Central‑Bank Bonanza: A Raucous Week Ahead

What’s on the Calendar?

- Wednesday: Fed & BoJ – both set to drop decisions that could shake markets.

- Thursday: BoE – the Bank of England kicks off the countdown with its own policy move.

Data Highlights Falling Down the Line

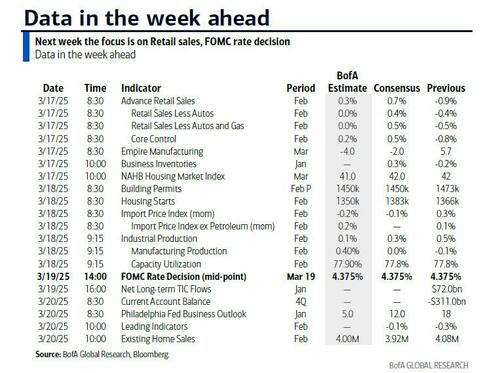

- US Retail Sales (today): The numbers were a mixed bag – no easy smile for economists.

- US Housing Figures: A slew of data points that could hint at a housing boom or bust.

- UK Labor Market (tomorrow): Jobs stats that will test the Bank of England’s patience.

- Japanese Inflation (Friday): A crucial read for the Bank of Japan’s next move.

- Canadian Inflation (tomorrow): Another north‑bound narrative moving the Bank of Canada.

Why It Matters

Grab your coffee, because this week is a carnival of policy releases and economic data. Watch the headlines, keep the markets in check, and try not to trip over your own excitement!

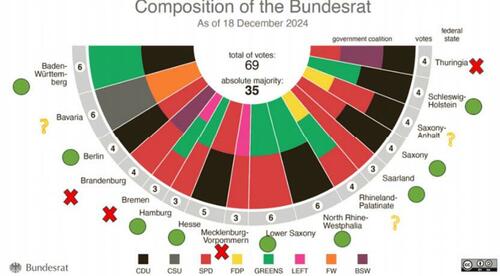

Germany’s Budget Blitz: A Quick Take

What Just Happened?

After the white smoke of a deal swept across Friday, all eyes have shifted to the mega fiscal expansion that’s expected to power up Germany’s economy.

Why It Matters

- Bundestag – Set to vote tomorrow.

- Bundesrat – Planned to weigh in on Friday.

- New Bundestag opens on March 25, ready for action.

Timelines & Tick‑Tocks

Think of it as a sprint: a vote tomorrow, a vote Friday, and then a fresh legislative house stepping in. Hit the right notes, and Germany could get a serious fiscal boost; miss, and it’s a cautious rewind.

And Oh… Trump’s Surprise Twist

Just as the political circus is tightening up, Donald Trump says he’ll be talking with Vladimir Putin tomorrow. Talk about an unexpected plot twist!

So, buckle up! It’s going to be a rollercoaster of debates, ballots, and a dash of diplomatic coffee chats.

What’s On the Menu This Week?

We’ve got a full banquet of economic headlines, central‑bank speeches, and a little political drama – all wrapped up in one powerhouse week. Let’s cut to the chase and flavor the story with some real‑world talk.

Fed’s Big Decision (Wednesday)

- Hold the line: Most analysts reckon the Fed will keep rates steady on the March 18–19 meeting. No “blink‑and‑you’ll‑miss‑it” cuts expected.

- QT pause, not a sprint: The Fed will likely announce a pause in the quantitative tightening starting in April. Think of it as a “take a breath” before pulling the lever again once the debt ceiling issue is sorted.

- Dot‑plot drama: They’re aiming for two cuts in 2025 but with an upward drift that could push the median dot to a single cut. 2026‑27 dots appear unchanged – a quiet 3.875% / 3.375% / 3.125% progression.

- Projection tease: Inflation pops up to 2.8%, GDP growth is trimmed to 1.8% (tariffs chewing up the numbers).

Germany’s $2‑Trillion Power Move (Thursday‑Friday)

- Berlin’s Fiscal FWD: The Bundestag votes tomorrow, the Bundesrat on Friday. If the deal gets the green light, we’re looking at a fiscal stimulus of 3–4% of GDP by 2027.

- Constitutional curveball: A court may rule there’s been no proper scrutiny, but the legislation is only a 20‑page chunk, so the legal risk stays low.

- Market reaction: DB’s Jim Reid says markets already priced in a game‑changer that will boost Germany’s longer‑term growth.

Central Banks Beyond the Fed

- BoJ: Will keep rates steady and the policy framework unchanged.

- BoE: Holds the Bank Rate at 4.5% – no surprises.

- ECB: Villeroy and colleagues will give speeches; watch for signals on future policy.

Geopolitics & Micro‑Worlds

- Trump‑Putin chat: Could whet the appetite for a ceasefire agreement next week.

- NVDA GTC: Jensen’s keynote on Tuesday will steal the spotlight.

- Earnings round‑up (Thursday): Nike, FedEx, Micron, Lennar, RWE, Accenture, PDD Holdings all drop their numbers. Keep an eye for surprises.

Daily Clock‑In

Here’s the rundown, but we’ve sliced it down for you. Read on if you’re hungry for the details.

Monday March 17

- US Retail Sales (Feb) – +0.7%

- Empire Manufacturing Index (Mar) – glance at the negative surprise.

- NAHB Housing Market Index (Mar) – stays flat at 42.

Tuesday March 18

- US Industrial Production (Feb) – 0.2% rise, thanks to auto and heating demand.

- Asset‑Pricing data – import/exclusion movements.

Wednesday March 19

- Fed announces no hurry for cuts; banking speeches.

- ECB, BOJ, BOE speak; markets flip over their projections.

Thursday March 20

- US Q4 Current Account – a sizeable negative balance.

- Philadelphia Fed Manufacturing Index – flat on expectations.

- Existing Home Sales – a modest jump.

- BoE and SNB decisions; Eurozone bulletin.

Friday March 21

- No major data releases – perfect day for speeches.

- New York Fed President John Williams delivers a keynote in the Bahamas.

Bottom Line

It may feel like a circus of policy and data, but the common theme? The Fed keeps the brakes on, Germany looks to jump on a fiscal storm, and other banks hold dear to the status quo. Keep your headset ready for speeches and watch those earnings for the juicy half‑pints of quarterly surprises.