectations

- Unemployment is creeping up.

- More people are losing jobs.

- People expect current wages to stagnate.

- Household income growth hopes are on the decline.

- Signor, signor — fear is mounting about next year’s finances and credit options.

Stock Market Sizzle

Even financial markets had to take a step back. Stock price forecasts fell, hitting the lowest level since June 2022. That’s a big drop, and it’s not just the numbers—we’re seeing the broader mood shift toward pessimism.

Calling the Numbers on Political Skepticism

Imagine explaining to the Democrats that while we’re battling high inflation, wages are actually shrinking. It’s a tough pill to swallow.

Bottom line: The economy feels a bit like a colde—prices are hot, but money flow is cold. Keep an eye on the trend, because it might steer the next wave of policy moves.

The Fed’s Alarm Bells: Recession Takes Center Stage

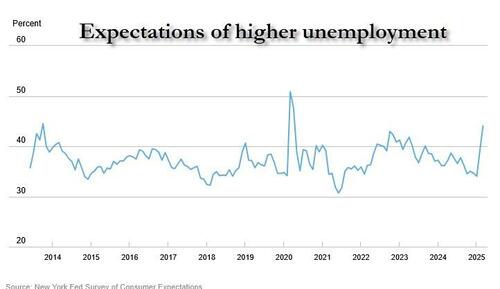

Forget about stagflation — it’s a thing of the past. What’s throwing the Federal Reserve into a frenzy is the looming threat of a recession. Recent data shows that the average unemployment expectations have surged by a jaw‑dropping 4.6 percentage points month‑over‑month, landing at 44.0%. That’s the highest reading since April 2020, and it’s giving economists a bad feeling about what’s next.

Why the Numbers Matter

- Long‑Term Jobless Risks Rising – Expecting more than 40% of the workforce to be out of work in a year signals a tough road ahead.

- Market Sentiment Shifts – Investors notice these bumps, and the markets start taking preemptive steps.

- Policy Hot‑Seat – The Fed feels the pressure to tweak rates, balance growth, and keep inflation in check.

Bottom Line

While the economy may still be juggling prices, the real concern is that jobs could be on a steep decline curve. If the rest of the market follows the Fed’s cues, we might see a recession on the horizon sooner than we’d like. Stay tuned — this story is far from over.

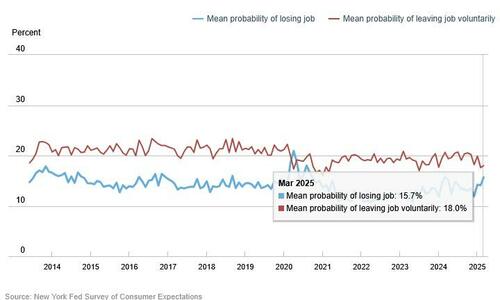

Job‑Fearing Numbers: The Latest Reality Check

Take a breath, because the stats just get a bit more dramatic. In the past month, 15.7 % of respondents feel there’s a real risk of losing their job within the next year. That’s the highest point since March 2024.

Who’s Ticking the Clock?

- Low‑income families (household earnings under $50,000) are watching the clock tremble the most.

- Those who might voluntarily quit see their chances rise slightly to 18.0 %—still shy of the usual 19.7 % average.

So What Does This Mean?

While the numbers are a bit uneasy, remember that most folks are still staying put. It’s a gentle reminder that the job market is holding its breath—especially for those earning less—so stay sharp and keep that résumé in mint condition.

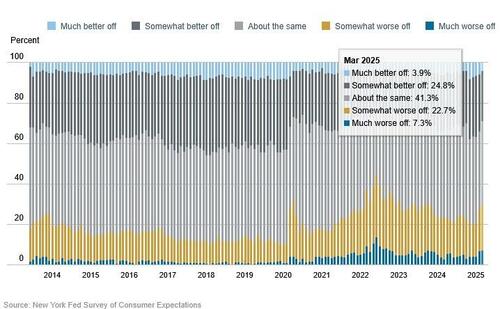

Household Finances in a Tight Spot

While the job market has been ebbing, the picture over the average household’s pocketbook isn’t looking much brighter. In March, folks began to feel less confident about where their wallets sit today compared to last year.

Key Takeaways

- Current Sentiment Slips: More families now say they’re worse off than a year ago than previously.

- Future Outlook in Decline: The doomsday forecast for next year’s finances jumped to 30 % – the highest since October 2023.

- Why It Matters: A sluggish economy and rising costs mean fewer hands to spend, less hope for savings, and a higher risk of hitting that dreaded “I can’t even afford groceries” threshold.

The Crunch Behind the Numbers

When families compare the present to a year back, they’re looking at changes in salary, living costs, and the mental chessboard of “will I make it next month?” The uptick in negative expectations suggests that more people are worried about future bills, stuck in a cycle of stress and uncertainty.

What to Do About It

- Revisit your budget like it’s a fresh piece of parchment.

- Cut that non‑essentials—yes, even those fancy coffee subscriptions.

- Seek out local community support or financial counseling; you’re not alone in this.

In short, the outlook is getting dimmer, but a little planning and a bit of community help can still help households stay afloat. Let’s keep an eye on those numbers and act before the tide is too high.

Household Income and Spending Outlook Drops Slightly in March

According to the latest data, median expected household income growth slid a bit in March, falling to 2.8 % – a touch below the 12‑month average of 3.0%. The dip is most noticeable among folks with only a high‑school diploma or those earning under $50,000 a year.

Key Highlights

- Income Growth Expectations: Down 0.3 pp to 2.8 %.

- Spending Growth Expectations: Slight dip of 0.1 pp to 4.9 %.

- Credit Access: More households say it’s getting tougher to snag credit now (and in the next year).

- Debt Payment Risk: Probability of missing a minimum debt payment in the next quarter dropped a thin 1.0 pp to 13.6%.

- Tax Outlook: Expectations for a future tax hike fell by 0.2 pp to 3.2%.

- Savings Interest Rates: Chance that saving‑account rates will climb in a year rose by 0.7 pp to 26.1%.

- Stock Market Expectations: Confidence that U.S. stock prices will rise in the next 12 months fell sharply by 3.2 pp, now at 33.8%—the lowest since June 2022.

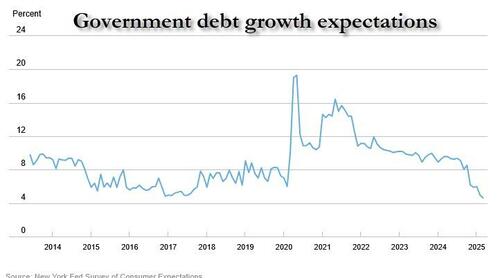

- Government Debt: Predictable debt growth is expected to slow, dropping 0.4 pp to 4.6%—the gentlest reading since the series began in June 2013.

What This Means for the Average Household

Imagine you’re juggling a bustling household budget. The numbers hint that while income might not surge dramatically, spending expectations are staying fairly resilient. Still, the widening credit squeeze means pulling a loan out of the closet is becoming a harder feat.

For those worried about monthly debts, there’s a slim sense that missing a payment becomes less likely than before—a small lift, sure, but a welcome one nonetheless.

Rumor Mill Verdict

All in all, it’s a mixed bag. Income and spending are conceding a little ground, but the risk of delving deeper into debt is easing just a touch. The real nail‑in‑the‑wall is the worrying dip in stock market optimism and that the expectations for U.S. savings rates are looking a little brighter.

What’s Inside the NY Fed Survey?

Everything you need to know about the economy is right here – the full New York Federal Reserve survey is just a click away.

- Economic sentiment – how consumers feel today.

- Unemployment trends – a look at the job market.

- Inflation outlook – what the data says about price hikes.

Why You Should Peek

Feeling curious? That’s the perfect time to dig deeper and understand the forces shaping our everyday lives.

Hang tight – recommendations are loading!

Please share the article you’d like me to rewrite, and I’ll get started right away!

Please share the article you’d like me to rewrite, and I’ll get started right away!