BofA’s Crystal Ball X-Force Says Traders Better Load for Calm

If BofA’s omniscient analysts are right—yes, they’ve been consistently on the winning side of this data series versus consensus for months—then traders should strap in for a bit of disappointment when the retail sales numbers drop into the night sky this morning.

In other words, don’t be surprised if the market takes a polite but firm bite away from those rosy forecasts.

Whoa, Wall Street Got It Wrong Again!

Retail Sales Surprise & the BofA Glitch

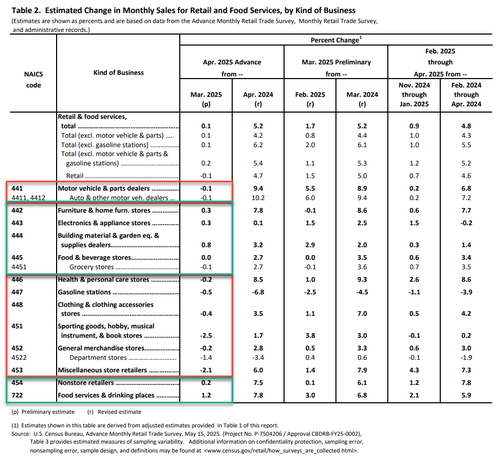

It turns out the Bank of America analysts missed the mark one more time. The headline retail sales jumped 0.1% month‑over‑month—so close to the market’s 0.0% expectation, but with a bonus tweak from last month’s surprises.

In March, economists had climbed the chart by +1.7% (instead of the originally projected +1.4%), giving buyers a little extra breathing room. That nudged the yearly figure up to +5.2%—right in the ballpark of the biggest jump since December 2023.

- 0.1% MoM increase thrilled shoppers and startled analysts.

- March’s +1.7% revision polishes the forecast.

- Year‑on‑year +5.2% puts us near the peak from last year’s December.

So if you’re planning a big shopping spree, remember: even Wall Street can swerve. Just go ahead—those sneakers are now officially better than your analysts predicted!

Sector Showdown: Sporting Goods Takes a Dip, Building Materials Rise to the Top

Why the market’s feeling a little sports‑centric and a lot of construction verbs.

Bloomberg’s latest rundown points to a clear winner and loser in the current trading landscape. Sporting Goods fell the steepest – think of it as a bad day for your favorite football shoes – while Building Materials shot up the loudest, like a new skyscraper hitting the skyline.

Key Takeaways

- Sporting Goods: Hit the worst slump of any sector. Investors seemed to have tossed their sports memorabilia into the bin.

- Building Materials: Experienced the biggest rally. Steel, lumber, and cement turned into the market’s new best friends.

- Other sectors saw modest moves, but the contrast between these two was hard to miss.

What’s the Inside Story?

When the bell rings, traders looked at sales fueling the economy. Sporting Goods—think gyms, outdoor gear, and that pricey new game console—struggled to keep pace. On the flip side, the construction surge suggests homes, businesses, and even new bridges are on the upswing.

Humor & Emotion: The Crowd’s Reaction

Picture a sports bar where everyone’s cheer squad is suddenly on sale. The cheers get quiet, and in the corner, someone with a hard hat is raising a toast to the booming building sector. “Let’s build up (the mood)” – you heard that right.

Bottom Line

In a nutshell, sporting goods shoppers feel a chill, while the trowel and hammer have a warm, triumphant vibe. Stay tuned for more updates on which sectors will keep their footing or go off the rails!

How Tariff Front‑Running Boosted Car Sales into a Wild Spin

Last month the motor‑vehicle market didn’t just shift—it sprinted. A so‑called tariff front‑running strategy pushed sales into a frenzy that had everything from bump‑in‑the‑road nutty to body‑shop managers cracking jokes about bumper‑up‑blowing.

Why the Surge Happened

- Strategic Price Hikes – When tariffs on imported cars popped, dealers pulled the trigger and lifted prices for a brief window.

- Consumer Psychology – The fear that “prices will go even higher” sparked a buying frenzy: “Buy now or rejoice later!”

- Limited Time Offers – “Deal for 48 hours only” slapped over shiny SUVs turned resale markets into arm‑chairs for quick grabs.

How Dealers Responded

- “Front‑running” was the name of the game: buying bulk inventory before tariffs kicked in. It kept the shelves stocked while others were scrambling.

- Dealerships stuffed promotional posters in the aisle, each one shouting: “Lowest price in town! Limited stock—grab it!”

- Some owners laughed and said, “I got my car at the wrong price in the name of front‑running; it’s like a game of Monopoly, but the house rule is ‘pay less if you rush’.”

Customer Highlights

- “I nearly lost my heart to a 2019 sedan – then the dealer convinced me it was the early‑bird special!” – says Emma K.

- “The reason I bought a used SUV last week was the front‑running craze; I’d never felt such a thrill when picking a car!” – declares Marco D.

- People are now calling it the “Turbo‑Tax” of the automotive world because those extra dollars are burning in the newest cars.

What’s Next?

Car polls say that if the tariffs keep the momentum, the market might just keep looking like a roller‑coaster for the next few months. Dealerships are poised to find the sweet spot between competitive pricing and thriving inventory while customers keep cheering for their next car adventure.

Bottom Line:

Tariff front‑running doesn’t just create a sudden spike—it creates a vibrant, emotional rush that basically turns anyone in a dealership into a playful gambler. A perfect mix of daring, drama, and a dash of humor.

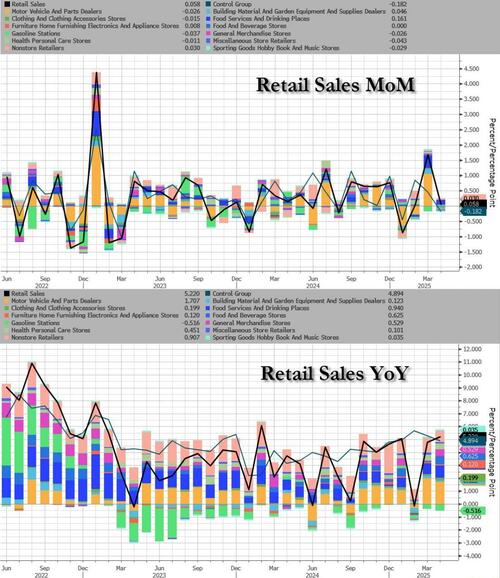

Retail Sales Break Out of the Cold

Picture this: every month people dump their wallets on the shelves—retail sales just sprinkled a generous 2.8 % increase year‑over‑year. That’s not a casual bump; it peaks the entire data stream from February 2022. Sound exciting? Let’s unpack the numbers.

What’s Really Happening?

- Nominal Numbers – The figures we see are straight‑line, not tweaked for inflation. Think of it like watching a movie in full color, not through a filter that removes the “real” picture.

- Rough Inflation Adjustment – A quick, low‑effort recalibration shows the growth remains solid when you factor in the cost of living.

- Compares to 2022 – The latest climb hits a high that hasn’t been seen since the early part of last year, meaning shoppers are still flustered around discounts and new gadgets.

Why the Buzz?

Retail sweet‑spot nudges the economy’s heartbeat. When sales climb, it hints that the crowd’s buying confidence is still open for business. From grocery aisles to flagship stores, this uptick signals “we’re climbing back up, folks.”

Funny Side‑Note

Do you think you’re saving? Maybe. If your mall run feels like a mini‑treasure hunt, you’re in the right frame.

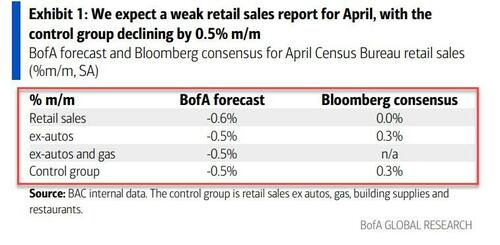

Economic Surprise! The Control Group Takes a Nosedive

What’s a Control Group Anyway?

The control group is the part of a survey that feeds directly into GDP calculations. Think of it as the “behind the scenes” crew that compiles the big numbers. If GDP was a movie, the control group would be the backstage crew—making sure everything runs smoothly. But hey, even backstage crews can slip on a banana peel.

Unexpected Drop – 0.2% vs Expected Gain

- Reported movement: Down 0.2% month‑over‑month.

- Expectation: A tidy 0.3% uptick.

- Result: A disappointment that rattles the market like a faulty elevator.

Why It Matters

When the control group missteps, GDP might skimp on its growth estimate. Investors scream, “Where did the money go?” and analysts scramble through spreadsheets faster than a caffeinated squirrel.

Bottom Line

Short‑term shock, long‑term questions. Keep your coffee ready—analysts are sprinting to patch the numbers. Meanwhile, you can sit back, breathe, and maybe laugh at the irony: a tiny fall in a tiny group can make a big splash in the economics ocean.

Americans Are Throwing Cash Into The Economy… But GDP Might Still Be Feeling the Pains

Let’s cut to the chase: Retail sales, dining‑in, and grocery runs are on the rise. That tasty “bottom‑up” picture shows folks throwing money down the consumer aisle, proving there’s still a lot of enthusiasm for everyday spending.

What “Bottom‑Up” Means

In simple terms, “bottom‑up” folks track how every single American is spending money. With more people buying coffee, streaming services, and that designer pair of sneakers, the data is singing a bright note. It’s like a group of friends happily tossing coins into a wishing well.

But the “Top‑Down” Side…

By contrast, the GDP company keeps a high‑level scoreboard that includes business investments, government spending, and global trade. Recent figures suggest that while consumer spending is thriving, the big boys—factories, tech firms, and real estate projects—haven’t been as exuberant. That means the overall GDP chart might dip a wee bit.

Why the Gap Appears

- Supply Chains: Manufacturers face bottlenecks and higher costs.

- Labor Market: While wages are rising, there’s still a shortage of skilled workers in certain sectors.

- Inflation Hiccups: Fluctuating prices make it harder for firms to plan long‑term.

What It Looks Like Today

Data from the U.S. Bureau of Economic Analysis (BEA) shows the consumer‑spending indicator by March hitting a new peak, a testament that Americans feel confident enough to splash out. That same month’s GDP, however, experienced a modest contraction thanks to lagging business investments and a lag in the real economy.

Think of it as having a packed party floor (consumer spending) but a loosely packed backstage (business data). The dance floor is full and livin’, but the stage crew isn’t cutting it.

Implications for the Economy

- Consumer Confidence remains high, fueling the retail economy.

- Business Sentiment is still cautious—companies are holding off on new capital investments.

- Inflation Pressure could stay at eye‑level, impacting wages and consumer budgets.

What Should We Do?

Addressing the mismatch means schools of thought converge:

- Boost productivity in sectors that lag behind, like manufacturing.

- Offer incentives for businesses to scale up and invest in new technologies.

- Implement sound monetary policy to ease the rhythm of inflation.

Bottom Line: The Economy’s Pulse Is Mixed, But The Beats Are Still Going

Bottom‑up spending is as vibrant as ever—so great for restaurants, shops, and the folks behind their doors. Top‑down GDP, meanwhile, is a bit more cautious. The key takeaway? The U.S. economy is showing resilience, but like any good dance routine, it needs a little seasoning to make every section move in harmony.

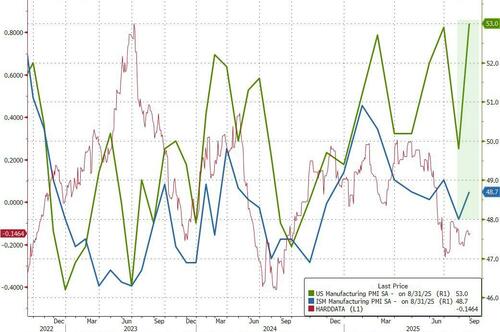

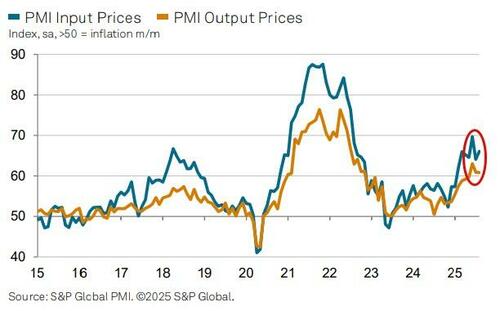

Source: BloombergUnder the hood of the ISM data, we see prices falling significantly, nmew orders jumping, but employment remaining significantly weaker (as we suggested will happen)…

Source: BloombergUnder the hood of the ISM data, we see prices falling significantly, nmew orders jumping, but employment remaining significantly weaker (as we suggested will happen)… Source: Bloomberg“Purchasing managers reported that the US manufacturing was running hot over the summer,” according to Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.“The past three months have seen the strongest expansion of production since the first half of 2022, with the upturn gathering pace in August amid rising sales. Hiring also picked up again in August as factories took on more staff to meet an influx of new orders and an accumulation of uncompleted work for waiting customers.”“The manufacturing sector is therefore on course to provide a boost to the US economy in the third quarter. But inflationary fears loom…“The upturn is in part being fueled by inventory building, with factories reporting a further jump in warehouse holdings in August due to concerns over future price rises and potential supply constraints. These concerns are being stoked by uncertainty over the impact of tariffs, fears which were underpinned by a further jump in prices paid for inputs by factories, linked overwhelmingly by purchasing managers to these tariffs.

Source: Bloomberg“Purchasing managers reported that the US manufacturing was running hot over the summer,” according to Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.“The past three months have seen the strongest expansion of production since the first half of 2022, with the upturn gathering pace in August amid rising sales. Hiring also picked up again in August as factories took on more staff to meet an influx of new orders and an accumulation of uncompleted work for waiting customers.”“The manufacturing sector is therefore on course to provide a boost to the US economy in the third quarter. But inflationary fears loom…“The upturn is in part being fueled by inventory building, with factories reporting a further jump in warehouse holdings in August due to concerns over future price rises and potential supply constraints. These concerns are being stoked by uncertainty over the impact of tariffs, fears which were underpinned by a further jump in prices paid for inputs by factories, linked overwhelmingly by purchasing managers to these tariffs. “Cost increases are being passed on to customers via widespread hikes to factory gate prices. The big question is the degree to which these price rises will then feed through to higher consumer price inflation in the coming months.”So S&P Global sees prices higher and hiring improving while ISM sees prices falling and employment still badly lagging… take your pick!!Loading recommendations…

“Cost increases are being passed on to customers via widespread hikes to factory gate prices. The big question is the degree to which these price rises will then feed through to higher consumer price inflation in the coming months.”So S&P Global sees prices higher and hiring improving while ISM sees prices falling and employment still badly lagging… take your pick!!Loading recommendations…

{kind=link}

{kind=link}