Apple’s Q3 Earnings Loom: What’s the Buzz?

1⃣ iPhone Performance: A Sagging Slide?

Apple is gearing up to drop its Q3 (3Q25) numbers next Thursday. The buzz on the town? iPhone sales are showing a little wobble.

- UBS analysts warn that June demand fizzled following a front‑loaded sales boom.

- That boom was sparked by tariff fears early in the quarter—people were rushing to buy before possible price hikes.

- Result: iPhone sell‑through dipped 18% YoY in June.

2⃣ Services Growth: Still a Strong Wing?

While iPhone sales face a chill, Apple’s Services arm continues to climb.

- Streaming, music, cloud, and the App Store keep pulling in steady revenue.

- Investors will be watching for how well this segment offsets the iPhone dip.

3⃣ Apple Intelligence: A Spark of Progress?

Apple’s foray into AI is still on the radar.

- Analysts are curious about AI-enabled products and services.

- Will it help push the platform forward, or are we still waiting for the big breakthrough?

What to Expect in the Earnings Call

- Clear numbers on iPhone sales and the June decline.

- Updates on how Services revenue is tracking.

- Concrete progress on Apple Intelligence, beyond the hype.

Bottom Line: The Apple story is a mixed bag.

Tech fanatics, investors, and the curious alike have their eyes glued to Thursday’s reveal. Apple’s latest chapter could be a tale of resilience or a cautionary tale—only time will let us know.

Apple’s June iPhone Knock‑Down: 18% Sales Drop, But a Currency Boost Keeps the Ties Tight

Picture an Apple‑Curated June where demand just fell off the runway—an 18% dip from last year’s numbers. That’s the headline. Yet behind the headlines, Apple’s “iPhone army” still climbed 3.4% in the quarter, landing at a solid 45 million units.

What went wrong?

- Early‑day sales—most of it in April and May—were heavy, because folks smelled the “tariff storm” coming. That pushed demand forward, leaving less room to swing in June.

- However, a currency tailwind—that’s the foreign‑exchange boost—helped cushion the blow, nudging Apple’s revenue past expectations.

New Numbers for June

- Revenue: $41.2 B (up 5.4% YoY)

- Earnings Per Share (EPS): $1.46 (was $1.40 in the prior estimate)

Because of the currency lift, we bumped the June outlook a touch but are pulling back for September. That’s where the change‑in‑direction kicks in.

September Forecast: Steep Winter Winds

- Units: 50 M (cut from 52 M)

- Revenue: $46 B (down from $47.7 B)

- EPS: $1.64 (trimmed from $1.68)

Apple’s hard‑to‑predict four‑month “pull‑in” from earlier sales means September will feel the chill of the prior rush. Think of it like a big heat‑wave leaving a lingering post‑breeze.

Looking Further Ahead – FY26 Trends

The early rush from April/May still looms large, dampening demand into the launch of the iPhone 17. In our view, the December‑25 fiscal quarter (Apple’s Q1 FY26) is expected to grind into a muted pace. Seasonal bars won’t be set to rise—just a modest bite in growth.

- We predict a mid‑single‑digit revenue uptick for FY26, but that’s all thanks to a slight lift that fits under the bigger picture.

- Because of the cooled expectation for the new form‑factor, consensus revenue and EPS estimates are likely to trend lower.

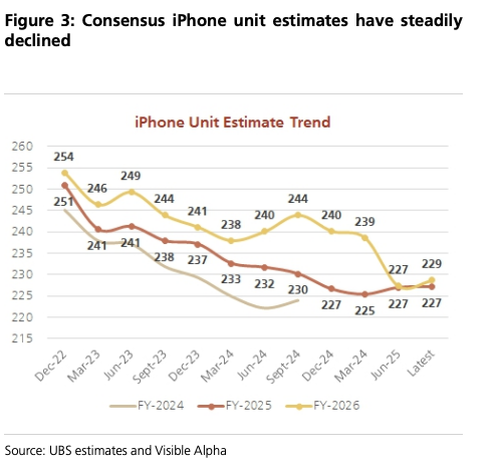

Bottom line: Apple’s iPhone unit demand is still on a slide, and the next few quarters might feel the echo of that early 2025 push‑in.

Analysts Stay Staunch About $210 Target

What’s the story?

Even after a week of market chatter, analysts are sticking with their 12‑month price target of $210. Nothing to shake things up for now.

Why the unchanged target?

- Strong earnings forecast: Earnings per share looks solid, enough to keep rockets flying.

- Consistent outlook: No new macro surprises, so the base assumptions remain solid.

- Market confidence: Shares have been steady, showing traders that the business model holds.

- “We’ve got our sights on a target and haven’t lost it in the haze”: Analysts keep a calm tone, reassuring investors.

Bottom line

The take‑away? The $210 target remains the same, and the market’s breathing easy. Just another stable day in the trading world.

Apple’s iPhone Sales: Summer Slew—or is it a Shar‑Quick Fade?

Let’s break it down in plain speak: UBS, the financial heavy‑hitter, just popped the big news that Apple’s recent iPhone sales are feeling a bit… soft. The big takeaway? There might be a chilly reception for the next August‑junkies‑get‑ready‑for‑launch lineup.

Why UBS Matters

- UBS isn’t just handing out forecasts; they’re crunching numbers that game‑changer managers look at.

- When their radar goes green for “slow sales,” it’s a red signal for investors.

- This isn’t just a headline—it’s a potential brain‑freeze for those racing to the launch.

What the Numbers Say

Apple’s summer dip isn’t a one‑off—both initial sales and post‑launch pulls lean toward the underwhelming zone. Think of it as a summer breeze that blew out the runway rockets.

So, What’s the Forecast for September?

- Expect a benign demand curve, especially if the latest tech sparkle isn’t hitting the crowd.

- Rumors about a sci‑fi, next‑gen camera, and longer battery life could, perhaps, stir the crowd if marketed right.

- Until then, gently tread the “water cooler” conversations—no one likes a loud shout about missing milestones.

Bottom Line: Stay Inspired, Stay Informed

Apple’s next iPhone could either be the splashy big splash or the measured soft rollout. Fans, analysts, and investors alike, keep an eye on the market’s pulse. If you’re watching the tech wave, remember it’s the season’s story—invested, replayed, and often rewound. Keep curious, keep watching, and don’t let a small breeze stop you from zooming forward.