Why the Treasury’s Cash Reserves Are Vanishing Fast

It’s been a bone‑shaking tumble. For the last year and a half the Treasury has been holding roughly $800 billion in cash—like the financial equivalent of a massive savings jar. But in just the past month, that huge stash has shrunk by a staggering $480 billion. If you’re following the financial chatter, you know the headline: Treasury cash down $480 billion in the past month.

What’s Behind the Numbers?

Ever since the debt ceiling became a real, not just a polite, notice out of the White House, the Treasury can’t issue fresh bonds. Think of it like a bank that’s run out of fresh credit cards. That means the Treasury has to dip into its existing cash to keep the government running day‑to‑day.

Now, the sky is not infinite. Once that cash balance hits zero, the Treasury will be forced to pick who pays first. The consequence? We could see delayed interest payments or even straight‑up default—money that is due but never paid.

The Congressional Budget Office’s Alarming Forecast

The latest CBO report was released this morning, and guess what? If lawmakers keep the debt limit stubbornly as it is, the government may run out of borrowing power around August or September this year. The exact date is fuzzy because it depends on how revenues and spending play out over the next few months.

The report’s key takeaway: Once the debt ceiling stays flat, extraordinary borrowing tricks will die out by late summer 2025.

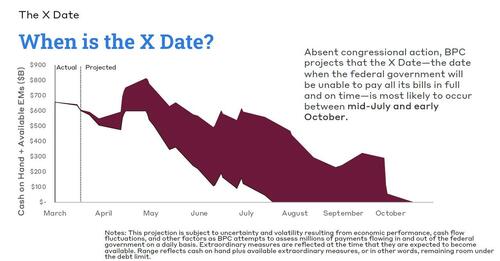

What Bipartisan Policy Center Says

On Monday, the Bipartisan Policy Center rolled out some unsettling numbers based on public data. They predict that the Treasury will start defaulting on obligations sometime between mid‑July and early October—no ifs or buts.

In short, the Treasury’s cash balance is in free‑fall, and the clock is ticking. Unless lawmakers raise or suspend the debt limit soon, the U.S. government could run into a serious cash crunch, with the possibility of missed payments looming as a real, not hypothetical, danger.

GOVERNMENT’S FINANCIAL TICK-TACK: THE DEBT CEILING DANCE

Picture this: the Treasury suddenly finds itself juggling a $36.1 trillion debt ceiling that’s been looming over it since the start of the year. They’ve been pulling a few clever accounting tricks since January 21 to keep the numbers from blowing up, but when those tricks run out is still up in the air. The stakes? A potential crunch in late May or June, before tax money starts trickling in mid‑June or an emergency measure is announced on the 30th.

Why the clock’s ticking

- Unpredictable tax receipts: Ever tried guessing how much money taxpayers will actually hand over? It’s like guessing lottery numbers.

- Rep. Jason Smith says it could be mid‑May: The door to financial disaster might open earlier than we thought.

- House Republicans are hungry for a swift tax bill: They want to squeeze all that money into legislation ASAP—ideally before the midterm elections roll around.

Enter the Trump Tax Monster

President Trump and his allies are eyeing a “$4+ trillion” extension of 2017 tax cuts that mostly favor the 1% of Americans who can afford to get rich faster. Add a handful of “painless” tweaks—like ending taxes on tips, overtime, and Social Security—and the total could balloon over $11 trillion in ten years, according to the Committee for a Responsible Federal Budget.

The “Budget Reconciliation” Shortcut

Reconciliation is like a celebrity backstage pass: it lets the GOP pass a bill with just 50 Senate votes instead of the usual supermajority. That means they can pair a tax cut with a debt‑ceiling hike in one go. But many in the House are wary of signing onto trillions of fresh debt without bipartisan applause.

House vs. Senate: The Strategic Divide

- House Republicans want to move fast, even if it means slashing Medicaid—a tough sell but a Party win in their eyes.

- Senate Republicans are more comfortable taking time, preferring to write a less aggressive tax plan that trims Medicaid cuts.

- “Coloring the bill” rumors: Senators might try to keep the “big tax kick” to a manageable size.

What Happens If Republicans Miss the Deadline?

According to Brian Gardner of Stifel, “If we can’t get the tax bill before the debt ceiling yanks in, we’ll need Democrats for a separate solution.” This could force:

- A political bargain from Senate Minority Leader Chuck Schumer.

- Potential blowback from Democratic base and a high‑stakes showdown.

- Worsened market volatility because Treasury may have to prioritize bondholders over other federal obligations.

Final Notes

House Democratic Chair Pete Aguilar warned that “nothing should be given away for free” when it comes to the debt ceiling. The political landscape is braced for a tense, high‑stakes bargain that could shape the economy for years to come.

The Eastern Florida State College women’s golf team will open the fall season Monday morning at the Seminole State Fall Warm Up at Rio Pinar Golf Course in Orlando. (EFSC Image)

The Eastern Florida State College women’s golf team will open the fall season Monday morning at the Seminole State Fall Warm Up at Rio Pinar Golf Course in Orlando. (EFSC Image) Related Story:Eastern Florida State College Women’s Soccer Team Defeats Butler 4-2 in Home Opener

Related Story:Eastern Florida State College Women’s Soccer Team Defeats Butler 4-2 in Home Opener Related Story:HOT OFF THE PRESS! August 25, 2025 Space Coast Daily News – Brevard County’s Best Newspaper

Related Story:HOT OFF THE PRESS! August 25, 2025 Space Coast Daily News – Brevard County’s Best Newspaper