The Battle Over Bankers and Their Clients

It started as a simple tech‑savvy exercise—just another way for banks to keep their calculators in line. Now, it’s turned into a full‑blown political warzone. Governments are scrambling to decide just how far banks can wander down the road of choosing, or outright refusing, who gets in and out of their vaults.

Key Points in the Skirmish:

- Evidence Matters: Regulators demand proof that a bank’s decision isn’t based on a bad hair day or a sneaky loyalty loyalty scheme.

- Transparency Wins: The public wants to know the “why” behind every denial—no more mysterious black‑box decisions.

- Fairness Over Fortune: Let’s keep banks from treating customers like a game of Monopoly, where some get to move to luxury property and others land on the dreaded “Go To Jail” page.

What’s Going on Behind Closed Doors?

While the headline is a daunting copy‑editor’s nightmare, the reality is a mix of good old policy debates and the occasional flurry of emojis—yes, even #BankFail trending on Twitter!

Bottom Line

In this wild ride, regulators are trying to play diplomat, while banks are trying to avoid a honeymoon—and preserve their bottom line. If this trend continues, we might see the first Banker’s Handbook that explains who can get in and who can be politely sent to the side, all while sprinkling a dash of humor to keep things from getting too boring.

![]()

When Your Bank Pulls the Plug on Your Life

Imagine waking up, pulling up online banking, and finding your account locked tighter than a banker’s safe. No cash, no credit, no standing orders—just a quick banner that reads, “Account closed. Please find another way to manage your money.” The shocking twist? There’s no fraud alert or bounced check. It’s just a silent nod to some new “de-risking” policy.

What’s De-risking, Anyway?

In the financial world, it’s called “de-risking.” Banks spot a client or a whole industry and decide it’s safer to cut ties to avoid regulatory headaches or reputation damage. The result? People and businesses suddenly find themselves de-banked—cut off from essential banking services.

Why This Matters More Than You Think

- Money Matters: We all depend on daily transactions, credit, and savings. Remove those, and everything stalls.

- Crime Prevention and Politics: De-risking sits at the crossroads between fighting financial crime and respecting citizens’ rights.

- Trade and Travel: With banking services muffled, smoothed trade routes and simple journeys become trickier.

Different Regions, Different Rules

It isn’t a one-size-fits-all solution. The UK, the US, and the EU each have their own playbooks on how to handle such moves—pragmatic for authorities, but headache-inducing for everyday folks.

So, if your account just vanished, you’re not alone. And if you’re heading outside the usual channels, you’ll need a backup plan—because nobody likes a bank that suddenly plays hide‑and‑seek with your financial life.

The US: Concerns over ‘woke capitalism’?

Trump’s New Banking Clamp‑down: Banks Can’t Hide Their Bias

In a move that feels like the start of a thriller, former President Donald Trump just signed an executive order that tells banks, “No more hiding your morals in the paperwork.” Banks are now barred from using “reputational risk” – a fancy phrase that secretly means having too much political baggage – to close accounts, and regulators must check the playbook in fifty‑two weeks.

Why the Trump‑Tresses Gave This Order the Green Light

- Freedom of Speech: Trump and his squad claim that conservative voices have been treated like digital asylum seekers, labeling their accounts for “insulting the president.”

- Defense Against De‑Banking: Those who think banks have been harassing Trump have a clear solution – make it illegal to refuse a customer because of their politics.

- Political Pizzazz: It’s a perfect bench‑warm for spin‑masters and campaign teams who want to keep the money flow humming.

Opposing Voices and Who’s Holding Their Hand

Some are hollering, “We’ve got to stick to good money!” Saying that this will turn banks into “bank‑gloat” to unverified shelters. They fear the policy will keep banks clinging to users who could be doing some shady stuff behind the curtain, like running crypto laundering schemes or enabling plots that could scare DOE (Decent Oblivious Extremists).

Trump’s Own Debits of Shame

He’s no stranger to blood on his hands. The man famously claimed that after his first term, two banking titans – JPMorgan Chase and Bank of America – started hydrating him “in a ‘No,’ we’re not going to do this.’” He says JPMorgan gave him a mere twenty days to close his account, while Bank of America kept its thumbnail up on an enormous deposit, yet both allegedly let the “in‑no‑political” act through.

De‑Banking: The Broader Plot

The simmering tension over “de‑banking” hit a new footnote in late 2022 when a National Council for Religious Freedom (NCRF) kicked off. They explicitly back those politicians who like to mix religious zeal with big‑bad politics, and dare to oppose bills like the Equality Act, citing “religious freedom” as the final front‑line defense.

Stay tuned. This drama is about to go public, but whether the banking system will finally turn a blind eye to politics— or whether they’ll keep buckling under the weight of its own moral… only time will tell.

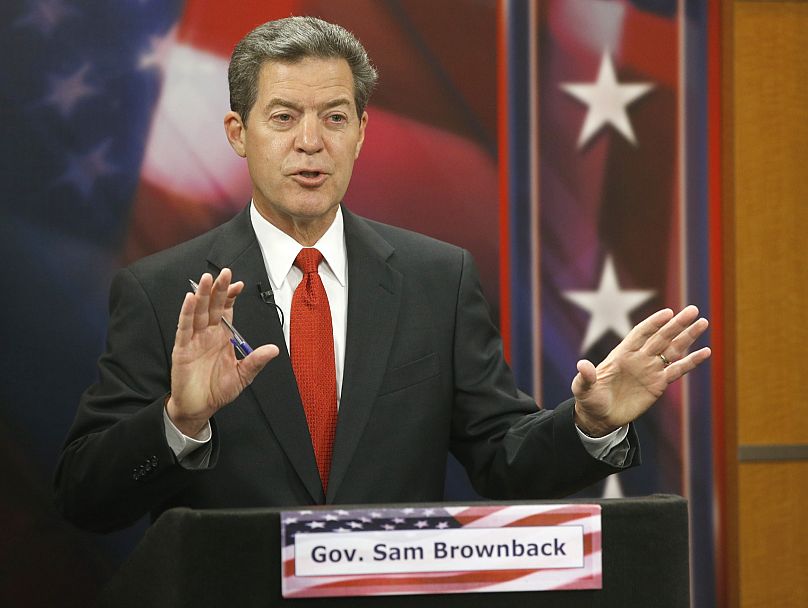

Sam Brownback Fights Back After His Bank Accounts Vanish

Former Kansas governor Sam Brownback, who kicked off the National Counter‑Response Fund (NCRF), is waving a flag that says he’s been de‑banked on purpose.

Why Banks Tempted to Box In Activists

- When a group suddenly stashes a fat stack of money into a bank, regulators go red‑alert.

- Big banks—especially JPMorgan Chase—have to keep their compliance wheels spun, or they risk government black‑listing.

- Activists can look “too political,” and banks hate being the center of a potential scandal.

The “Not a Political Move” Letter

The bank sent a letter that reads like a polite yet professional medical report:

“The closure arose from incomplete compliance documentation, not religious or political reasons.”

Sound familiar? No.

From “De‑Banked” to “Woke Capitalism”

Instead of shrugging off the bureaucracy, the NCRF turned a bank’s oversight into a campaign slogan:

- They’re shouting, “This is woke capitalism for the win!”

- The goal? Crowds out decision‑makers that put politics over pure risk metrics like credit or compliance.

- They’re even gearing up for a national lobbying push to fight defunding and reputational risks.

What This Means for the Banking World

Bankers now have a new headache: imagine sifting through thousands of closed accounts, recording every small oversight, and deciding whether to re‑open them. It’s a recipe for chaos.

Bottom line: Sam Brownback’s story shows that “politics” might not be the real reason your account gets flagged—often, it’s just a compliance glitch folks miss. And if you’re a bank, you’d better double‑check your docs, because it could cost you a lot more than just a few polite letters.

The UK: Farage, Coutts and public outrage

The Nigel Farage—Coutts Saga: A Closer Look at the Banking Backlash

Picture this: a flagship private bank, known for its hush‑hush charm, suddenly drops a high‑profile political figure from its roster. The media erupts, headlines scream, and the public demands answers. That’s the 2023 scene when Nigel Farage’s account was slammed shut by Coutts, only to later reveal that his politics had been the real reason behind the move.

Why the Bank’s Decision Might Just Be Smart Business

- PEP Status Matters: Farage is officially a Politically Exposed Person (PEP). Banks must conduct “enhanced due diligence”—think of it as a mega‑security check on every transaction, constant monitor‑and‑reassess routines, and an eye on any hint of corruption.

- Higher Costs, Lower Returns: A PEP demands a lot more resources—a full time detective team, extra compliance paperwork, and a rigorous risk review. If the client’s account didn’t meet profitable benchmarks, the balance tip looks like a no‑go zone.

- Reputation at Risk: This isn’t a cute “politics” issue. Every high‑profile vetting brings the chance of a PR nightmare. For a bank built on low‑risk, discreet clientele, the cost of staying on board could outweigh the benefits.

In short, from the bank’s side, letting Farage go may have been a textbook risk‑management decision—more of aligning a client with a strategy than a political cleanse.

How The Story Steered UK Banking Policy

Even though Coutts’ reasons might make sense to insiders, the public got a different story. Here’s why this one set a precedent:

- Financial Ombudsman Service (FOS) Buzz: In 2024, account‑closure complaints spiked 44%, hit almost 3,900 cases, and more were in favour of the customers. Over 140,000 business accounts were shut down the previous year — a shock to small firms and non‑profits.

- New Rules Rolled Out: Banks now must give at least 90 days’ notice before stopping an account and detail why they’re pulling the plug.

- The Headlines Still Stick to Politics: It’s odd, but that’s the twist that keeps the narrative focused on the personal drama, not the broader economic consequences of de‑risking.

So while the bank’s playbook may have been perfectly fine, the public and regulators got a storyline that’s part drama, part policy lesson, and all about how a single high‑profile case can reshape an entire industry.

Standing Tall in Frankfurt’s Financial Hub

Picture this: the European Central Bank, a stone‑cold monarch of monetary policy, and it’s chillingly calm next to a row of sleek banking giants in Frankfurt. 2019, September—when the sun had a chance to drape a golden glow over the city’s skyline.

The ECB Building: More Than Just a Brick Wall

- Architectural prowess: A minimalist façade that whispers “authority” to anyone passing by.

- Office vibes: Inside, negotiators and analysts scribe the future of euro‑sized economies.

- Paneramic views: From the balcony, you can almost hear the gentle hum of transactions worldwide.

Frankfurt – The City That’s All Business and a Dash of Culture

Once a sleepy riverside town, Frankfurt now juggles towers and traffic with equal flair. The Central Bank’s presence is akin to a cool guru standing guard beside a bustling hive of financiers.

Why September 2019 is a Milestone

That summer buzz was about more than just June heat – it marked the ECB’s 30th anniversary of influencing the euro. 2019’s autumn chill added a dramatic touch to the ceremony.

A Bit of Humor to Warm the Mood

Ever wondered why the ECB doesn’t play hide‑and‑seek? The reason: there are plenty of hurdles to cross and no time for games. Even so, the building’s silent demeanor hints at a gentle heart—forever watching over the financial universe.

The EU: Quiet, technical and high stakes

Brussels vs. Bankers: A Light‑hearted Look at De‑Risking

Picture Brussels as the eternally patient teacher, handing out lesson plans for how banks can keep the bad actors out while still giving the good folks a chance to keep their savings. The EU has been rolling out the same textbook for years—keep financial inclusion alive but still stop money‑laundering nu‑baboons and plots of terror from getting a free ride.

The Tightrope Walk

“European Banking Federation (EBF) member banks often find themselves stuck between a rock and a hard place: they must drop the wackiest customers to meet AML/CFT rules but still need to hit the VIPs of the regulary paying people,” Roger Kaiser, Head of Tax & Compliance at the EBF told Euronews. He added, “The bank’s decisions should be smart, risk‑based and not block entire countries or customer groups outright.”

How Banks Keep the Scale Tied

Most ever‑European banks tackle the problem on a case‑by‑case basis, hunting for the red‑flag situations like:

- When a customer’s ID can’t be verified with secure, government‑approved checks.

- Transactions where the real person or company behind the move is unclear, or the true “beneficial owner” can’t be pinpointed.

- Any tricky, uncertain client. Banks weigh the cost of extra scrutiny versus the worth of the file.

Balancing Act

For these banks, the toughest part is deciding whether the risk can be mitigated while not over‑spending on paperwork that could drain the account’s value. It’s a delicate split‑second call: “Will we drop this customer? Does the regulation say so? Or do we keep ‘em on the list with a simplified verification process?”

Is this a New Issue?

According to Kaiser, the EU is increasingly treating de‑risking as a consumer-problem but it doesn’t mean the “Trump era adjustments” are the exact same. “The European Banking Authority and others have long been around the corner, giving us guidelines that protect everyone’s sanity and wallet.”

In short, Brussels is still on the possibility of keeping banks safe but not turning anyone into a banking ghost.