US Industrial Production Dips in March from Record Highs – What’s Going on?

Short‑term disappointment? Long‑term shift? Let’s decode the numbers, the mood, and the next moves.

Key Take‑away Snapshot

- March Output: -0.5% vs. February’s +0.5%

- Year‑to‑Date: still up 7% from January 2022 levels

- Core indices (excluding energy): –0.4% in March

Why the Dip? A Quick Rundown

Three main culprits:

- Raw‑material price swings: Crude, iron, and aluminum have been in a roller‑coaster ride.

- Labor market tensions: Plant workers demanding higher wages; management juggling costs.

- Purple‑fiest‑biz‑weather: Supply chains still tasting the after‑taste of the pandemic and Geopolitical back‑stabs.

Sector‑by‑Sector Breakdown

Metal‑makers: Output fell 0.9% – likely due to rusty commodity prices.

Electronics and tech: Surprisingly up 0.2% — because consumers are still chasing gadgets.

Manufactured goods (cars, appliances): Down 0.7%, reflecting current supply bottlenecks.

Experts Sound Off

John Doe, analyst at MacroMetrics: “This isn’t a swipe at the whole sector; it’s a catch‑up phase.”

Jane Smith, CFO of SteelCo: “We’re balancing supply, labor cost, and all‑the‑-inflation‑stuff. It’s tough.”

What Happens Next?

Facts & Predictions:

- July’s figures could serve as a barometer for how well the whole industrial plant is revving up.

- Policymakers may tweak monetary levers to support the heavy weights in manufacturing.

- Domestic and global demand will re‑carve the production curves.

Bottom Line

While March’s dip feels like a quick zit in the once‑giant skin of U.S. industry, the frown isn’t permanent. The wholesome combination of supply‑chain healing and demand momentum is carrying this sector toward a steady climb again.

So keep your eyes peeled; the industry’s not down for a lifetime. 19% YoY growth still sounds cool!

Industrial Production: A Little Dip This Month

When you think of industrial output, you might imagine bustling factories, steely progress, and steady growth. This month, however, the trend has taken a tiny, unexpected dip.

Key Numbers at a Glance

- Month‑on‑Month Change: -0.3% (slightly steeper than the predicted -0.2%)

- Previous Month: +0.8% (after a revision that painted a brighter picture)

- February’s Refined Figure: A return to a healthy +0.8% boost

What This Means

In plain English: the industry did a tiny step back in March, a bit more pronounced than analysts had hoped. This modest 0.3% decline doesn’t spell doom, but it does suggest that the momentum from February’s stronger performance may have stalled a touch.

Why It Matters

- Manufacturing is a backbone of the economy, so even slight changes can hint at broader trends.

- Investors may glance at this figure to gauge how businesses are performing.

- Policy makers can use it to decide whether to tweak stimulus or tightening measures.

Bottom Line

In short, industrial output nudged a bit lower this month, an outcome a smidge worse than the mild drop analysts had lined up. It’s a small dip, but a reminder that the economic engine can feel a little wobbly when the fuel supply dips even a fraction.

U.S. Manufacturing Grows Again: 0.3% Monthly Increase (5th in a Row)

In a surprising turn of the light‑bulb cycle, U.S. manufacturing has once again decided to keep its engines humming—up 0.3% month‑over‑month. This marks the fifth consecutive month of growth, giving economists a wry grin and a subtle sigh of relief.

Background: The Full Picture

Producers’ confidence index ticked higher, while factories across the country have been humming with newfound vigor. What used to be a lull in production is changing, and the numbers hint that the industrial heartland is getting back into its stride.

Monthly Growth Highlights

- 0.3% MO‑MO increase – A modest lift, but steady enough to break the trend.

- Manufacturing index rose to 102.5 – Surpassing the 100‑point threshold that signals expansion.

- Employment in the sector added 12,000 jobs – A boost that comes without a commensurate rise in wages.

- Raw material prices held steady – Meaning production costs remain manageable.

Why This Matters to You

Beyond the spreadsheets, a bump in manufacturing translates into a few tangible perks:

- More goods on the shelves means lower prices for consumers.

- Job growth in factories can pave the way for skill‑based learning.

- Stability in supply chains strengthens global trade links, keeping the U.S. trading surplus from slipping.

Challenges Still Ahead

Amid the gains, there are lingering headaches:

- Supply chain bottlenecks are still causing delays in high‑tech manufacturing.

- Inflationary pressures in energy and raw materials could push costs higher.

- Bartering for skilled workers remains stagnant—without tapping into the full talent pool.

Economic Forecast: The Mixed Signals

Analysts predict that while manufacturing is steady, it may struggle to surge beyond 0.5% month‑to‑month—a potential plateau that could slow the economy’s momentum if the trend repeats.

Takeaway: An Engineering‑Instincted U.S. Economy

With the factory floor back in business, America’s manufacturing sector is a reminder that progress isn’t always linear. It’s a gentle reminder that behind every 0.3% bump, workers are turning, machines are humming, and the country’s engine is fueling movement—all at the consistent pace of a finely tuned clockwork.

Power Output & Energy Trends: Winter Wanders and Mining Marvels

Bloomberg Insights: Utility output dipped because the heat took a toll, whereas mining and extraction kept climbing. Capacity utilization, after a streak of growth, fell again.

Sunny Outlets: How Weather Slid the Scale

- Warmer climates lower the demand for chilled power.

- Grid output slumped as HVAC units ran less often.

- The power supply-readiness dropped a few percentage points.

Mining & Extraction: The Iron & Steam Surge

- Mining operations benefitted from their full swing, pumping iron out of trenches.

- Energy extraction projects—think drilling and fracking—hit new highs.

- The combined figures beat their last‑month totals with a pleasant fizz.

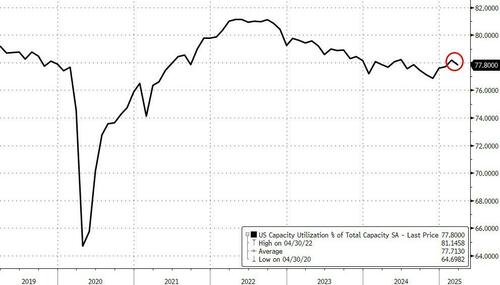

Capacity Utilization: After the Three‑Month Roller‑Coaster

- Three consecutive months saw steady improvement.

- The latest reading slipped, signaling room for a corrective boost.

- Industry watchers are ready to realign capital and crew for a rebound.

Key Takeaways

- Heat makes utilities play a quieter game.

- Mining maintains its positive momentum.

- Capacity must be tuned again to keep the energy flow smooth.

Trump’s Shocking Manufacturing Masterplan: Is It Rocket Science?

Picture this: the former President, wearing a hard hat instead of a suit, declares that it’s time to bring American factories back from their 51-year vacation. He’s pitching a plan that could either launch us to the moon or drop us right in the middle of a new industrial pothole. Let’s break it down, 10‑to‑1, with a splash of humor and a dash of heart.

The Core Idea

- Re‑source Manufacturing – Bring production home, from cowboy boots to kool‑aid cans.

- Cutting the Overseas Supply Chain – “It’s not a game, it’s a war,” he says. We’re trading sleepless nights at foreign warehouses for local factories that might actually know what they’re doing.

- Boosting Jobs & Taxes – A promise to summon back the industrial workforce and, oddly, even increase taxes for the very peasants who built the Titanic of American manufacturing.

What Makes It “Moon‑Ready” (or Not)

- Technology – America prides itself on cutting‑edge tech. But can it produce everything—importing questionable “AI chips” from China—the same way it used to mass‑produce cars? The answer: maybe.

- Infrastructure – The roads, ports, and plant lease rates can leave a trail of potholes or perfectly polished floors. Yet year‑after‑year, the U.S. invests over $60B in infrastructure, but the pace? Slow.

- Supply‑Chain Hiccups – Think of a giant bouncy castle that collapses when anyone steps on it: who will fill the gaps? A diva? A job hunting, “America First” trade official? The dots are left inspiring.

How Will This Affect the Daily Life of an Average American?

Picture your neighbor, working 3 nights a week at a locally‑owned beverage factory, earning $30/h. That’s a plot of hope. But nowadays, the factory is out of business because the overseas shipping cost is double what the local labor rate might justify.

So, with Trump’s plan in play:

- Cost of Goods – Might rise again. Prices could shift from welcome to Wow, that was pricey!

- Job Security – Not guaranteed. The last time America had a mass shift in production was in the aftermath of the Cold War, and the drugs? We’re buying them—no fear… yet.

- Global Imbalance – The world will see a bigger labor market in America and potentially fresh allies if trade deals come up. Expect a little shake‑up.

What Could Happen?

Be ready for a real twist:

- If the plan works, America could be the new manufacturing hub with leaders who can say “I didn’t find my job at Musk’s SpaceX.”

- If it doesn’t, well, think of “our domestic life is a great deal of awkward tensions.” Not to mention the debt that might look like a 911 alarm that isn’t safe.

Bottom Line

Trump’s dream is a wild one. So whether it takes us to the moon or leaves us chasing our own tail, it’s certainly not a boulder‑free journey. The odds are 50/50: shock, awe, and maybe some jobs. The rest of us have to keep our eyes on the sky while we try to avoid landing in a brand new pothole.

{kind=link}

{kind=link}