Manufacturing PMI: The Rollercoaster of Numbers

Soft data once fantasized about endless growth, but reality’s hard data button hit the reset knob. All eyes are now glued to this morning’s PMI figures, hoping for a reality check that keeps the economy from strutting too far.

- S&P Global’s US Manufacturing PMI: Officially leaped from 50.2 to 52.0 in May—slightly shy of the flash print of 52.3, but still the highest since February. The bell’s ringing loud, but not too loud.

- ISM’s US Manufacturing PMI: Dropped from 48.7 to 48.5— below the expected 49.5—and marked the lowest since November. A gentle nudge that the economy is holding its feet on the ground.

Key Takeaways

- Manufacturing is showing signs of partial recovery with S&P Global’s numbers amused to their highest in months.

- However, ISM’s dip reminds us that the overall mood is still cautious.

- Both indices underline the importance of hard data over soft optimism.

US PMI Flips: Growth on the Surface, Turbulence Beneath

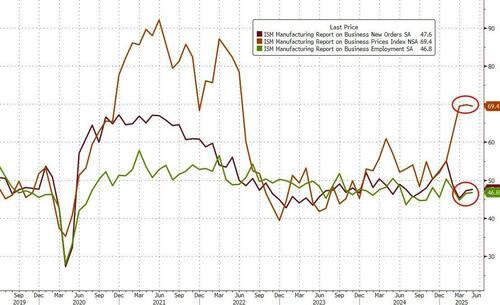

While the headline PMI zoomed up in May, the back‑story is far from rosy. According to Chris Williamson, the Chief Business Economist at S&P Global Market Intelligence, the uptick hides a brewing storm in the U.S. manufacturing sector.

What the Numbers Show

New orders climbed and suppliers were busier than a street corner mural artist on a Saturday rush.

- Highest supplier delays since October 2022

- Price hikes at a peak that hasn’t been seen since November 2022

- Drivers? Mostly tariffs pulling the strings.

Who Gets Hit the Hardest?

Small‑scale manufacturers and those selling to everyday consumers have felt the brunt.

- Tariffs squeeze supply chains, throwing a wrench in their operations.

- Demand spikes are temporary—rooted in fear of plant downtime and soaring costs.

Key Takeaways

Even as the PMI porch is occupied by new orders and job cuts slipping, the economy’s heart is suffering from giant price inflation and the longest supply interruptions in years.

Prices are chilling at or near three‑year highs, while new jobs and orders take a nosedive.

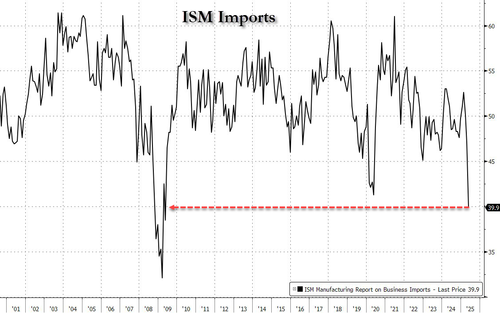

April’s Import Slide: A Record Low Since 2009

Picture this: the U.S. import ledger suddenly feels a bit lighter than usual. In April, the bulk of goods coming across our borders dipped to the lowest point in over a decade—since the financial crisis of 2009, to be precise.

What’s Going Down?

- Automotive: Fewer cars, fewer trucks. Think of it as the economy taking a hit on the “drive” factor.

- Manufactured Goods: From silicon chips to kitchen appliances, imports of manufactured items took a nosedive.

- Consumables: Even everyday items like coffee beans and canned goods saw less inflow.

Why Did It Drop?

Several factors played their part:

- Supply Chain Strains: The pandemic aftershock left many factories running on fumes.

- Currency Fluctuations: The dollar’s strength made foreign goods cheaper, but also reduced the volume of imported goods.

- Trade Policy Swings: Recent tariff changes created momentum ripples across the import tide.

The Bigger Picture

While a drop in imports can be seen as a heartening sign that domestic production is holding up (or at least that imports aren’t causing runaway inflation), it also raises a few red flags:

- Potential partners in China and Mexico might find their American output markets shrinking.

- Industries that rely heavily on imported components could feel the pinch—think semiconductor manufacturers.

- Consumers could end up with fewer options or pricier goods in the long run.

Bottom Line

April’s import slump is a headline worth paying attention to. It’s the kind of economic ripple that could reshape trade relationships, influence inflation dynamics, and, frankly, leave marketers staring at a suddenly shorter list of products to sell. Keep an eye on the data curve—it’s still a far from smooth ride.

Manufacturers’ Mood Swing

What happened? After the tariff storm in April knocked many plants for a beat, the crew bounced back a smidge in May. The pause on new levies gave them a breather, but the big picture is still a bit shaky.

Why the hesitation persists

- Tariff Flexibility: The rules keep shifting, like a merry‑way that’s always in flux. That makes it hard to put faith in any long‑term plan.

- Hiring Angst: Human resources? Not so sure. With the numbers dancing, most factories are knocking the “I’m hiring” button and then cringing.

- Business Pulse: Even the confident ones can’t ignore the lingering uncertainty—after all, who wants to market to a business that’s in a constant state of “what‑now?”

Takeaway

Even with a flicker of optimism, the tolerance for risking fresh hires is low when the tariff landscape resembles a pick‑up game that never stops changing the rules.