What’s Happening This Week in the Money World

The economic calendar is flat as a pancake—no big, blatant headline events are on the horizon. That said, chaos keeps creeping in all the time, so while it’s quiet on paper, the universe is probably refusing to stay still.

Key Highlights

- Global Flash PMIs – Thursday, a sneak‑peek into how manufacturing worldwide is feeling.

- ECB Holds – No policy changes, just a “no‑action‑packed” meeting that the crowd expects.

- Fed’s Radio Silence – Preparing for next week’s FOMC, they’re keeping the press off the hook.

- Potent Trump – He’s going to keep harping on Powell every day, so expect some side street noise.

- Powell’s Regulatory Talk – Tomorrow, but no word on money policy (blackout rules).

US Market Sensors for the Next Few Days

- Regional Manufacturing Surveys – Tomorrow: see how factories on different coasts are doing.

- Existing Home Sales – Wednesday brings the latest on houses already on the market.

- New Home Sales – Fresh listings going up for grabs.

- Jobless Claims – Weekly count of people filing for unemployment.

- Chicago Fed’s Chicago Board of Trade Survey – Thursday’s uptick on futures and rolls.

- Durable Goods Orders – Friday shows the latest on big-ticket purchases.

In short: keep your eyes on the global PMIs, the ECB’s “hold” status, the Trump‑Powell roast, and the US auto‑updates from manufacturing to housing. That’s the low‑key soundscape for the coming days.

ECB Focuses on the Great Pause Mystery

On Thursday, Europeans will tune in to see how long the European Central Bank might hold its breath—because the real question is whether they’re going to pause the rate hikes or keep the ball rolling.

What’s on the Envy Calendar?

- ECB publishes its tantalising bank‑lending survey tomorrow.

- Next week, banks armed themselves with fresh data: French, German, Israeli, and the other European hot spots.

Economic Mood‑Check Updates

- Thursday – German consumer confidence is coming out. Yes, we’re all rooting for a spike.

- Friday – UK, France, and Italy are set to spill the beans on sentiment.

- Friday – a German Ifo survey will drop its latest business insight.

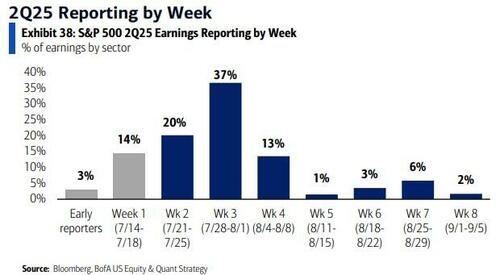

Corporate Earnings – The Party’s Over, Now What?

Quarter‑two is finally letting loose, with 135 S&P 500 firms and 189 Stoxx 600 players chipping in their numbers.

- Wednesday – the tech giants Alphabet and Tesla will drop their quarterly show flags.

- Other tech stars this week: IBM, ServiceNow, and Intel are all ready to perform.

- Defense powerhouses like RTX, Lockheed Martin, and Northrop Grumman will also bring their numbers to the table.

Stick around—whether the ECB is pausing, rolling, or racing to the next number, the markets are buzzing with activity and a little bit of caffeine‑driven curiosity.

Catch the European Earnings Wave – July 22‑25

Fasten your seatbelts, finance fanatics – the European market is gearing up for a packed week of shares, stats, and a smattering of brass‑finched central‑bank chatter. Below is the low‑down for the stars of the show, broken day by day. Grab your coffee, because the charts are rolling in!

Monday, July 21 – Zero‑Headline‑Hype

Nothing big on the data front. But keep your eyes peeled: three powerhouses of the European roster are about to drop earnings bulletins that could shift the market’s mood.

- Biggest name on the stage: SAP – the software giant that practically lives in the cloud.

- Also on the docket: LVMH, Roche and Nestlé – the new holdouts of the “Top‑10” club.

- And don’t forget the banks; their quarterly earnings have us all hoping for smooth sailing.

Tuesday, July 22 – Oil Fires & Earnings Bonanza

Data has been quiet – performances are loud.

- Data Highlights:

- U.S. Philly Fed’s payroll‑satir start (non‑manufacturing)

- Richmond Fed’s manufacturing stance sticking?

- Number crunching of the UK’s public finances and France’s retail scene.

- Central‑Bank Chatter:

- Powell’s tweet‑worthy remarks on U.S. Fed policy.

- ECB’s labour‑in‑lending survey – will banks feel the buzz?

- BoE’s Bailey diving into monetary policy (yes, still hot!).

- RBA’s July minutes – jo’ jo’ it.

- Earnings Hype:

- Legendary SAP (carry the flag!)

- Happy CFO’s report from Coca‑Cola.

- Welcome to the big tech club: RTX, TEXAS Instruments, Intuitive Surgical.

- Financial fairy tales: Capital One, Chubb, Lockheed Martin.

- Outfit-champ: Sherwin‑Williams and Northrop Grumman.

Wednesday, July 23 – Press‑Ups & Home Sales

Inside the UK’s PMI nerd‑arena & the U.S. housing market.

- Data:

- U.S. existing home sales for June – the numbers might paint a rosy skyline.

- Eurozone consumer confidence for July – love that over‑the‑counter portal.

- Central‑Bank Whisper:

- The BoJ’s Ochida telling us whether the yen will keep flirting.

- Earnings Parade (Next‑Gen Goldmine):

- Alphabet, Tesla – feel the electric buzz.

- IBM’s secrets, T‑Mobile’s deals, IBM, AT&T’s Q4 reveal.

- Biotech bragging: Thermo Fisher, NextEra Energy ‘s solar rockets.

- Health & Hospitality: Boston Scientific, GE Vernova.

- And a full lineup of intangibles: banking, food, and zero‑emission power companies.

- Auction Flash:

- U.S. 20‑yr bonds re‑open for $13 bn – the tick‑tock is real.

Thursday, July 24 – Market Milestone Money‑Sweets

All eyes on the EU’s fledgling PMI spree.

- Data:

- PMIs across U.S., UK, Japan, Germany, France, Eurozone.

- Chicago and Kansas City Fed quips about activity and manufacturing.

- Jobless claims to keep us laughing over the 221k, 232k numbers.

- Germany’s GfK consumer confidence – in September or not? It may rock that.

- Central‑Bank Booms:

- ECB’s decision – will the euro survive the tremors?

- Earnings Extravaganza:

- From LVMH luxe to Blackstone bank deals.

- Tech titans: SK Hynix, TotalEnergies.

- Transportation vibes: Union Pacific, Intel, Newmont.

- List of bank & insurance names to keep your portfolio glued to the board.

- Auction Warm‑ups:

- U.S. 10‑yr TIPS at $21 bn – the rate‑tracking calendar!

Friday, July 25 – Durable Goods & Consumer Cheers

Durable goods are the main event of today’s data docket.

- Data:

- Durable goods orders for June – an initial 9% slip painting a picture of resurgence.

- Core capital goods insights: a 0.2% drop in orders and a 0.3% rise in shipments.

- Other favorites: PPI, consumer confidence and professional forecasts.

- Central‑Bank Voice:

- ECB’s survey of professional forecasters – the “market wizard” graphic.

- Earnings Collectibles:

- HCA Healthcare’s wellness analysis.

- Charter Communications shares – find your internet bandwidth.

- Volkswagen’s car‑finance insights, NatWest’s banking backstage.

- And we’re wrapping up the big round of industry names: Eni, oil and gas, lending, and more.

Heads up – the U.S. gets the biggest data push this week with durable goods orders on Friday. No Fed monetary haggling this week (the blackout pre‑FOMC), so focus on the numbers. Tune in, trade nicely, and keep your portfolio humming – we’re all in this financial rave together.