Gold Goes on a Winning Streak as China Opens the Market

In the run‑up to tonight’s much‑anticipated economic reveal from Beijing, the financial spotlight was on bricks of shiny gold. The gold market hit a sweet spot for the third consecutive day during the China open, sending investors across the board a little dose of pure optimism.

Why the Gold Is in the Driver’s Seat

- Stable Demand: Global traders see gold as a safe haven when uncertainty is high.

- Low Interest Rates: With yields on traditional bonds staying low, gold becomes a more attractive option.

- Currency Movements: Fluctuations in the yuan give gold a chance to sparkle brighter.

The Market Pulse

Gold prices keep your fingers trembling and your wallets itching for that next hint of brilliance. Investors have been dancing to a simple rhythm: buy more, hold tighter, and hope for more. And right now, that rhythm is hitting the high notes.

What’s Next?

Beijing’s upcoming policy statements may shift the gold wave, but for today, the market is treating investors like guests at a sizzling bash. Whether you care about the economy or just want to see your coins sparkle, tonight’s opening session sets the stage for both excitement and a touch of golden intrigue.

Yuan’s New Low: PBOC’s Latest Fix Leaves Investors Talking

Yesterday’s currency fix had the market buzzing. The People’s Bank of China (PBOC) nudged the Chinese yuan’s reference rate to 7.2133 per dollar, dipping down even further than the 7.2096 mark it carried over the weekend. It’s the weakest rate since September 2023 – a slow march toward the record low we’ve been eyeing.

Why the Fix Matters

- Currency Sentiment: Every time the yuan slides, it feels like a tiny boat wobbling on the waves of global trade.

- Market Confidence: A lower rate can shake up investor confidence, especially those eyeing China’s economic roadmap.

- Export Competitiveness: A cheaper yuan makes Chinese goods cheaper abroad, potentially boosting export sales.

The GDP Preview: What’s In the Numbering

We’re about to roll out China’s GDP data for the birth month of this year. Meanwhile, the statistics bureau’s March releases gave us a sneak peek.

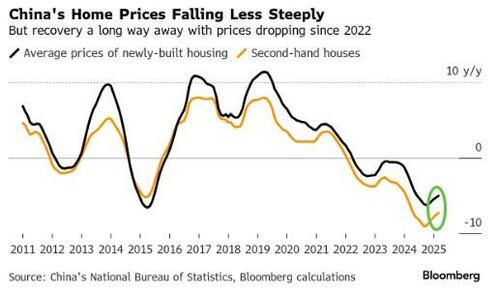

Home Prices: The You-know-Who’s Numbers

In March, prices for new homes dipped just 0.08% month‑on‑month. Meanwhile, existing homes slid a bit harder, down 0.23%. Looks like the price drop is slowing – maybe the market is getting a breather or just making sure buyers don’t miss out.

Investors’ Takeaway

- New homes are still holding their ground a fraction more than last month – a small sigh of relief for builders.

- Existing homes? The chuckle‑mile reduction signals steady demand, albeit softened.

- Combined, the numbers hint that the real estate market’s nightmare of falling prices may be on a one‑way ticket to a more balanced ride.

Bottom line: The yuan’s tug-of-war continues, but the real estate houses seem to be taking it in stride. Stay tuned, because next week’s GDP will reveal if China’s economy is sprinting, strolling, or taking its sweet time.

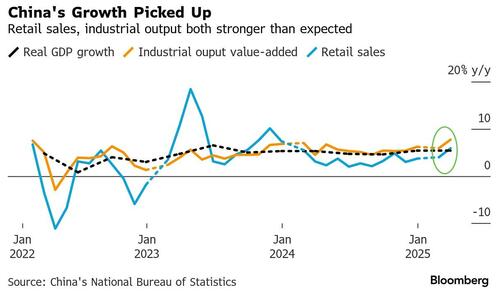

China’s GDP Growth Cuts Through the Tariff‑Tide

When you’re watching the heatwave of tariffs lick the borders, you’d expect the economy to slow down a bit – especially with March’s uneven numbers. But China surprised everyone by jacking up its GDP by a solid 5.4%, beating the 5.2% forecast and proving that growth still has a few tricks up its sleeve.

Why the numbers matter

- 5.4% GDP growth – the headline that keeps economists and investors on their toes.

- Against a backdrop of 10% tariffs on raw China imports (thanks, Trump), the surge shows resilience.

- Accurate forecasting would have predicted a slowdown, but the market says otherwise.

Three Things You’ll Notice

- The data came in pre‑Liberation Day, a key period that can tip the trend upside or downside.

- Manufacturing kept its hype alive, feeding consumer demand and export orders.

- Fiscal stimulus and tech investments are still paying off, clawing back any distortions from trade wars.

What this means for the global scene

- Supply chains get a little more reassuring – China’s output is steady, not flailing.

- Investors will keep a close eye on how tariffs might wrap themselves around next quarter’s data.

- It suggests that the “global slowdown” narrative isn’t as silver‑lining as some thought.

Bottom line

In a world where trade wars are the new normal, China’s 5.4% GDP growth whispers a simple message: Even with tariffs hawking overhead, the economy can still push forward. So, grab that coffee and keep your eyes on the reports – the numbers keep rolling in, and who knows where the next wave will take us?

China’s Fiscal Feats: Growth Hits the Mark and Surplus Breaks the Bank

In a season of bumper headlines, China’s economic performance was not just “in line” with its Q4 growth punchline— it also smashed Beijing’s 2025 full‑year ambition. And that’s saying something big!

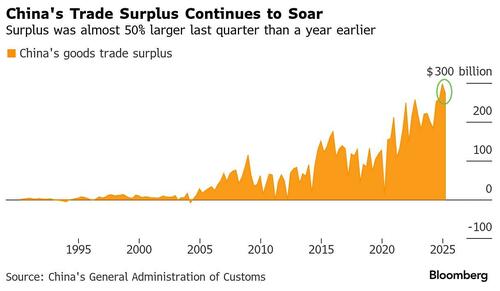

First‑Quarter Trade Swings: The Surplus Showdown

- Over $270 billion in trade surplus recorded in Q1.

- Just shy of last year’s record‑grabber from the final three months.

- Nearly 50% jump compared to the same period a year ago.

It’s like hearing that your favorite band ranked number one on the charts, except this time the numbers are less about an album and more about commodities, services, and a roaring market skyrocket.

The Record‑Breaking Surplus of 2023

Last year’s almost $1 trillion surplus wasn’t just a figure—it was a force multiplier that drove about one‑third of China’s overall growth. Think of it as the “big push” that propelled the economy forward. And the echo from that boost is still reverberating in Q4.

Why It Matters… and Why Everybody’s Happening a Bit Excited

- Smaller businesses got a chance to dip into a larger consumer market.

- Investment in high‑tech and green infrastructure got a boost.

- Every field, from niche startup gear to global supply chains, felt the ripple.

In short, China’s trade surplus isn’t just a statistic—it’s the economic equivalent of a massive confetti cannon, marking the continued ascent of the world’s second‑largest economy.

China’s Economic Pulse: A Quick Glance

China’s finance chiefs have set a 5 % growth target for the year—think of it as the big boss saying, “Let’s keep the economy humming.” To make that happen, they’re rolling out new stimulus measures and aiming for a record‑breaking budget deficit. Sounds bold, right?

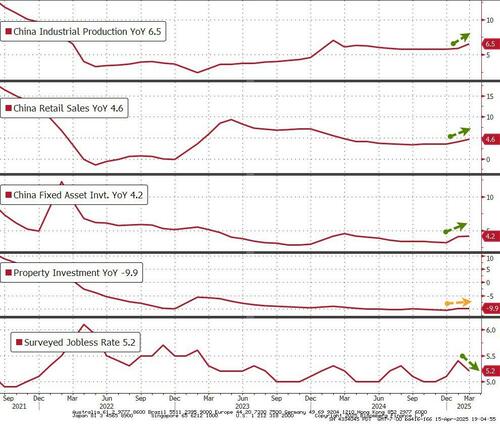

Data Highlights (and Some Surprises)

- Retail Sales jumped +4.6 % year‑to‑date – beating the +4.3 % expectation and the prior +4.0 %. A win for consumer confidence.

- Industrial Production went +6.5 % – outpacing the forecasted +5.9 % and matching the prior +5.9 %. Production lines are humming!

- Fixed Asset Investment earned a solid +4.2 %, just 0.1 % higher than the anticipated +4.1 %.

- Property Investment stayed flat at -9.9 %, exactly where analysts predicted it would land.

- Unemployment fell slightly to 5.2 % – a small but meaningful dip from the expected 5.3 % and the prior 5.4 %.

Why the Beat?

It turns out that tariff “front‑running”—think of it as catching the wave before it hits—has kept those numbers looking sharp. As Michelle Lam, Greater China economist at Societe Generale, puts it:

“The most pleasant surprise is retail sales, which shows that consumption subsidies are working,” she says. “Industrial production was a beat but understandable after the strong export data. But that’s all in the past now.”

Bottom Line

All in all, China’s metrics are telling a story of resilience and a few unexpected wins. With 5 % growth aims and big‑time stimulus, it seems the country’s economic engine is fine‑tuned and ready for the next quarter—just as people say: “Keep the gears turning!”

China’s Energy Boom Meets a Trade‑Aged Thriller

Why Beijing’s Belt‑and‑Braces Approach Is Import‑Skeptic

China is the world’s largest grabber of oil, natural gas and coal. To keep the country from becoming a one‑stop shop for burning fuel, Beijing’s been nudging energy companies to crank up production, hoping to keep the country’s hundreds of millions of extra feet of in‑feed burning under its own roof.

One‑Month Spark – Output Gains

- Coal: +9.6%

- Natural gas: +5.0%

- Crude oil: +3.5%

Coal and oil were way better than analysts had pinned, giving the ministry a brief “cheerful grin” before they meet the real drama.

U.S. Tariffs Turn the Inevitable into a Bargain Discount

According to Bloomberg, the U.S. duties on Chinese shipments are high enough to scrub them out of the U.S. market. Markets like UBS have dwarfed China’s GDP projection to a meager 3.4%, and Goldman Sachs and Citigroup have all loosened the optimism band.

“We’re in a trade war where the U.S. can crush most exports, even with temporary exemptions,” said Bloomberg economists Chang Shu and David Qu. “We expect Beijing to roll out stimulus faster than a Netflix binge roller‑coaster.”

The NBS Sombre Forecast

The National Bureau of Statistics issued a sober reminder:

- External environment getting rougher.

- Domestic demand failing to ignite.

- Need for more macro‑policy hacking.

They basically told us: “Heads up, we’re not done building the rocket.”

Beijing’s 30‑Point “Spend‑It” Blueprint

To keep the consumer economy rock‑steady, top Communist Party bodies rolled out a 30‑point blueprint. The goal: make people feel like new shopping carts are [somewhere] between the valley of the apple and the tech stack of the capital. It’s a consumer‑stimulus play that’s half aggressive, half “just give us a bigger budget for the snack bar.”

Bottom Line: Energy, Trade, and a Beekeeper’s Mission

Energy firms are firing up the engines, but the U.S. tariff wall is roughly a brick wall with a moniker of “Shocking”… If you’re in the Chinese consumer market, the government’s 30‑point plan might be the best thing since hanging the CCTV in every bakery. The economics are as real as a broken phone charging cable – keep them plugged in, or the whole system will die.

Ursula von der Leyen will take in an EU-China summit in July.

Ursula von der Leyen will take in an EU-China summit in July.