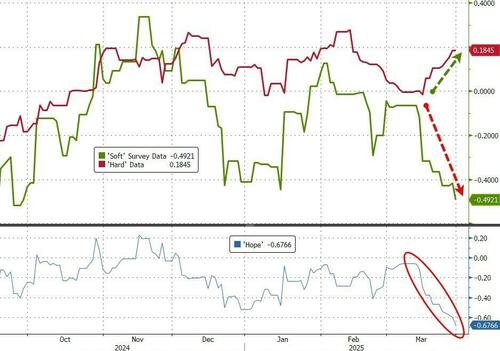

Macro Data Goes Full‑Mix‑mime: A Roller‑Coaster of Signals

We’ve all learned to get used to a little yellow‑balloon feeling each time the latest soft‑survey figures roll in. Today’s update? A bouquet of mixed messages that’ll have you second‑guessing whether the economy is moving forward or just wiggling around in place.

What the Numbers Actually Say

- Employment Growth: Slight uptick – looks promising at first glance.

- Consumer Confidence: Up, but not enough to ignite a full-blown spending spree.

- Business Outlook: Mixed – some optimism in tech, but traditional manufacturing sticks to the old hat.

- Inflation Pulse: Still lingering, but at a lower rate than expected.

Why the Confusion?

The soft survey data often reflects a snapshot of many moving parts, and each sector may feel a different article of the news. Think of it like a mixtape with tracks that jump from upbeat dance to mellower ballads – leaving you on an emotional carousel.

Quick Take‑Away (with a Smile)

In short, the macro looks like a tug‑of‑war between optimism and caution. No winner is declared yet, so stay tuned and keep your coffee ready – it’s going to be a wild ride.

What the Numbers Are Saying (and Why It Matters)

It’s a mixed bag from the US manufacturing front this week.

Bright Side: Chicago Keeps the Momentum Going

- PMI for July leapt to 47.6 — a solid bump above what analysts were bracing for.

- Still below the 50‑point line that marks expansion, but it’s the best reading since December 2023 for this region.

- What this means: A bit of a rebound in Chicago’s factories, but economic growth remains on thin ice.

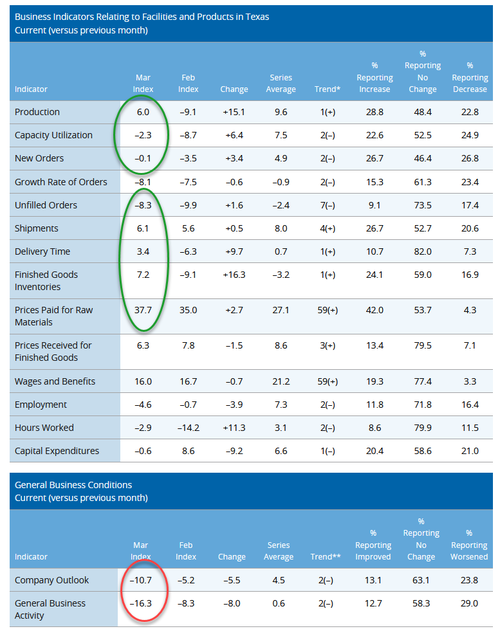

Not‑So‑Bright Side: Texas Takes a Dip

- Dallas Fed’s Manufacturing PMI slid to a punitive -16.3.

- This mark is the lowest since July 2024— a real slam‑down in production activity.

- Why it matters: A serious contraction in Texas’ steel, metal, and high‑tech sectors, and a warning bell for policymakers.

Bottom Line

Chicago’s PMI is nudging upward, giving a glimmer of hope, while Dallas’s numbers are a stark reminder that manufacturing health is uneven across the country. Keep an eye on both – they’re like the weather forecast: a sunny patch might just be a hurricane waiting to roll in.

City‑by‑City Real Estate Pulse

Let’s break it down in plain talk, no jargon—just the gist of what’s happening across two key metros.

Chicago: The Slow‑Roller (No Sweat)

- Prices Paid – Tipping the scales a bit: slower than last month.

- New Orders – The buzz has dimmed; fewer folks signing up.

- Inventories – Libraries are shrinking, so fewer homes to choose from.

Bottom line: Chicago’s market is tempering, but things are still moving—just not as fast.

Dallas: The Hot‑Spot (Ye-eh!)

- Prices Paid – Going up, pushing that golden “price tag” higher.

- New Orders – The rush? It’s still strong—more folks are inked in.

- Inventories – A surplus’s on the grow; more options for buyers.

Dallas keeps the heat on—buyers are clamoring, and sellers are feeling the pressure.

What Does This Mean?

Chicago’s slowing trends might signal buyers have more breathing room. Dallas, on the flip‑side, suggests a competitive arena where staying alert is key. Either way, the real estate landscape is shifting—so keep your eyes peeled.

The Dallas Fed’s Turbocharged Turbulence

Why the Fed’s Forecasts Are Now and Then…

The Dallas Federal Reserve’s outlook just took a nosedive—thanks to a flood of “tariff‑tiring” chatter from industry folks. The atmosphere on the trading floor smells of copper, and every analyst says, “Tariffs are the nightmare, and the future is fuzzy.”

Key Takeaways

- Immediate Cost Surge – Equipment and piping prices are climbing faster than a microwave‑toast—every project is sweating up the cost sheet.

- Tariff‑Driven Fear – Buyers and suppliers can’t gauge how much a new trade ban will push up prices. Who’s going to pay? Which markets will refuse? The unknowns outweigh the possibilities.

- Uncertain Market Shifts – A new tariff might open doors for foreign firms in the U.S., but the risk‑reward equation leans toward caution.

- Corporate Existential Angst – With Trump’s “ever‑changing” policy, planning feels like trying to predict the weather with a broken thermometer.

The Sweet Spot of Economic Possibility

Despite the “tremendous noise” about trade restrictions, the baseline economic engine keeps rolling. The cyclical rebound looks steady, but the unpredictable macro‑canvas—especially from the U.S. import taxes—casts a giant shadow over price forecasts.

What Businesses Are Tuning Into

- Import taxes from Mexico and Canada are raising costs at a rate that outpaces the official tariff numbers.

- Raw material prices are inflation‑inflated. In some loops, the price jump feels like riding a freight train that’s gone off the rails.

- Nonetheless, sales orders remain surprisingly steady. Tenacity in investing over the past year is finally paying off.

“We’re Not Losing Orders” – The Warm‑Button Counter‑Narrative

Even in a potential mild recession triggered by reduced government spending, a firm can do the math: expanding capacity now gives a net positive for the medium term. The mantra is simple – “Focus on the business, forget the policy theatre” – and it’s time to work again.

Final Closing Thought

In a world flooded with doom‑scrolling predictions, the real story is clear: tariffs are a heavy but not forgotten operand. While uncertainty stalks every strategy, the business model—rooted in fresh capital and a careful eye on cost curves—remains resilient.