GDP’s Second Shake‑Up: Numbers Gone Wild (but not as Wild as Yesterday’s Milk)

Ever feel like economics is stitched together by yesterday’s milk and today’s stale data? That’s how this story starts. Skipping the buttery swirl of wait‑and‑see politics, the Bureau of Labor Statistics just pushed a second revision to Q4 GDP, pushing that figure up to 2.4%. Even though it’s slightly shy of the 2.5% dream we all thought, it still beats the median pick of 2.3% (ath a range +2.2% to +2.6% from 55 sharp‑eyed economists). Let’s cut to the chase and see why the numbers dipped, DNA‑checked, and how the inflation picture comes to the party.

Snapshot of the Revision

- GDP (Second Revision): +2.4% versus the second estimate of +2.3%

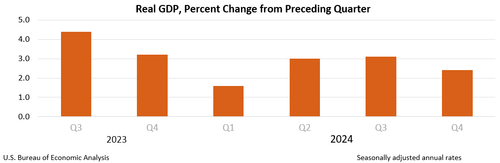

- Previous Final Print (Q3): +3.1% — the new 2.4% is noticeably lower.

- Consumer Stuff: Despite the usual consumption squeeze, it dipped from 4.2% to 4.0% — both shy of the expected 4.2%.

- Trade & Imports: The uptick is thanks mostly to a less‑than‑expected cut in imports, pulling the ballast back.

Inflation Storyline (What’s Not Melting Fast)

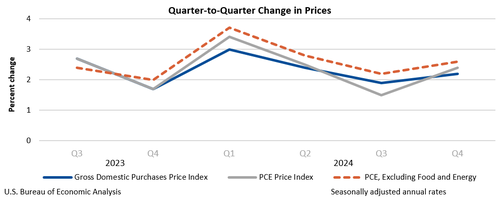

- GDP Price Index: +2.3% compared to the second estimate of +2.4%. Hot, but not scorching.

- Core PCE Q/Q: +2.6% versus the second estimate of +2.7%. So, the price tag is tidier than we predicted.

Why the Numbers Show a Downward Trend

It’s like a dance floor that’s almost burned out: consumption is stepping back, imports are sliding away, and trade’s not giving us that boost we hoped for. Yet, the GDP stillclimbs because a few imbalances – the slower pull on imports – make the heavier part of the economy feel a little lighter.

Quick Takeaway

We’re not seeing the economic fireworks that a 2.5% headline would promise. Instead, we have a more reserved performance, with inflation whispers and trade dropping the mic. The next big block is the personal income/core PCE numbers tomorrow, so keep your eyes (and your snacks) on the main stage.

Q4 Real GDP: A Roller‑Coaster of Spending & Imports

Ever wondered what the Bureau of Economic Analysis (BEA) had to say on the latest quarter? Grab a cup of coffee and let’s dive into the story behind the numbers.

What’s Fueling the Upswing?

- Consumer spending – People are treating themselves a little more, which keeps the economy humming.

- Government spending – Public projects and services are pumping cash into the mix.

These two forces pushed GDP up, but there’s a twist:

The Investment Oopsie

Meanwhile, investment dipped a bit. Think of it as the economy saying, “Hold on, I’m still figuring out what I’ll buy next.”

Imports: The Silent Saboteur

Imports, which subtract from GDP, were on a downward trend. The fewer things we’re buying from overseas, the less we’re subtracting from our growth figure.

Chart Highlights (Without the Visuals)

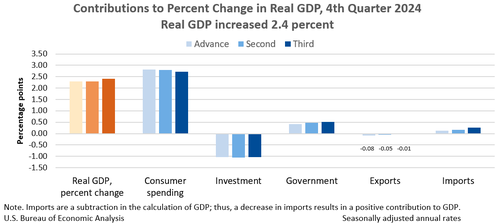

Figure double-check! The latest season’s estimate saw GDP jump 0.1 percentage point from the previous (second) estimate.

Why? It’s mainly a downward revision in imports that freed up some room for the overall GDP figure.

Bottom Line

So, in short: folks are spending more, the government’s injecting funds, investment has taken a breather, and imports have tightened up. Altogether, that’s why we’re seeing a modest uptick in Q4 real GDP. Cheers to a balanced economy—just a bit more balanced than before!

GDP Growth Dissected: A Fourth‑Quarter Breakdown

What Stole the Momentum?

Here’s the low‑down on how each Lego block of the economy chipped into the total. No fancy jargon, just the real numbers that markets chase.

- Personal Consumption: 2.70% – because everyone loves a good coffee buzz.

- Fixed Investment: –0.2% – a tiny hiccup in the “build‑your‑dream‑factory” budget.

- Private Inventories: –0.84% – shelves look a touch thinner than last quarter.

- Exports: –0.01% – barely a drag, but a stub in the planet‑wide trade parade.

- Imports: 0.27% – a mild surrender, not a disaster.

- Government Consumption: 0.52% – a modest nudge from the public‑sector side.

Grand Total: 2.44% – a respectable jump when you add up the whole village.

Why the Drive Was Slower This Quarter

The slowdown in real GDP mainly came from two bad guys: a slump in investment and a dip in exports. The hero of the story—consumer spending—kicked back a little boost, pulling the economy out of a potential wobble.

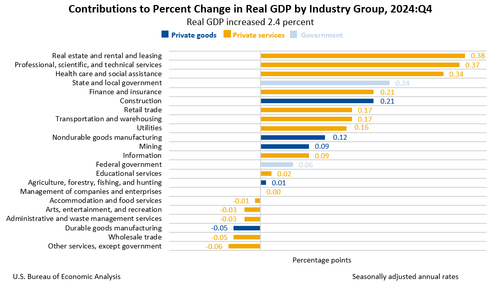

Industry Highlights

- Private goods‑producing sectors saw a 2.3% rise in real value added.

- Private services‑producing industries pulled a 2.4% increase.

- Government’s own contribution jumped 2.7%.

Bottom line? Even when the runners in the marathon feel a bit sluggish, keeping your footfalls steady—especially with those consumer swings—can keep the finish line within reach.

Yo, the Economy’s Still on the Rise!

In Q4, the U.S. real gross output didn’t just lag behind – it sprinted forward by 1.7%. That’s a pretty solid jump, and here’s the low‑down on where the gains came from:

- Private goods‑producing firms nudged up by a modest 0.3% – slow and steady.

- Private services‑producing businesses pumped up by a hearty 2.0%, giving a nice boost.

- Government‑run sectors surged the biggest, a cool 3.1% – talk about a public‑sector party!

Inflation? The Big Picture

The price index for gross domestic purchases slid up 2.2% this quarter, but that’s 0.1 percentage point lower than the earlier forecast. A small dip, but still on the inflation‑track.

Personal Consumption Expenditures (PCE) – No Skipping Nostalgia

The PCE index is up by 2.4%, matching last quarter’s estimate – steady as daisies. If we strip out the fickle food and energy prices, the core PCE climbs even more, hitting 2.6% – again, a quick bump of 0.1% from the previous figure.

Bottom Line

So, even with the usual price tags tightening up, the economy’s still pulling up its socks and looking better than the slump of past weeks. Economic growth seems to be dancing the last half‑step into the next quarter.

Inflation Numbers: A Warm‑Up, Not a Finale

Bottom Line

It’s just another meaningless print—not really because the data feels so stale that it’s practically a relic, but also because the market is scrambling over the ripple effects of the trade war.

The real deal? A fully updated core PCE version of the numbers drops in exactly 24 hours, and that’s the plot twist everyone’s waiting for.

- Stale Data: Think of it as the bread that’s gone flat before you even started baking.

- Trade War Tension: The market’s eyes are on trade-blueprints, not on yesterday’s figures.

- Upcoming Core PCE: Fresh and ready to be “served” in 24 hours—no more stale crumbs.

We’ve Got Your Recommendations Ready!

Stay tuned—once the fresh numbers roll in, we’ll cut the fluff and deliver the insights you need, minus the breakfast‑stale drama.