Central Banks Grab the Spotlight After a Turbo‑charged Earnings Season

After a whirlwind first‑quarter profit parade and a macro‑boom that shipped the economy past the “tariff‑turbo” doldrums, we’re rolling into a week that’s all about the lofty leaders of U.S. and U.K. policy. The Federal Reserve will speak on Wednesday, followed by a crisp press conference for Chair Powell, and the Bank of England will drop its voice on Thursday.

Why the Fed and the BoE are the stars

- Markets have shrugged off the past weeks’ tariff jitters, thanks to a surprisingly upbeat jobs report and solid U.S. payrolls.

- That lift pushed the S&P 500 back above its pre‑Liberation Day highs, sparking the longest winning streak since 2004.

- Not every asset class is partying with the 2004 vibe—think the U.S. dollar, which is down nearly 4% from its April 2 peak.

- Investors are eyes‑rolling over tariff headlines and watching data like the U.S. April ISM services (today), German factory orders (Wed), and China’s April trade numbers (Fri). Because tariffs aren’t just about trade, they ripple across everything.

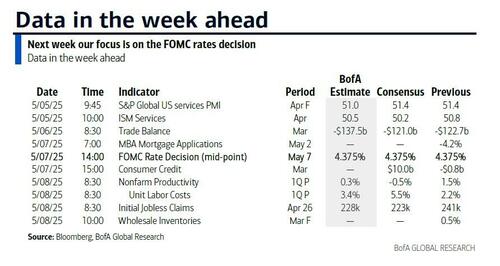

The Fed’s Forecast

Most economists are leaning toward a steady‑rate outlook. The Fed’s likely to keep rates unchanged, and they won’t drop any “forward guidance” for a while. The general vibe will echo recent speeches: the administration’s policies might tug the economy a bit farther away from the Fed’s dual mandate for a stretch, but the Fed is “well positioned” to respond when the outlook evolves.

Rate‑cut jawbreakers surged after that strong jobs print, but markets now say the next cut hinges on a weaker labor market—after all, the Fed won’t cut up there until it feels the need.

- Fed funds futures now price a 37% chance of a cut by the June meeting, and a full 25bp cut by July.

Europe’s Central‑Bank Spotlight

Thursday’s agenda over in Europe will see the Bank of England, Norges Bank, and Riksbank in the flashlights:

- BoE is expected to trim rates by 25bp, making the Bank Rate 4.25%.

- Both Norges and Riksbank are likely to hold rates steady.

Meanwhile, the European Central Bank will hold an informal meeting on May 6–7 to talk around its 2025 monetary‑policy strategy.

Key Economic Data in the U.S.

Today’s main test lies with the April ISM services reading, expected to slide just a touch to 50.3. The current road shows a modest decline from last week’s 50.8—still keeping the image of a dampened but not yet broken economy.

As we hang on the central banks’ watercooler chats and the economic releases, we’ll keep you updated on the financial waves. Stay tuned!

Week‑in‑Review: Europe’s Chill & Asia’s Are‑Worried Trade Signal

It’s gonna be a pretty quiet data week over in Europe—Germany’s factory orders on Wednesday and industrial output on Thursday are the main steak. Across the sea, Asia’s April trade numbers from China on Friday are poised to reveal a pretty significant slowdown as tariff chaos continues to stir the pot.

Corporate Beat – Pick Me Up

- US – Palantir, AMD, Walt Disney, Uber, and a gallery of other high‑profile earnings dropping into the spotlight.

- Europe – Novo Nordisk, Siemens Energy, AP Moller‑Maersk, BMW, AB InBev, Rheinmetall – all neck‑and‑neck in a trades‑tension heated arena.

Day‑by‑Day Snapshot

Monday, May 5

- Data – US April ISM services, Switzerland CPI.

- Earnings – Vertex, Williams, CRH, Ares, Diamondback Energy, Ford, BioNTech, ON Semiconductor.

- Auction – $58 bn US 3‑yr Notes.

Tuesday, May 6

- Data – US Mar trade balance, China Apr Caixin services PMI, UK April reserve changes, new‑car registrations, France Mar industrial output, Italy Apr services PMI, Eurozone Mar PPI, Canada Mar merchandise trade.

- Earnings – Palantir, AMD, Arista, Intesa Sanpaolo, Ferrari, Constellation Energy, Zoetis, Marriott, Coupang, Fidelity, EA, Datadog, IQVIA, Rivian, Vestas, Astera Labs, Zalando.

- Auction – $42 bn US 10‑yr Notes.

Wednesday, May 7

- Data – US Mar consumer credit, China Apr reserves, UK Apr construction PMI, Germany Mar factory orders, April construction PMI, France Mar trade balance, current‑account, Q1 wages, private‑sector payrolls, Italy Mar retail sales, Eurozone Mar retail sales, Sweden Apr CPI.

- Central Bank – Fed decision.

- Earnings – Teva, Novo Nordisk, Walt Disney, Uber, ARM, MercadoLibre, DoorDash, Fortinet, Siemens Healthineers, BMW, Carvana, Axon, Vistra, Flutter, Occidental, Barrick Gold, Legrand, Rockwell, Vonovia, Ørsted, Pandora, Telecom Italia, Sandisk.

Thursday, May 8

- Data – US Q1 non‑farm productivity, Q1 unit labour costs, Mar wholesale trade sales, April NY Fed 1‑yr inflation expectations, initial jobless claims, UK RICS house‑price balance, Germany Mar industrial output, trade balance.

- Central Banks – BoE, Riksbank, Norges Bank decision; BoJ March minutes; BoE April DMP survey; BoC financial‑stability report.

- Earnings – Toyota, AB InBev, Shopify, ConocoPhillips, Nintendo, DBS, McKesson, Enel, Rheinmetall, Siemens Energy, Coinbase, Cheniere Energy, Infineon, Kenvue, HubSpot, TKO, Leonardo, AP Moller‑Maersk, Warner Bros Discovery, Toast, Expedia, Pinterest, DraftKings, Affirmm, Tapestry, Illumina, Banca Monte, Rocket Lab, Paramount, Campari, Crocs, Lyft, Puma, Peloton, Sweetgreen.

- Auction – $25 bn US 30‑yr Bonds.

Friday, May 9

- Data – China Apr trade balance, Q1 BoP current account, Japan Mar labour cash earnings, household spending, leading index, coincident index, Italy Mar industrial output, Canada Apr jobs report, Norway Apr CPI.

- Central Banks – Fed officials speaking (Williams, Waller, Kugler, Goolsbee, Barr), ECB (Simkus, Rehn), BoE (Bailey, Pill).

- Earnings – Mitsubishi Heavy Industries, Recruit Holdings, Commerzbank, Cellnex.

Why This Matters

While Europe’s data is going to keep things slightly under the radar, Asia’s slowing trade due to tariffs will inevitably ripple across global markets. The US’s ISM services read‑out on Monday gives a first clue into whether commercial conversations are still comfortable or starting to feel the pinch. The FOMC will keep an eye on the lane marked “Rate Cut”—think of it as a laid‑back road trip guided by the latest wage and productivity drops.

Fed officials and central banks will be on the mic, offering “talk‑to‑the‑public” insights into the great balancing act of stimulating employment vs. curbing inflation. These speeches can tip the scales in the markets, especially if the trade and tariff updates storm the newsroom.

In short, prepare to catch the high‑wire juggling act between businesses climbing the chart and governments walking the fine line of monetary stability.